Foreclosures Are Rising in Georgia and Illinois—Here’s the Short Sale Opportunity

With foreclosures rising in Georgia and Illinois, discover how short sales can turn distress into opportunity for homeowners and agents.

You can feel it happening again.

More calls from stressed homeowners. More listings sitting longer. More agents quietly wondering if that "normal sale" is about to turn into something else entirely.

And now the data is catching up to what’s already happening on the ground: foreclosures are rising—fast—in both Georgia and Illinois.

That’s not just a headline. It’s a signal.

And for agents and homeowners who understand how to respond early, it’s also a major opportunity.

The Surge Is Real—And It’s Accelerating

Recent foreclosure data shows a sharp uptick:

- Filings jumped 18% month-over-month

- First-quarter totals are up 26% year-over-year

- Illinois is ranking among the highest foreclosure rates nationally

- Georgia is climbing into the top tier by volume of new foreclosure starts

This isn’t random. It’s the result of pressure building over time—and now releasing all at once.

Even more telling: Georgia’s mortgage assistance program recently shut down, removing a safety net that had been quietly keeping many homeowners afloat.

When that kind of support disappears, distress doesn’t vanish—it surfaces.

What This Means for Homeowners

Most homeowners don’t start in foreclosure — they slide into it.

It usually looks like this:

- Missed one or two payments

- Tried to catch up, but couldn’t

- Ignored a few letters from the lender

- Suddenly facing a foreclosure timeline they don’t fully understand

By the time they reach out for help, they feel like they’re out of options.

They’re not.

A short sale can often stop the foreclosure process, protect credit far better than a foreclosure, and allow the homeowner to walk away with a clean slate.

But timing matters.

The earlier they act, the more options they have.

That’s why starting the process early—before the sale date is looming—is critical. If you’re dealing with a situation like this, the best move is to start the short sale process as soon as possible.

What This Means for Real Estate Agents

This shift is going to show up in your pipeline whether you’re looking for it or not.

Listings that:

- Aren’t getting offers

- Have unrealistic payoff numbers

- Keep getting price reductions

- Have sellers under pressure

These are often early-stage short sale opportunities.

The problem? Most agents either:

- Don’t recognize it early enough

- Or try to manage it themselves and get stuck in the process

That’s where deals start to fall apart.

Short sales are not just "another type of listing" — they’re a completely different transaction.

They require:

- Direct lender negotiation

- Strategic offer positioning

- Complete and accurate document packages

- Constant follow-up with loss mitigation departments

This is exactly where a short sale negotiator or short sale coordinator becomes critical.

If you’re working a deal like this, getting short sale assistance early can be the difference between a closing and a cancellation.

Why Georgia and Illinois Are Heating Up First

Not all markets react the same way to economic pressure.

Georgia and Illinois are showing early spikes for a few key reasons:

1. Expiring Assistance Programs

Georgia’s recent shutdown of mortgage relief programs is removing a key buffer.

2. Higher Legacy Distress Levels

Illinois has historically had higher foreclosure rates, so it reacts faster when pressure builds.

3. Affordability Pressure

Rising payments, taxes, and insurance costs are squeezing homeowners who were already on the edge.

4. Delayed Market Correction

Many homeowners held on through previous relief periods—but now those protections are gone.

Put it all together, and you get exactly what we’re seeing now: more listings quietly turning into short sales.

The Window Most People Miss

Here’s the reality most agents and sellers don’t realize:

The best time to negotiate a short sale is before foreclosure is imminent — not after.

Early-stage short sales:

- Get faster responses from lenders

- Have more flexibility in approvals

- Are less likely to fall apart

- Create better outcomes for everyone involved

Waiting too long limits options.

That’s why working with a short sale specialist early in the process is so important.

Turning Market Stress Into Closed Deals

This shift in the market isn’t something to fear—it’s something to prepare for.

Agents who adapt now will:

- Save more listings

- Close more deals that others lose

- Build stronger relationships with distressed sellers

- Become the go-to resource in their market

Homeowners who act early will:

- Avoid foreclosure

- Protect their credit

- Move on without the long-term damage

But none of that happens without the right strategy and support.

