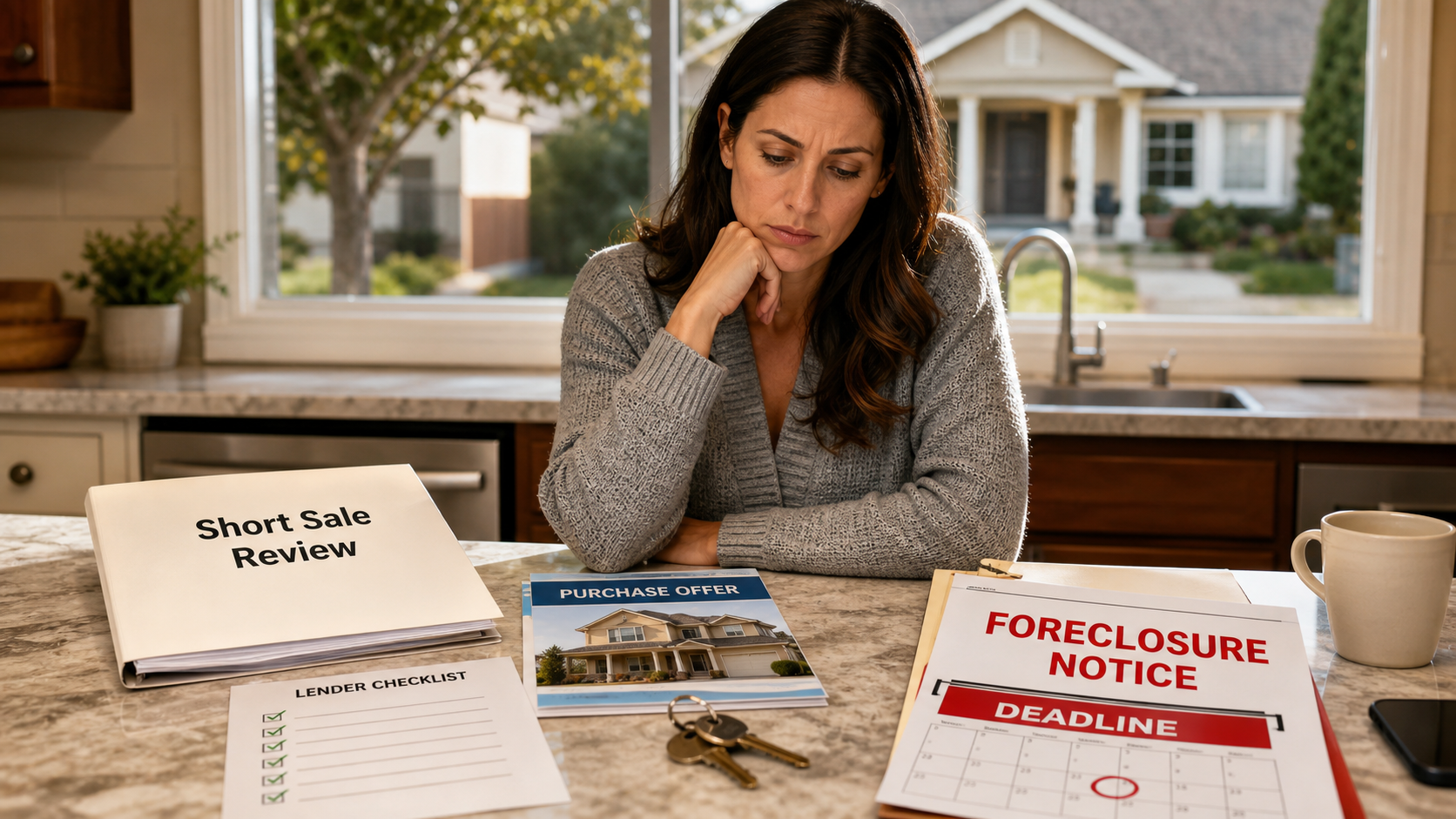

Why the Short Sale Approval Clock Keeps Resetting

Short sale approval clock keeps resetting? See what restarts lender review and how agents can keep the file moving before deadlines tighten.

Fast Answer

A short sale approval clock can reset when the lender, servicer, investor, mortgage insurer, or title reviewer needs updated information before it can keep reviewing the file. The most common reset triggers are stale seller documents, a changed buyer, a new offer term, a BPO value issue, missing title or lien information, a revised settlement statement, expired approval terms, or a foreclosure deadline that requires a new escalation.

The best fix is to stop treating submission as the finish line. Track what review stage is open, what document is about to expire, and what changed since the last lender review.

What To Do Next

- Ask the servicer which review stage is active right now.

- Confirm whether any seller financial documents are stale.

- Recheck the buyer, offer, closing date, and settlement numbers.

- Find out whether valuation, title, investor, or mortgage insurance review is still open.

- Have the short sale processor document the reset reason and next follow-up date.

Why the Clock Resets After Everyone Thinks the File Is Moving

Short sale approval time can feel unpredictable.

The seller signs the hardship package. The agent sends the contract. The buyer looks ready. The title company starts asking closing questions. Everyone assumes the lender review is finally moving.

Then the servicer asks for updated bank statements.

Or the buyer changes financing.

Or the BPO comes in too high.

Or title finds another lien.

Or the file gets sent to mortgage insurance.

Suddenly the short sale is not just waiting. The review clock has reset.

That reset is frustrating, but it is usually not random. It normally means something inside the file changed, expired, or moved into a new review layer.

For agents and sellers, the key question is not only, "How long do short sales take?"

The better question is, "What can restart the approval clock after the file has already been submitted?"

Submission Is Not the Same as Final Review

A short sale needs more than a buyer and a signed contract.

The mortgage servicer has to approve the sale because the sale proceeds will not fully pay the debt. If there are other mortgages or lienholders, they may also need to approve the transaction. The file may also involve the loan owner, investor rules, mortgage insurance, title clearance, settlement statement review, foreclosure timing, and final closing instructions.

That is why a submitted file can still be fragile.

The servicer may mark the package received, but that does not mean every review layer is complete. One stage can clear while another stage waits. One document can be accepted while another expires. One approval condition can be solved while a new closing issue appears.

This is where a short sale coordinator or short sale negotiator earns their keep. The job is not just uploading documents. The job is knowing which part of the file can still reset the timeline.

Reset Trigger 1: Seller Documents Went Stale

Short sale documents age quickly.

Bank statements, pay stubs, profit and loss statements, hardship letters, financial worksheets, tax documents, occupancy statements, and authorization forms may all need to stay current during review.

That creates a timing problem. The seller may have submitted a complete package on day one. But by the time the reviewer opens the file, those documents may no longer satisfy the current checklist.

The agent hears:

"We already sent that."

The servicer says:

"We need updated documents."

Both can be true.

The fix is to track document age before the servicer asks. If a file is likely to sit for several weeks, the short sale processor should know which items may expire and prepare the seller early.

Reset Trigger 2: The Buyer or Offer Changed

A short sale review is tied to the offer in front of the lender.

If the buyer changes, the price changes, the financing changes, the closing date changes, the earnest money changes, or a seller-credit request changes the net proceeds, the file may need another review.

That does not always mean starting from zero. But it can restart part of the lender's decision process.

The servicer may need to confirm:

- Is the buyer still qualified?

- Does the revised offer still meet investor requirements?

- Did the lender net change?

- Does the closing date still work?

- Does the approval letter need to be revised?

- Does the new contract still match the settlement statement?

Agents can reduce this risk by keeping buyer changes tight, documented, and explained. A revised offer should not arrive as a mystery. It should arrive with the support needed to keep review moving.

Reset Trigger 3: The BPO or Value Review Changed the File

Many short sales slow down because the lender is still deciding what the property is worth.