That’s where having a dedicated short sale processor and negotiation team makes all the difference.

If you’re an agent dealing with a listing that feels like it’s heading in this direction—or a homeowner starting to feel the pressure—you don’t have to figure it out alone.

We specialize in helping real estate agents and homeowners navigate short sales from start to finish, making sure deals don’t just get approved—but actually close.

You can learn more about who we work with and how we support different situations here.

The Bottom Line

Foreclosures are rising in Georgia and Illinois. That part is clear.

What happens next depends on how early people act.

Because behind almost every foreclosure filing… there was a short sale opportunity that came first.

The question is whether you catch it in time.

Short Sale vs. Foreclosure Timeline: What Homeowners Don’t Realize Until It’s Too Late

A breakdown of short sale vs. foreclosure timelines explaining how early short sale assistance helps homeowners maintain control, avoid delays, and minimize credit damage.

When homeowners fall behind on their mortgage, the conversation almost always centers on one question:

Related topic hub: Foreclosure Urgency. It groups timing-sensitive posts for sale dates, foreclosure pressure, lender postponements, and short sale options.

“How much time do I have?”

Unfortunately, that’s the wrong question.

The real difference between a short sale and a foreclosure isn’t just the final outcome—it’s who controls the timeline, the decisions, and the damage along the way. And most homeowners don’t realize how fast control slips away once foreclosure momentum starts.

Let’s break down what actually happens in each scenario, and why early short sale assistance can completely change the outcome.

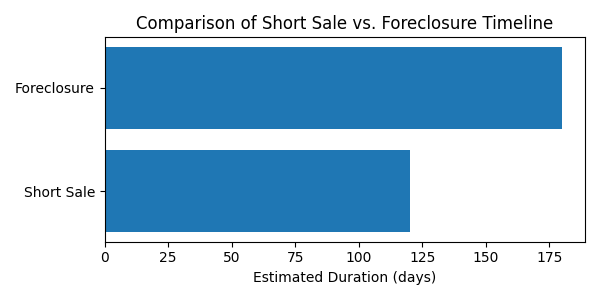

The Foreclosure Timeline: Faster Than You Think

Foreclosure feels slow—until it isn’t.

Most homeowners assume they’ll receive plenty of warning before anything serious happens. In reality, the foreclosure timeline accelerates quickly once key deadlines pass.

Here’s what typically unfolds:

- Missed payments trigger default notices

- Legal filings begin (often before homeowners fully understand their options)

- Fees, legal costs, and interest stack up

- Decision-making shifts from homeowner to lender

- Sale dates get scheduled—even while homeowners are still “figuring things out”

Once foreclosure is in motion, options narrow fast. Loan modifications get denied. Buyers hesitate. And homeowners often discover too late that a short sale is still technically possible—but now much harder to execute cleanly.

This is where many deals fail: not because a short sale wasn’t allowed, but because it was started too late and without structure.

The Short Sale Timeline: Slower, but Strategic

A short sale doesn’t stop time—it replaces panic with process.

When started early and handled correctly, a short sale gives homeowners breathing room while maintaining control over key decisions like:

- Who buys the home

- When the sale closes

- How relocation is handled

- What the final credit impact looks like

Unlike foreclosure, a short sale timeline is driven by documentation, valuation, and lender review—not court schedules.

But here’s the catch: banks don’t wait forever.

Delays, missing documents, or sloppy communication can quietly push a short sale past the point of no return. That’s why experienced short sale processing matters far more than most homeowners realize.

What Homeowners Don’t Realize Until It’s Too Late

This is where timelines collide—and mistakes become permanent.

1. Waiting Does Not Buy Time

Many homeowners delay action because they’re overwhelmed or hopeful something will change. Unfortunately, waiting usually reduces options instead of preserving them.

By the time foreclosure notices feel “real,” lenders may already be less flexible.

2. Short Sales Are Front-Loaded

The most important work in a short sale happens early:

authorizations, hardship review, document accuracy, and valuation strategy.

If those pieces aren’t handled properly from the start, approvals stall—or get denied outright.