The lender may order a BPO, appraisal, automated value, investor review, or internal value check. If the value comes in higher than the offer, the file may pause while the lender counters, requests more support, or reviews a value dispute.

That can feel like a reset because the approval conversation changes.

The file is no longer just:

"Can this seller qualify for a short sale?"

It becomes:

"Does this offer make sense based on the lender's value?"

If the BPO value is wrong, the agent should not just wait. Strong value support may include repair estimates, property photos, condition notes, comparable sales, listing history, buyer feedback, inspection issues, and market data.

Related guide: short sale BPO value and appraisal issues: https://www.crispshortsales.com/the-short-sale-blog/bpo-vs-appraisal-short-sale-bank-value-changed.

Reset Trigger 4: Title or Lien Problems Appeared Late

Title can reset a short sale timeline even when the seller and buyer are ready.

A short sale may involve unpaid HOA dues, municipal liens, tax liens, judgments, second mortgages, HELOCs, old releases, probate authority, divorce orders, or missing signatures. If those issues are not found early, they can surface after the lender has already spent time reviewing the file.

That creates a practical problem:

The lender may be willing to approve the short sale, but the closing numbers or title clearance no longer work.

If a new lien appears, the settlement statement may need to change. If the settlement statement changes, lender net proceeds may change. If lender net proceeds change, the file may need another review.

This is why title should not be treated as a closing-week task in a short sale. It should be checked early enough to prevent a late reset.

Reset Trigger 5: Mortgage Insurance or Investor Review Is Still Open

Sometimes the servicer is not the only approval layer.

The loan owner, investor, or mortgage insurer may need to approve the short sale terms. That can create a second review path after the servicer intake looks complete.

Agents often do not see this clearly from the outside. They may only hear that the file is "under review." But internally, the question may have moved to a different party.

This matters because each layer may care about different details:

- Seller hardship.

- Offer price.

- Property value.

- Required net proceeds.

- Seller contribution.

- Closing costs.

- Deficiency language.

- Approval expiration date.

- Final settlement statement.

If the file moved into investor or mortgage-insurance review, ask what is open and what response is needed. Do not assume silence means nothing is happening.

Reset Trigger 6: The Settlement Statement No Longer Matches

Short sale approvals depend heavily on the numbers.

If the settlement statement changes, the lender may need to review the file again. That can happen when taxes update, HOA amounts change, title fees change, seller credits appear, buyer credits change, junior lien payments shift, closing costs move, or a new payoff is added.

Small changes can matter because the lender is reviewing what it will receive from the sale.

Before closing, compare:

- The contract.

- The approval letter.

- The settlement statement.

- Payoff information.

- Title and lien amounts.

- Any investor or servicer closing instructions.

If they do not match, fix the mismatch before the final closing push.

Reset Trigger 7: The Approval or Closing Window Expired

Even when a short sale is approved, the file is not finished until it closes.

Approval letters often include closing deadlines, net requirements, buyer conditions, seller conditions, document conditions, and language about what happens if the closing date changes.

If the buyer misses the deadline or the title company cannot close in time, the file may need an extension or a new approval letter.

That can reset review because the servicer may need to confirm that the buyer is still active, the numbers still work, and the investor still agrees.

This is why agents should treat the approval letter as a closing instruction document, not just a permission slip.

How Agents Can Keep the Approval Clock From Resetting

No agent can control every lender delay.

But agents can reduce preventable resets by building a file that stays current and by tracking each review layer.

Start with these checks:

1. Confirm the current review stage.

2. Track document expiration dates.

3. Keep the buyer package updated.

4. Watch BPO and valuation status.

5. Pull title issues early.

6. Keep the settlement statement aligned with the approval request.

7. Escalate foreclosure-deadline pressure before the file is out of time.

8. Document every request, response, and next follow-up date.

Related guide: why short sales stall after the file looks complete: https://www.crispshortsales.com/the-short-sale-blog/why-short-sales-stall-after-file-looks-complete.

When to Bring in Short Sale Help

If the file has reset once, it may reset again unless someone identifies the pattern.

A short sale specialist, processor, coordinator, or negotiator can help organize the package, track lender requests, watch title and valuation issues, communicate with the servicer, and keep the approval path from drifting.

That help matters most when:

- Foreclosure timing is active.

- The buyer is getting impatient.

- The lender keeps asking for updated documents.

- The BPO value is disputed.

- Title or lien issues are still unresolved.

- The approval letter has a tight closing window.

- The agent does not have time to track daily lender conditions.

If the deadline is already close, get short sale help before foreclosure: https://www.crispshortsales.com/start-short-sale while there is still time to move the file.

Bottom Line

Short sale approval time is not only about how fast the servicer works.

It is also about whether the file stays reviewable.

The approval clock can reset when documents expire, the buyer changes, the offer changes, the BPO value creates a dispute, title problems appear, mortgage insurance or investor review opens, settlement numbers shift, or the approval window expires.

The safest way to protect the timeline is to track what changed, what expired, and what review stage is still open.

That is how agents move from "we already sent everything" to "we know exactly what needs to happen next."

Short Sale Incentive Programs: What Blocks Seller Money

Short sale incentive money can help sellers move, but approval terms, occupancy, timing, and closing documents can block payment.

Short sale incentive programs can make a difficult move more manageable. For a seller who is already under foreclosure pressure, even a modest relocation payment can help with movers, storage, a rental deposit, utility setup, or the basic cost of leaving the home in good condition.

But agents and sellers should be careful with one assumption:

If incentive money exists, the seller will automatically receive it.

That is not how short sales work.

Short sale relocation assistance, move-out money, cash-for-keys style payments, and seller incentive programs usually depend on the loan type, investor, servicer, approval terms, occupancy status, closing documents, and timing. A seller can be in hardship and still be denied. A seller can qualify early and still lose the payment if the final approval or settlement statement is wrong.

Before anyone counts on the money, check the blockers.

The Approval Letter Has to Say More Than "Approved"

A short sale approval letter can approve the sale but still leave the seller with no incentive payment.

That is why the first check is simple: does the approval letter clearly allow the seller to receive money?

Look for language about short sale relocation assistance, incentive payment, transition assistance, seller proceeds, cash contribution, occupancy, closing costs, and disallowed payments. The amount should be clear. The payee should be clear. Any conditions should be clear.

If the approval letter is silent, vague, or says the seller cannot receive funds from closing, do not assume the payment can be added later.

The safest next step is to ask the servicer or authorized short sale contact in writing before closing. If the payment is approved, the file may need a corrected approval letter, written closing instruction, or settlement statement update.

Related guide: what the short sale approval letter must say about relocation assistance.

Occupancy Can Decide the Answer

Many short sale incentive programs are tied to the seller living in the property.

That means the seller may lose eligibility if the property is already vacant, rented, abandoned, occupied by someone else, or delivered in a condition that violates the approval terms.

Agents should confirm this before giving advice about moving out early. A seller may think leaving quickly shows cooperation, but in some files, moving before the right time can create a problem.

The practical question is not just:

Can this seller get incentive money?

The better question is:

Does this specific program require the seller to occupy the property through approval, closing, or a required move-out date?

If the answer is yes, the move-out plan should match the approval terms.

Seller Contributions Can Block the Payment

Some files require the seller to contribute cash toward the short sale. In those situations, incentive money can become more complicated.

Investor rules may prevent a seller from receiving relocation assistance if the seller is also required to make a cash contribution. There may be exceptions, but those exceptions usually need written approval.

This is where short sale files can become confusing. The seller may hear "relocation assistance" and "cash contribution" in the same conversation, but the two may conflict depending on the investor and file facts.

Do not try to solve that at the closing table. If the servicer is asking for seller contribution money, confirm whether that affects any relocation or incentive payment before final documents are prepared.

Outside Assistance Can Reduce or Eliminate Incentive Money

Some sellers may receive move-out help from another source. That can include government relocation assistance, employer relocation help, buyer concessions, third-party payments, or other transaction-related assistance.

Depending on the investor and program, outside assistance may reduce the incentive amount or make the seller ineligible for part of the payment.

That does not mean every outside payment is prohibited. It means the source and disclosure matter.

If money is connected to the transaction, the closing team and short sale negotiator should confirm whether it must be disclosed and whether it affects the lender-approved incentive.

Side payments are especially risky. If a payment is part of the deal, do not keep it informal. Get it reviewed before closing.

The Settlement Statement Has to Match

Even when incentive money is approved, it still has to be handled correctly in the closing documents.

The settlement statement should show the payment in the right amount, under the right description, and in a way that matches the approval letter and closing instructions. If the document is wrong, the lender may reject the final closing package or delay funding.

This is one of the most preventable problems in a short sale.

Before closing, compare:

- The approval letter.

- The settlement statement or closing disclosure.

- Any servicer closing instructions.

- Any investor-specific relocation or incentive conditions.

If they do not match, fix the mismatch before closing.

Late Requests Are Harder to Win

A seller may ask about move-out money after approval, especially if they are worried about paying for the move.

Sometimes a late request can still be reviewed. But it is harder once the servicer has approved final terms, issued a closing deadline, reviewed the net proceeds, and prepared closing instructions.

A late request is most likely to create a problem when:

- Closing is days away.

- The approval letter already says no seller proceeds are allowed.

- The settlement statement is locked.

- The buyer or title company is waiting on final approval.

- The incentive would reduce the lender's required net.

- The foreclosure deadline is close.

If incentive money matters to the seller, raise the issue before approval. That gives the short sale negotiator more room to document eligibility and request the payment correctly.

Related guide: asking for short sale move-out money after approval.

Program Names Can Be Misleading

Short sale incentive programs have changed over time. Some older programs ended, some investor rules changed, and different servicers may use different names for similar concepts.

That is why agents should avoid promising a seller a specific dollar amount based on something they saw online or handled years ago.

The current file controls the answer.

Loan type matters. Investor rules matter. Servicer authority matters. Occupancy matters. Approval-letter language matters. Closing documents matter.

If the seller needs the money to move, get the answer in writing early.

What Agents Should Check Before Promising Incentive Money

Before telling a seller they can count on short sale incentive money, check these items:

- What loan type is involved?

- Who is the investor or insurer?

- Does the servicer currently offer relocation or incentive money on this file?

- Does the seller still meet occupancy rules?

- Is the seller required to make a cash contribution?

- Is the seller receiving relocation help from another source?

- Is the amount written into the approval letter?

- Does the settlement statement show the payment correctly?

- Does the closing deadline leave enough time to correct mistakes?

- Has the payment been reconfirmed if terms changed?

If one of those answers is unclear, the seller should not make moving plans around the money yet.

The Safe Rule

Short sale incentive money is not real until it is approved in writing and matches the closing documents.

That may sound strict, but it protects everyone.

It protects the seller from counting on funds that may not be paid. It protects the agent from making a promise the lender will not honor. It protects the title company from closing with documents that do not match approval terms. It protects the buyer from a last-minute delay.

Short sale relocation assistance can be valuable. It can help a seller leave the home cleanly and move forward after a difficult financial stretch. But the details need to be handled before closing, not after the seller has already made commitments.

If a short sale file includes possible incentive money, review the approval terms early, confirm eligibility, and make sure the settlement statement matches before the deadline gets tight.

Crisp Short Sales helps agents and sellers review short sale approval terms, coordinate lender requirements, and avoid avoidable closing problems. If you need short sale help before the approval or move-out deadline gets too close, start the review early.

Related guide: short sale relocation assistance.

FAQ

Is short sale incentive money guaranteed?

No. Incentive money depends on the loan, investor, servicer, seller eligibility, occupancy, approval terms, and closing documents.

Why can short sale relocation assistance be denied?

It may be denied because the seller does not meet occupancy rules, the approval letter does not allow the payment, the seller is required to contribute cash, another source is providing assistance, or the settlement statement does not match the approved terms.

Does incentive money have to appear on the settlement statement?

In practical short sale closings, the payment should be disclosed correctly and match the lender's approval terms. If the approval letter and settlement statement do not match, the issue should be fixed before closing.

Short Sale BPO Rebuttal Package: What Evidence Works?

Bank value too high? See what evidence agents can send to challenge a short sale BPO and keep the approval moving.

What Is a BPO Rebuttal in a Short Sale?

A short sale can move smoothly for weeks and then suddenly stall because of one number: the bank's property value.

That value often comes from a BPO, or broker price opinion. If the BPO comes in too high, the lender may reject the offer, ask the buyer to increase, delay the approval, or hold the file open while the market moves around the deal.

The good news is that a high BPO is not always the end of the road. The bad news is that simply saying "the value is too high" usually does not help.

A stronger approach is to send a clean BPO rebuttal package that gives the lender specific reasons to question the value.

A BPO rebuttal is a value-challenge package sent to the lender or servicer when the short sale value appears too high for the property's real condition, location, market, or buyer pool.

The goal is not to argue emotionally. The goal is to make the lender's review easier.

A useful rebuttal answers three questions:

- What did the BPO likely miss?

- What evidence shows the property is worth less?

- Why is the current offer still the strongest realistic path to closing?

That means the package needs more than a short email. It should include photos, repair details, better comparable sales, market context, and a clear explanation of why the current BPO number may not match reality.

Start With the Property Condition

The first place to look is the property itself.

If the BPO relied on exterior photos, old listing photos, or broad neighborhood data, it may not reflect the true condition of the home. This matters in short sales because many properties have deferred maintenance, damage, occupancy issues, missing appliances, title delays, or repair problems that reduce buyer demand.

Strong condition evidence can include:

- Clear photos of damage or deferred maintenance

- Contractor estimates

- Inspection findings

- Agent notes from a walkthrough

- Buyer repair objections

- Photos showing outdated systems, flooring, roof issues, water damage, or safety concerns

The photos should be organized, not dumped into a messy attachment. Label the issue in plain English and explain why it affects value.

For example, "rear bedroom flooring damaged" is more helpful than "see attached photos."

If the file already has short sale BPO photos, use them as evidence instead of treating them as decoration. The lender needs to see what the valuation missed and why the buyer's offer may still be reasonable.

Use Comparable Sales That Match the Property

A common BPO problem is that the value is based on cleaner, newer, larger, or better-located homes.

Your rebuttal should show better comparable sales when possible. The best comps are recent, nearby, similar in size, similar in condition, and similar in buyer appeal.

If the BPO appears to use renovated homes while the short sale property needs repairs, point that out directly.

Useful comp notes include:

- Distance from the subject property

- Sale date

- Square footage

- Bedroom and bathroom count

- Condition differences

- Whether the comp was renovated or distressed

- Any location difference, such as a busy road, flood area, school zone, or neighborhood boundary

Do not overload the lender with every possible comp. A few strong, clean comparisons are better than a long list that makes the file harder to review.

The lender is looking for a reason to reconsider the number. Your job is to make that reason obvious.

Explain Buyer Reality

The lender may see a number on a report. The agent sees how buyers are reacting.

That market feedback can matter, especially when the property has already been exposed to buyers.

Include relevant buyer reality, such as:

- Days on market

- Showings with no offers

- Buyer repair concerns

- Low investor interest

- Financing issues caused by property condition

- Prior price reductions

- Offer history

The strongest point is simple: if the current buyer is the only serious buyer at a realistic price, the lender needs to understand that rejecting the offer may not produce a better result.