This is where a dedicated short sale coordinator or short sale negotiator makes a measurable difference.

3. Foreclosure Narrows Buyer Interest

Buyers get nervous when foreclosure timelines tighten. They worry about auctions, title issues, and approval risk.

That reduces leverage and limits offers—exactly the opposite of what homeowners need.

4. Relocation Help Is Time-Sensitive

Relocation assistance (often called “cash for keys”) is far more likely when a short sale is organized early and presented correctly. Once foreclosure progresses, those opportunities often disappear.

At Crisp, this kind of homeowner support is built directly into how we help distressed sellers navigate the process.

Control Is the Real Difference

A short sale isn’t just about avoiding foreclosure—it’s about preserving agency.

Foreclosure is something that happens to homeowners.

A short sale is something homeowners participate in.

When structured correctly, a short sale allows families to:

- Exit with dignity

- Avoid last-minute chaos

- Minimize long-term credit damage

- Move forward on their own timeline

That’s why we focus on short sale assistance that starts early, stays proactive, and doesn’t rely on hope or guesswork.

Whether we’re helping homeowners directly or supporting agents through the process, our role is to keep files moving, lenders engaged, and deadlines under control. You can see exactly who we work with on our who we serve page.

The Right Question to Ask

Instead of asking, “How much time do I have?” Homeowners should be asking:

“How much control do I want to keep?”

If foreclosure is already on the horizon, the window for a successful short sale hasn’t necessarily closed—but it is narrowing.

Starting the short sale process early, with experienced guidance, is often the difference between an orderly transition and a forced one. If you’re considering next steps, this is the moment to start the short sale process before decisions get made for you.

The Top 5 Myths About Short Sales—And the Truth Behind Them

Debunk five common myths about short sales and learn the truth behind each misconception to help sellers and agents navigate short sale transactions with confidence.

When it comes to short sales, misinformation is everywhere. Sellers hear one thing from a neighbor, agents read something online from ten years ago, and buyers assume short sales are just “foreclosure light.”

The truth? Short sales are a unique, highly strategic transaction that can benefit everyone involved—when handled correctly. Let’s break down the five biggest myths about short sales and uncover the reality behind each one.

Myth /#1: Short Sales Always Take Forever

It’s true—years ago, short sales had a reputation for dragging on for six months or more. Back then, lenders were still figuring out the process, and delays were common.

The Truth: With the right negotiator and proper file preparation, many short sales can be approved in 60–90 days, sometimes even faster. At Crisp Short Sales, we pre-package every file with exactly what the lender needs, cutting weeks off the timeline.

Myth #2: Short Sales Hurt Your Credit Just Like a Foreclosure

One of the scariest misconceptions is that a short sale damages your credit just as badly as losing your home to foreclosure.

The Truth: While any late mortgage payments will impact your credit, a completed short sale is typically far less damaging than foreclosure. More importantly, a short sale can allow you to recover financially faster—often making you eligible for a new mortgage in as little as two years, compared to seven after a foreclosure.

Myth #3: The Seller Has to Pay All the Costs

Many homeowners avoid short sales because they think they’ll be hit with big fees they can’t afford.

The Truth: In most cases, the lender pays the real estate commissions and negotiator’s fees. At Crisp Short Sales, there’s no cost to the seller or their agent—ever. Our fees are built into the transaction and paid by the buyer’s side at closing.

Myth #4: Short Sales Mean the Seller Is Walking Away With Nothing

There’s a common belief that in a short sale, the homeowner hands over the keys and walks away empty-handed.

The Truth: Many lenders offer relocation assistance at closing—sometimes thousands of dollars—to help sellers move. This incentive is especially common when the short sale is part of a government program or negotiated properly.

Myth #5: Any Agent Can Handle a Short Sale Without Extra Help

While any licensed real estate agent can technically list a short sale, that doesn’t mean they should try to manage the entire process alone.

The Truth: Short sales require specialized knowledge of lender processes, document requirements, and negotiation tactics. Without it, deals fall apart. That’s why experienced negotiators like Crisp Short Sales exist—to protect the deal, keep communication flowing, and make sure the closing actually happens.