This is also why timing matters. Short sale BPO and appraisal delays can create a gap between what the lender thinks the property is worth and what the market is actually willing to pay.

Keep the Rebuttal Easy to Review

Short sale departments move through a lot of files. A rebuttal that is hard to understand may get ignored, delayed, or bounced back for more information.

A good package should be simple:

- One short cover letter

- A clean photo set

- A small group of better comps

- Repair estimates or condition notes

- The current offer summary

- A clear request for value review

The cover letter should not sound angry. It should sound useful.

A strong opening could be:

"The current BPO value appears to rely on comparable sales that do not reflect the property's repair condition. Attached are condition photos, repair notes, and recent comparable sales that support reconsideration of value."

That gives the lender a reason to keep reading.

What Not to Send

Some rebuttals fail because they create more confusion than clarity.

Avoid sending:

- Blurry photos

- Unlabeled repair pictures

- Old comps

- Comps from a different neighborhood

- Emotional hardship details unrelated to value

- Long arguments with no backup

- Huge attachments with no summary

- A demand that the lender accept the offer without evidence

The lender needs a reason to reconsider the BPO. Give them that reason quickly.

When to Send the Rebuttal

Send the rebuttal as soon as the value problem is clear.

Waiting too long can cause the buyer to walk, the foreclosure timeline to tighten, or the approval window to expire. If the file already has an offer, every extra week matters.

The short sale coordinator or negotiator should also confirm how the lender wants value disputes submitted. Some servicers want a specific form, portal upload, or escalation path. Others will accept a written rebuttal with supporting attachments.

This is where experienced short sale processing can help. The evidence is important, but so is getting it into the right channel before the file loses momentum.

If the BPO comes in too high, the next move should be organized proof, not a frustrated email.

The Bottom Line

A high BPO does not automatically end a short sale, but a weak response can make the problem worse.

The best BPO rebuttal package is clear, organized, and focused on evidence. Show the lender what the valuation missed, support the current offer with better market data, and make the review easy.

If the bank's value is too high, the next move is not panic. The next move is proof.

If you need help preparing or submitting a short sale value dispute, you can start the short sale process with Crisp Short Sales before a bad value review causes the buyer to walk.

Why Short Sales Stall After the File Looks Complete

Short sale file submitted but still stuck? See the hidden lender, title, value, and approval steps that can delay review after everything looks complete.

The File Looks Complete. So Why Is Nothing Happening?

This is one of the most frustrating moments in a short sale.

The seller signed the hardship package. The buyer submitted the offer. The agent sent the contract. The financial worksheet is in. The payoff numbers have been requested. Everyone thinks the hard part is done.

Then the file sits.

No approval.

No clear answer.

No clean next step.

This is why so many agents ask the same question: why do short sales take so long after everything has already been submitted?

The answer is that a short sale package can be complete at the document level but unfinished at the review level. Those are not the same thing.

"Submitted" Does Not Mean "Approved"

In a normal transaction, sending a complete package often feels like the finish line.

In a short sale, it is closer to the starting line for lender review.

Once the servicer receives the short sale package, the file may still need to pass through several internal checkpoints. Depending on the loan, investor, insurer, and file history, that may include:

- Document intake review.

- Seller hardship review.

- Valuation or BPO review.

- Investor review.

- Mortgage insurance review.

- Title and lien review.

- Buyer and offer review.

- Final approval-letter drafting.

The file can be "complete" for intake but still waiting on one of those steps.

That is why short sale processing is not just about uploading documents. The real work is tracking what stage the file is in, what condition is open, and what response will move it forward.

Delay 1: The Documents Are Complete But Not Current

Short sale documents age quickly.

A bank statement that was current when the file was first submitted may be stale by the time the reviewer opens the file. Pay stubs, profit and loss statements, financial worksheets, hardship letters, buyer proof of funds, and estimated settlement statements can all need updates.

This is where a file starts to feel circular.

The agent says, "We already sent that."

The servicer says, "We need updated versions."

Both can be true.

The fix is to track document expiration dates before the servicer asks again. A short sale processor should know which items are likely to expire and refresh them before review resets.

Delay 2: The File Is Waiting On Valuation

Many short sales stall because the lender has not finished deciding what the property is worth.

That value may come from a BPO, appraisal, automated valuation, investor review, or a combination of those inputs. If the short sale BPO value comes in higher than the offer, the lender may counter, pause, or ask for more support.

This does not always mean the offer is dead.

It does mean the file needs evidence.

Helpful evidence may include:

- Clear property photos.

- Repair estimates.

- Condition notes.

- Comparable sales.

- Listing history.

- Buyer feedback.

- Market data that supports the offer.

If the value issue is not identified early, everyone may think the lender is simply slow. In reality, the approval may be waiting on a number nobody has challenged yet.

Delay 3: Investor Review Is Still Pending

The servicer is often not the final decision-maker.

The company collecting documents and communicating with the agent may be servicing the loan for another investor. That investor may have its own rules for hardship, net proceeds, offer terms, seller contributions, closing costs, relocation assistance, or deficiency language.

This matters because a servicer can say the file is under review even when the decision is waiting somewhere else.

A good short sale negotiator should ask whether investor review is required, whether it has started, and whether any investor-specific conditions are open.

If the answer is vague, keep pushing for the active stage.

"Under review" is not enough.

Delay 4: Mortgage Insurance Has A Separate Say

Some loans have mortgage insurance involved. When they do, the mortgage insurance company may need to approve the short sale terms.

That can create a second layer of review.

The servicer may be comfortable with the package, but the mortgage insurance review may still be pending. This can affect seller contribution requests, closing costs, deficiency language, or approval timing.

That is why mortgage insurance can make a file feel complete but still stuck.

The best move is to identify it early. Ask whether mortgage insurance is involved and whether the file has been sent for that review.

Delay 5: Title Is Not Actually Clear

Title problems often appear late because everyone focuses on the lender first.

But a short sale approval letter is not enough if title cannot close.

Common title-related issues include:

- Junior liens.

- HOA balances.

- Tax liens.

- Judgment liens.

- Incorrect payoff figures.

- Missing releases.

- Probate or heirship issues.

- Name or ownership problems.

If title is not clean, the file may stall even after the lender has most of what it needs.

This is why title review should not wait until the approval letter arrives. If a lien problem is hiding in the file, it needs to be handled while the lender review is still moving.

Delay 6: The Buyer Or Offer Changed

Short sales take time, and buyers do not always stay still.

The buyer's lender may update requirements. Proof of funds may expire. The closing date may need to move. The buyer may ask for a credit or repair. The contract may need an addendum.

Any change can affect the short sale review.

The lender approved, or is considering, a specific deal. If the deal changes, the review may need to be updated.

That does not mean every buyer change kills the file. It means the change needs to be submitted cleanly, with the settlement statement and supporting documents matching the new terms.

Delay 7: Approval Letter Conditions Are Not Ready

Sometimes the file is close to approval, but the final letter is not ready because the lender is checking conditions.

The short sale approval letter may need to confirm:

- Approved sale price.

- Approved closing costs.

- Closing deadline.

- Seller contribution terms.

- Deficiency language.

- Relocation assistance terms.

- Junior lien payoff limits.

- Required buyer or title conditions.

If those terms are wrong, vague, or missing, the file can still be delayed.

This is why the approval letter should be reviewed carefully before everyone celebrates. A weak approval letter can create closing problems after the lender finally says yes.

What Agents Should Ask Instead Of "Do You Have Everything?"

"Do you have everything?" is not a strong enough question.

The answer may be yes, even if the file is not moving.

Better questions include:

- What review stage is active right now?

- Is the file in document review, valuation review, investor review, mortgage insurance review, or final approval?