Short sales are often misunderstood, but when done right, they can be a win-win for everyone involved—lenders avoid costly foreclosures, sellers avoid devastating credit damage, and buyers can secure great properties.

The key is working with someone who knows the process inside and out. At Crisp Short Sales, we’ve spent over 15 years perfecting our system so short sales close faster, smoother, and with less stress for everyone.

If you’re a seller or an agent with a short sale on your hands, start a short sale with us today. You might be surprised how quickly we can turn a “hopeless” situation into a done deal.

What Happens After a Short Sale Offer Is Accepted?

Learn the steps to navigate the short sale process after accepting an offer, with guidance for both homeowners and agents.

Related topic hub: Short Sale Approval Delays. It breaks down lender delays, document loops, valuation problems, mortgage insurance review, and next steps.

Fast Answer: After a Short Sale Offer Is Accepted

After a short sale offer is accepted, the seller's agent or short sale processor submits the contract, hardship package, financials, authorization, HUD or net sheet, and supporting documents to the lender. The lender then reviews the seller, buyer, value, title, and investor rules before issuing approval or conditions.

What To Do Next After Acceptance

- Submit the full short sale package quickly so review starts without avoidable delay.

- Prepare the buyer for valuation, counteroffers, extensions, and lender conditions.

- Track title, liens, HOA balances, and closing costs before approval terms are finalized.

Accepting a short sale offer feels like the finish line, but it is really the handoff to lender approval. After a short sale offer is accepted, the next steps determine whether the file moves cleanly or stalls in documents, valuation, title, and buyer uncertainty. Accepting a short sale offer is an exciting step—but it’s really just the beginning. Whether you’re a homeowner trying to avoid foreclosure or a real estate agent guiding a client through the process, knowing what happens after the seller says “yes” can make the difference between a smooth approval and a stressful delay.

The Seller Chooses the Offer

In any real estate transaction, the sale of your home is a contract between the buyer and the seller, so the seller decides which offer to accept—not the bank. You’re not obligated to take the highest offer or meet any specific criteria. The decision is yours, based on what’s best for your situation.

Buyer Documentation: Proof They Can Perform

After acceptance, the buyer must show they have the ability to close. For cash buyers this means proof of funds; for financed buyers it means a pre‑qualification or pre‑approval letter. If the buyer is purchasing through an LLC, the lender will also require articles of organization listing all members and documentation that the person signing has authority to do so.

Ordering Title & Checking for Liens

Once the offer and buyer documentation are ready, work with your local title company or closing attorney to order title. The title report will list all liens, mortgages, and judgments on the property. Disclosing everything upfront prevents last‑minute surprises that could derail approval.

The Preliminary Closing Statement

Next, the title company or attorney will prepare a preliminary closing statement (also called an estimated settlement statement) outlining all of the costs on the seller side of the transaction. This includes mortgage payoff amounts, property taxes owed, title and attorney fees, HOA dues or special assessments, and transfer taxes. For homeowners, this is your first look at the numbers. For agents, it’s a required part of the short sale submission.

Submitting the Package to the Lender

Finally, your short sale negotiator will submit the executed purchase contract, buyer’s proof of funds or pre‑qualification, LLC documentation if applicable, the full title report, and the preliminary closing statement to the lender. From here, the bank will begin its review process, which may include ordering a valuation, verifying the buyer’s qualifications, and reviewing the seller’s hardship documentation.

Why This Process Matters

For homeowners, knowing what to expect keeps you in control and reduces stress, and providing complete documentation early helps speed up bank review. For agents, a well‑organized submission positions you as a professional who makes the bank’s job easier—which can lead to faster approvals and fewer deal‑killing delays.

The Bottom Line

Once a short sale offer is accepted, it’s not time to sit back—it’s time to move quickly. Each step, from collecting buyer documents to ordering title and preparing the preliminary closing statement, sets the stage for lender approval. When sellers, agents, and negotiators work together to get a complete package to the bank early, short sales can move surprisingly fast—and everyone gets to the closing table with less stress.

Ready to navigate your own short sale? Start a Short Sale or learn How We Help with Crisp Short Sales.