- Are any documents expired or about to expire?

- Has the BPO or appraisal value been received?

- Is title review complete?

- Are there any open approval-letter conditions?

- What is the next follow-up date?

- What exact item would move the file forward today?

Those questions force the file out of vague status updates and into real next steps.

How A Short Sale Coordinator Keeps The File Moving

A short sale coordinator does not just send paperwork.

The coordinator keeps the moving pieces from drifting apart.

That includes tracking deadlines, matching documents, watching stale dates, following up with the servicer, flagging title issues, checking the buyer package, and making sure approval conditions are answered before they become emergencies.

The role matters because short sale files rarely fail all at once. They usually slow down one small missing item at a time.

When nobody owns the follow-up, those small items turn into weeks of delay.

When To Bring In Short Sale Help

Bring in short sale help when the file has been submitted but nobody can explain what is still pending.

That is the sign that the problem may not be missing paperwork. It may be unclear file control.

A short sale processor or short sale negotiator can help identify whether the blocker is:

- Document freshness.

- Hardship review.

- BPO value.

- Investor review.

- Mortgage insurance.

- Title.

- Buyer changes.

- Approval-letter conditions.

Once the real blocker is named, the file has a better chance of moving.

Bottom Line

A short sale can look complete and still be stuck.

That does not mean the deal is hopeless. It usually means the active review stage has not been identified clearly enough.

The best next move is not to resend the same documents blindly. It is to find the exact stage, condition, or approval layer that is holding the file in place.

That is how agents turn "we submitted everything" into a real plan for getting the short sale reviewed, approved, and closed.

Short Sale Hardship Letter Mistakes That Make Lenders Pause

Short sale hardship letter weak or vague? See the mistakes that make lenders pause and what to fix before the file loses time.

Why The Hardship Letter Still Matters

A hardship letter is not the only document in a short sale package.

The lender or servicer may also review bank statements, pay stubs, tax documents, a financial worksheet, the purchase contract, buyer proof, title issues, payoff figures, and an estimated settlement statement.

But the hardship letter still matters because it gives the file a story the reviewer can understand.

The lender is being asked to approve a sale for less than the full payoff. That means the file should explain why the seller cannot solve the problem through a regular payoff, normal sale, reinstatement, refinance, repayment plan, or other option.

A good hardship letter does not guarantee approval.

A weak one can still slow the file down.

Mistake 1: The Letter Is Too Vague

The most common problem is a letter that says only:

- "I cannot afford the home."

- "I need to sell."

- "The market changed."

- "Please approve the short sale."

That may be true, but it does not give the servicer much to review.

A stronger letter explains what happened, when it started, and why the seller cannot recover enough to keep the home or pay the mortgage in full.

Examples may include job loss, reduced income, divorce, medical costs, death in the family, business failure, relocation, increased expenses, expired assistance, or a property-value drop that makes a regular sale impossible.

The point is not to write a dramatic story. The point is to make the hardship understandable.

Mistake 2: The Letter Does Not Match The Financials

The hardship letter should line up with the rest of the short sale package.

If the letter says the seller lost income, the financial worksheet and income documents should not tell a totally different story. If the seller says medical expenses changed everything, there should usually be some supporting detail. If the seller says the property cannot sell high enough to pay the loan, the estimated settlement statement should show the shortage.

This is where short sale processing matters.

A short sale processor should not treat the hardship letter as a standalone document. It should be checked against the financial worksheet, bank statements, pay stubs, listing information, offer, title costs, and payoff numbers.

When the documents conflict, the reviewer may ask for clarification or updated paperwork. That means more time lost.

Mistake 3: The Letter Blames Only The Market

A low property value can be part of the hardship, but it is usually not the whole story.

If the seller simply says, "The home is worth less than I owe," the servicer may still need to know why the seller cannot keep making payments or otherwise resolve the debt.

The stronger approach is to connect the market problem to the seller's actual situation.

For example:

- The property value is below the loan balance.

- The seller cannot bring money to closing.

- The seller's income or expenses changed.

- The seller needs to sell because of a real life event.

- The current offer may prevent a worse foreclosure outcome.

That is different from saying, "The market is bad, so approve the sale."

Mistake 4: The Letter Is Too Emotional And Not Specific Enough

Short sales are stressful. The seller may be exhausted, embarrassed, angry, or scared.

It is okay for the hardship letter to sound human.

But the letter should still stay focused on facts the servicer can use.

A letter filled with frustration but light on dates, numbers, and events may not help the file. The servicer does not need a long argument. The servicer needs a clear explanation that fits the documents.

Good hardship letters usually answer:

- What changed?

- When did it change?

- Is the hardship temporary or ongoing?

- Why can the seller not catch up or pay off the loan?

- Why is a short sale being requested now?

That is enough.

Mistake 5: The Letter Leaves Out The Timeline

Timing matters in a short sale.

The servicer may need to know when the hardship started, when payments became difficult, whether the seller has already tried other options, and whether a foreclosure deadline is active.

A timeline helps the reviewer understand the file.

For example, a seller who lost income six months ago, used savings to keep paying, listed the property, accepted a market offer, and still cannot cover the payoff is telling a clearer story than a seller who simply says, "I need help."

The timeline does not need to be complicated.

One short paragraph can explain the sequence.

Mistake 6: The Letter Overpromises

A hardship letter should not promise things the seller cannot deliver.

Do not say the seller can make a contribution unless that has been reviewed. Do not say the seller can close by a specific date unless the buyer, title, lender, and approval process support it. Do not say all liens are resolved if title has not confirmed that yet.

Short sale files can be delayed when the letter creates expectations that the documents do not support.

Keep the letter honest and practical.

Mistake 7: Nobody Reviews It Before Submission

Many hardship letters are written quickly because everyone is trying to get the package submitted.

Speed matters, but sending a weak or inconsistent letter can create extra requests later.

Before submission, the short sale negotiator or processor should check:

- Does the letter explain the hardship clearly?

- Does it match the financial documents?

- Does it avoid unnecessary drama or unsupported claims?

- Does it include the seller's current situation?

- Does it support the reason a short sale is needed?

- Is it signed and dated if the servicer requires that?

That review can prevent a simple document from becoming another reason the file sits.

What A Strong Hardship Letter Usually Includes

A strong short sale hardship letter usually includes:

- Seller name and property address.

- Clear hardship explanation.

- Approximate date the hardship began.

- Current financial impact.

- Why the seller cannot keep the home or pay the shortage.

- Why a short sale is being requested.

- A short request for lender review.

- Signature and date if required.

It should be direct. One page is usually enough for most files.

The hardship letter is not supposed to replace the rest of the package. It should make the rest of the package easier to understand.

How This Affects Short Sale Approval Time

A clear hardship letter helps the file move because the reviewer can understand the request faster.

A weak letter can trigger more questions:

- What is the actual hardship?

- Is the hardship still active?

- Why can the seller not pay?

- Why does the financial worksheet look different?

- Is this a short sale request or just a low offer?

Those questions can add days or weeks, especially if other parts of the file are already slow.

If you are dealing with a file that is sitting, it may also help to review why short sale approval takes so long and check whether the issue is hardship, valuation, title, buyer proof, investor review, or missing documents.

When To Get Help

Bring in short sale help when the seller cannot cover the payoff, the documents are incomplete, foreclosure pressure is building, title has issues, or the agent does not have time to manage every servicer request.

A short sale processor can help organize the package.

A short sale negotiator can help communicate with the servicer, track review stages, respond to conditions, and keep the file from drifting.

The hardship letter is only one piece, but it should not be treated casually. It is the seller's clearest explanation of why the lender is being asked to approve the short sale.

Bottom Line

A short sale hardship letter does not need to be perfect writing.

It needs to be useful.

Make it clear, specific, honest, current, and consistent with the financial documents. Avoid vague statements, unsupported promises, and emotional paragraphs that do not explain the file.

When the letter helps the reviewer understand the hardship, the rest of the short sale package has a better chance of moving without avoidable delays.

FAQ

What should a short sale hardship letter include?

It should include the seller's hardship, when it started, why it affects the ability to keep the home or pay the full mortgage balance, and a clear request for short sale review.

Can a weak hardship letter delay a short sale?

Yes. If the letter is vague, inconsistent, unsigned, outdated, or unsupported by the financial documents, the servicer may ask for clarification or updated paperwork.

How long should a short sale hardship letter be?

Most hardship letters should be about one page. The goal is not length. The goal is a clear explanation that fits the rest of the short sale package.

Should the hardship letter match the financial documents?

Yes. The letter should match the financial worksheet, bank statements, income documents, payoff numbers, and estimated settlement statement. Conflicting documents can slow review.

What Is a Short Sale in Real Estate When Foreclosure Is Already Scheduled?

Foreclosure scheduled? Learn what a short sale is, when lender approval can still work, and what to move first before time runs out.

Fast Answer

A short sale in real estate happens when a homeowner sells the property for less than the full mortgage payoff and the mortgage servicer approves the sale. If foreclosure is already scheduled, a short sale may still be possible, but it is not automatic. The seller needs a real buyer, a complete short sale package, servicer approval, and enough time before the foreclosure deadline to review and close the file.

What To Do Next

• Confirm the foreclosure sale date, court date, or trustee sale deadline.

• Ask the mortgage servicer whether short sale review is still available.

• Gather the hardship letter, financial documents, listing agreement, offer, buyer proof, and estimated closing statement.

• Check for title issues, second mortgages, HOA balances, taxes, or liens before approval.

• Get short sale help before the file loses the time needed for lender review.

Why This Search Usually Means The Clock Is Running

When someone searches "what is a short sale in real estate," they may be asking a simple definition question.

But in real life, that question often comes up late.

The homeowner may have missed payments. A foreclosure notice may have arrived. The agent may have a buyer, but the payoff is higher than the market value. The seller may be trying to avoid foreclosure but does not know whether a regular sale can still work.

That is where the definition matters.

A short sale is not just a discounted sale. It is a lender-approved sale for less than the amount owed. That means the homeowner, agent, buyer, title company, mortgage servicer, investor, and sometimes junior lienholders all have to move in the right order.

If foreclosure is already scheduled, the short sale question becomes urgent: is there still enough time for the lender to review and approve the sale before the foreclosure process finishes?

What Is A Short Sale In Real Estate?

A short sale is a real estate sale where the property sells for less than the total mortgage debt, and the lender agrees to accept the sale terms so the transaction can close.

The homeowner cannot force a short sale by accepting a low offer. The lender or mortgage servicer has to approve it because the sale will not pay the loan in full.

The Consumer Financial Protection Bureau explains that with a short sale, the homeowner is responsible for finding a buyer, needs mortgage servicer approval, and may also need approval from other mortgage servicers if there are additional loans on the property.

That is the practical difference between a regular sale and a short sale.

In a regular sale, the purchase price is high enough to pay the liens and closing costs.

In a short sale, the numbers do not fully pay everyone, so the lender has to decide whether approving the sale is better than continuing toward foreclosure.

What Changes When Foreclosure Is Already Scheduled?

Foreclosure changes the timeline.

If no foreclosure deadline exists yet, there may be more time to list the property, collect documents, negotiate with the servicer, handle value issues, and fix title problems.

When foreclosure is already scheduled, every delay matters more.

The lender may still review a short sale, but the file usually has to be complete and credible. That means the servicer needs more than a vague promise that "we might have a buyer."

The file should show:

• The seller has a hardship.

• The property is listed or under contract.

• The buyer is real and can close.

• The offer makes sense for the market.

• The estimated closing statement is realistic.

• Title and lien issues are known.

• The seller has authorized the short sale team to speak with the servicer.

• The foreclosure deadline has been identified.

Foreclosure does not always happen overnight, and HUD encourages homeowners at risk of foreclosure to contact a HUD-approved housing counselor. But once a deadline is active, the safest approach is to treat the date as real while checking whether short sale review is still available.

Does A Short Sale Stop Foreclosure Automatically?

No.

A short sale does not automatically stop foreclosure just because the seller wants one, the property is listed, or a buyer has made an offer.

The mortgage servicer still has to open the file, review the package, order or review valuation, check investor rules, evaluate the settlement numbers, and issue written approval. If the foreclosure deadline is close, the servicer may also need to decide whether it will postpone the foreclosure sale while reviewing the short sale.

That is why timing is the first issue.

Before assuming the short sale will stop foreclosure, confirm:

• Has the servicer opened a short sale review?

• Is the package complete?

• Has a negotiator been assigned?

• Has the value review started?

• Is there a sale date or court date?

• Has anyone requested postponement if needed?

• Is the buyer still willing and able to close?

If those answers are unclear, the file is not controlled yet.

Who Has To Approve A Short Sale?

The first mortgage servicer usually leads the review, but other parties may also have approval rights.

Depending on the file, approval may involve:

• The first mortgage servicer.

• The loan investor.

• Mortgage insurance.

• A second mortgage or home equity line.

• HOA or condo association balances.

• Tax liens or judgment creditors.

• A probate, divorce, bankruptcy, or estate issue.

This is one reason short sales can feel slow. The listing agent may have a buyer. The seller may be cooperative. The title company may be ready to help. But if a second lienholder, mortgage insurer, or title issue is not handled, the file can still stall.

The approval letter is also critical. It should state the approved sale price, closing deadline, allowed costs, seller contribution if any, relocation terms if any, and deficiency language.

If foreclosure is close, do not wait until the closing table to read those terms.

What Documents Usually Matter First?

Every servicer can have its own process, but a short sale package often includes:

• Written authorization to speak with the lender.

• Hardship letter.

• Financial worksheet.

• Recent bank statements.

• Pay stubs, income proof, or unemployment documentation.

• Tax returns or tax transcript forms when required.

• Listing agreement.

• Purchase contract.

• Buyer proof of funds or pre-approval.

• Estimated settlement statement.

• Payoff statements.

• HOA, tax, title, and junior lien information.

The package should be clean, current, and consistent. If the hardship letter says one thing and the financial documents say another, the file may get delayed. If the buyer proof is expired, the file may get delayed. If the estimated settlement statement leaves out a lien or HOA balance, the file may get delayed.

Those delays matter when foreclosure is already scheduled.

When A Short Sale May Still Work

A short sale may still work after foreclosure has started when the core pieces are strong.

The property is worth less than the payoff. The seller has a real hardship. There is a buyer or a fast path to one. The seller can provide documents. Title problems can be identified. The buyer can wait for approval. The servicer will still review the file. There is enough time to make a serious postponement or approval request before the foreclosure date.

None of that guarantees approval.

But it gives the file something the lender can evaluate.

A short sale specialist or short sale negotiator helps by organizing the package, tracking missing items, communicating with the servicer, watching deadlines, and pushing the file toward a written decision.

That work is especially important when the seller is no longer operating with a comfortable timeline.

When It May Be Too Late

A short sale may be too late if the foreclosure sale is imminent, the servicer will not review or postpone, the seller cannot provide documents, there is no buyer, the buyer cannot close, title issues cannot be solved, or the numbers do not make sense.

This is why homeowners should not wait for the last notice before asking for help.

Even if a short sale is not possible, the homeowner may still need legal, housing counseling, tax, or credit guidance. A short sale professional can help with the sale and lender-submission side, but state-specific foreclosure rights and legal defenses should be discussed with a qualified attorney.

Short Sale Vs Foreclosure: The Practical Difference

The practical difference is control.

With a short sale, the homeowner may still be able to participate in the sale process, work with a buyer, seek lender approval, clarify deficiency language, and close before foreclosure finishes.

With foreclosure, the lender's process controls more of the outcome.

That does not mean a short sale is painless. It can still affect credit. It can still involve tax questions. It still requires lender approval. It still means the homeowner is leaving the property.

But when it works, a short sale can give the homeowner a more organized exit than simply letting the foreclosure process finish.

For a deeper comparison, read the short sale vs foreclosure guide and the 7-day checklist. Those pieces help homeowners compare the risks after they understand what a short sale actually is.

The Bottom Line

A short sale in real estate is a lender-approved sale for less than the mortgage payoff.

If foreclosure is already scheduled, the short sale question is not just "what does it mean?"

The real question is: can the file still be submitted, reviewed, approved, and closed before the foreclosure deadline takes over?

That depends on timing, documents, buyer strength, title issues, servicer rules, investor rules, and whether someone is actively coordinating the file.

If you need short sale help before foreclosure, start with the deadline. Confirm the sale date, call the servicer, gather the package, check the liens, and get the review moving before the clock makes the decision for you.

Crisp Short Sales helps homeowners, listing agents, and investors organize short sale files, communicate with servicers, track missing documents, and negotiate short sale approvals before deadline pressure breaks the deal.

Georgia Short Sale Timeline Before Foreclosure: What to Move First

Georgia foreclosure date coming up? See what must move first so a short sale has a real chance before the auction clock runs out.

Georgia foreclosure deadlines can feel sudden because the final sale date is not a vague future threat. In Georgia, foreclosure sales are generally tied to a specific auction schedule, and once the sale happens, the short sale window may close fast.

That does not mean every file is too late. It does mean the short sale has to be handled in the right order.

If you are a homeowner, listing agent, or short sale processor trying to help a Georgia seller before foreclosure, the goal is simple: build a complete short sale file quickly enough for the servicer to review it before the sale date becomes the controlling problem.

Why Georgia Short Sale Timing Feels So Tight

Georgia is commonly a nonjudicial foreclosure state, which means many foreclosures can move without a long court process. That is why a seller may go from "we are behind" to "there is a sale date" faster than expected.

The Georgia Attorney General explains that foreclosure sales take place at the county courthouse on the first Tuesday of the month between 10:00 a.m. and 4:00 p.m. Georgia law also requires foreclosure notice to the debtor no later than 30 days before the proposed foreclosure sale, and foreclosure sale advertising generally has to run once a week for four consecutive weeks.

For a short sale, that timing matters because the lender is not just deciding whether the seller has a hardship. The lender is reviewing an offer, payoff numbers, investor rules, title issues, seller documents, buyer proof, and closing feasibility before the auction date.

If any one of those pieces is missing, the file can stall.

The First 48 Hours: Confirm The Sale Date And File Status

The first move is not pricing. It is not marketing. It is not calling five different people for opinions.

The first move is confirming the real deadline.

Ask for the foreclosure notice, the lender or servicer name, the loan number if available, the attorney or trustee contact information, and any sale date listed in the documents. If the homeowner only knows that foreclosure is "soon," treat that as incomplete information until the date is verified.

At the same time, find out whether the seller has already submitted a short sale package, whether a previous buyer walked away, whether there is an active offer, and whether the lender has assigned a negotiator.

This is where short sale assistance becomes practical. A file with no offer, no hardship package, and no sale-date confirmation is in a very different position from a file with a complete package and a buyer waiting for approval.

Days 1-3: Gather The Seller Package

A Georgia short sale can lose precious time if the seller package comes in pieces. The servicer may ask for updated documents, but the first submission should be as complete as possible.

Common short sale package items include:

• Seller authorization

• Hardship letter

• Financial worksheet

• Recent bank statements

• Pay stubs or income proof

• Tax returns or tax transcripts if required

• Listing agreement

• Purchase contract

• Buyer proof of funds or pre-approval

• Estimated settlement statement

• HOA, lien, or payoff details if known

The exact list can vary by servicer, investor, loan type, and file history. The key is not to guess. Ask the servicer what is required and submit a clean package that matches their process.

Days 3-7: Check Title, Liens, HOA, And Payoff Problems

Many short sale files do not fail because the seller had no hardship. They fail because a hidden closing issue shows up too late.

Before waiting on the lender, check for title problems, judgment liens, HOA balances, second mortgages, tax liens, open permits, or unpaid municipal items. In Georgia, these problems matter because the sale date may leave very little room for late corrections.

This is also where a short sale coordinator or processor can protect the file. Someone needs to track each payoff, each authorization, each third-party demand, and each settlement statement revision before the lender says yes.

If the approval comes with a narrow closing window and the title work is not ready, the file can still fall apart.

Days 7-14: Push For A Real Servicer Review

Once the package is submitted, the next job is to avoid passive waiting.

The servicer needs to confirm the file is open, complete, assigned, and moving toward valuation or investor review. If the file is missing documents, get the missing items immediately. If a negotiator is assigned, keep the communication organized and documented.

For agents, this is where the difference between "we sent it in" and "the file is actually under review" matters.

A Georgia foreclosure date creates urgency, but urgency alone does not force approval. The file still has to be complete enough for the servicer to make a decision.

Days 14-30: Watch The Auction Date And Escalate Carefully

As the sale date gets closer, the key question becomes whether the servicer has enough to postpone foreclosure while reviewing the short sale.

Not every servicer, investor, or file will qualify for postponement. But if a complete short sale package, valid offer, buyer proof, hardship documentation, and title path are already in place, the case for review is much stronger.

If the sale date is approaching and the file is still sitting, escalation may be needed. Keep the message simple:

• The property is in Georgia.

• The foreclosure sale date is approaching.

• A short sale offer has been submitted.

• The package is complete or the missing items are identified.

• The seller is requesting review before the sale.

This is not the moment for scattered calls or unclear updates. It is the moment for clean documentation.

What Usually Delays A Georgia Short Sale

The most common delays are predictable:

• The foreclosure sale date was not confirmed early.

• The seller package was incomplete.

• The buyer proof was weak or expired.

• The estimated settlement statement did not match lender expectations.

• A second lien, HOA payoff, or judgment appeared late.

• The listing price did not match the lender's valuation.

• No one followed up after submission.

Most of these are preventable if the file is organized from day one.

Can A Short Sale Stop A Georgia Foreclosure?

Sometimes a short sale can help avoid foreclosure, but it depends on timing, servicer rules, investor requirements, documentation, and whether the lender agrees to postpone or approve the sale.

No article can promise that a foreclosure will be stopped. The safest approach is to treat the sale date as real while building the short sale file as quickly and completely as possible.

If you are already close to the auction date, talk with a qualified Georgia attorney about legal options. A short sale professional can help with the lender and transaction side, but legal rights and foreclosure defenses should be reviewed by an attorney.

The Simple Priority List

If a Georgia foreclosure deadline is already in play, move in this order:

Confirm the sale date and servicer status.

Get written authorization to speak with the lender.

Gather a complete seller hardship package.

Confirm the buyer's offer and proof.

Check title, liens, HOA, and payoff issues.

Submit a clean package.

Confirm the file is complete and assigned.

Track the sale date and escalate before it is too late.

That order matters. A short sale is not just one phone call to the bank. It is a timed file-management process.

Need Georgia Short Sale Help Before Foreclosure?

Crisp Short Sales helps agents and homeowners organize short sale files, communicate with servicers, track missing documents, and negotiate a short sale when time matters.

If a Georgia foreclosure date is already on the calendar, do not wait for the file to become easier. The safest next step is to confirm the deadline, gather the package, and get the short sale review moving now.

Short Sale vs Foreclosure Pros and Cons in 2026

Compare short sale vs foreclosure pros and cons in 2026, including credit, timing, deficiency risk, and when short sale help may still work.

Fast Answer

Short sale vs foreclosure comes down to control, timing, credit impact, possible deficiency risk, and whether the lender will still review a sale before foreclosure finishes. A short sale may let the homeowner sell with lender approval and avoid the foreclosure sale, but it takes a complete package, a real buyer, and enough time. Foreclosure may feel simpler because no sale negotiation is required, but it usually gives the homeowner less control over timing, credit reporting, move-out pressure, and the final outcome.

What to do next

- Confirm the foreclosure deadline, payoff, and loan status before comparing options.

- Ask the servicer whether short sale review is still available.

- Check title, liens, HOA balances, and deficiency language early.

- Get short sale help before the foreclosure date becomes the only timeline.

Why This Decision Feels So Heavy

Most homeowners do not compare short sale vs foreclosure in a calm moment.

They compare them after missed payments, stressful letters, awkward servicer calls, and maybe a foreclosure date that is already on the calendar.

That pressure can make the options blur together. Both paths may involve leaving the home. Both can affect credit. Both can create stress for the homeowner and family.

But they are not the same path.

A short sale is a negotiated sale. Foreclosure is the lender's legal process to take back the property after default. The difference is not only what happens to the house. The difference is how much control the homeowner may still have before the outcome becomes final.

What Is a Short Sale?

A short sale happens when the lender agrees to let the property sell for less than the full mortgage payoff.

The homeowner does not simply decide to sell short. The lender, investor, mortgage insurer, and sometimes junior lienholders must approve the deal. The servicer usually reviews the hardship, offer, property value, closing costs, payoff numbers, title issues, and whether the proposed sale makes more sense than foreclosure.

That makes a short sale a process, not just a listing strategy.

It can work when the homeowner has a real hardship, the home is worth less than the debt, there is a serious buyer, and there is enough time to submit a complete package before the foreclosure date gets too close.

What Is Foreclosure?

Foreclosure is the legal process where the lender moves to take back the property after default.

The process varies by state. Some states use court foreclosure. Others use a trustee sale process. Either way, once foreclosure moves far enough, the homeowner can lose control over timing and the final result.

The Consumer Financial Protection Bureau says foreclosure can hurt credit and that foreclosure information generally remains on a credit report for seven years from the foreclosure date. The CFPB also says most negative credit information can generally be reported for seven years.

That does not mean a short sale has no credit impact. Missed mortgage payments and settled debt can still affect credit. But foreclosure usually creates a different kind of event than a negotiated sale.

Short Sale Pros

The biggest advantage of a short sale is control.

With a short sale, the homeowner may be able to stay involved in the process, review offers, work toward an approved closing, and avoid the property going all the way through foreclosure.

A short sale may also help clarify whether the lender is waiving or preserving the right to pursue a deficiency. That language matters. The approval letter should be reviewed carefully before closing so the homeowner understands what the lender is agreeing to and what conditions still apply.

A short sale can also help agents and buyers keep a transaction alive when the payoff is higher than the market value. If the numbers are supported and the file is complete, the lender may decide that approving the sale is better than taking the property through foreclosure.

For some loans, investor or servicer guidelines may allow specific short sale review paths, relocation assistance, or deficiency treatment when the file meets the rules. Fannie Mae's servicing guide, for example, includes short sale review, borrower package, valuation, subordinate lien, relocation, and deficiency-waiver requirements for certain loans.

The key is that the file has to be handled correctly.

Short Sale Cons

A short sale is not instant.

The lender has to review the file. If there are multiple loans, mortgage insurance, HOA balances, tax liens, title issues, buyer delays, or value disputes, the process can take longer than expected.

A short sale also does not automatically remove every risk.

The approval letter matters. Homeowners need to understand whether the lender is waiving the deficiency, requiring a contribution, issuing tax forms, or placing conditions on closing.

Another downside is that several parties have to cooperate. The buyer must stay patient. The agent must price and submit the file correctly. The servicer must review it before the foreclosure clock runs out.

That is why short sale help matters most when the case is already under pressure.

Foreclosure Pros

Foreclosure may feel simpler because the homeowner does not have to negotiate a sale, manage a buyer, or gather a full short sale package.

For some homeowners, especially those with no realistic buyer, no time left, no ability to cooperate, or legal defenses being handled by an attorney, foreclosure may seem like the only path left.

But simpler does not always mean better.

It usually means the homeowner has less control over the result.

Foreclosure Cons

The major downside of foreclosure is loss of control.

The lender controls the process. The sale date can move forward. The homeowner may have fewer chances to negotiate terms. Credit damage, public records, deficiency risk, moving pressure, and future housing issues can all become part of the fallout.

The CFPB notes that foreclosure hurts credit and can remain on a credit report for seven years. That is one reason many homeowners at least explore a short sale before assuming foreclosure is unavoidable.

Foreclosure can also create emotional and practical stress. Families may have less control over move-out timing, communication, and the final handling of the home.

Which Option Is Better?

The better option depends on timing and facts.

A short sale may be better when:

- The home is worth less than the mortgage balance.

- There is a serious buyer or time to find one.

- The homeowner has a hardship.

- The foreclosure date is not too close.

- The lender is still willing to review a short sale.

- Deficiency language can be negotiated or clarified.

- Title and lien problems can be resolved before closing.

Foreclosure may become more likely when:

- There is no time left before the sale date.

- The homeowner cannot gather required documents.

- The buyer walks away.

- The lender will not postpone foreclosure.

- Legal or bankruptcy issues take priority.

- The property cannot close because of title, lien, or occupancy problems.

The mistake is waiting until the last few days to ask which option is better. By then, the real question may be whether there is enough time for any short sale review at all.

The Real 2026 Decision Point

In 2026, homeowners are not just asking, "Is a short sale better than foreclosure?"

They are asking:

Can I still stop the foreclosure timeline from becoming the only timeline?

That is the question that matters.

A short sale can protect options, but only if the package is complete, the buyer is serious, the numbers are realistic, and the lender has enough time to review the file. Foreclosure may still happen if those pieces are not handled quickly.

If you are comparing short sale vs foreclosure, do not wait for the process to decide for you. Get the payoff numbers, sale date, hardship documents, title status, and property value reviewed as early as possible.

Crisp Short Sales helps homeowners, agents, and investors work through short sale files before foreclosure removes the room to negotiate.

Ohio Short Sale Experts: When to Call Before Foreclosure

Ohio foreclosure is court-based. The Supreme Court of Ohio explains that a lender files a complaint in the county court of common pleas, and the homeowner generally has 28 days to respond. Ohio law also requires public notice before sale, and redemption may be possible before the court confirms the sale. That does not mean every short sale can be saved late. It means timing matters.

Why Ohio Short Sales Need Early Help

A short sale is not just a listing problem. It is a lender-approval problem.

The listing agent may have a buyer. The seller may be ready. The title company may be willing to close. But the lender still has to review the hardship, financial documents, payoff, offer, title issues, and investor requirements before it releases the lien for less than the full balance.

That is where Ohio files can stall.

If the foreclosure case is already moving, the short sale file needs to be organized quickly. Missing bank statements, unsigned forms, unclear hardship explanations, junior liens, HOA balances, tax issues, judgment liens, buyer financing delays, or incomplete payoff numbers can all burn time.

A short sale expert helps keep the file from drifting while everyone assumes someone else is handling the lender side.

When to Call a Short Sale Expert in Ohio

Call before the foreclosure deadline feels urgent.

That sounds obvious, but many sellers and agents wait until the sheriff sale is already close. By then, the lender may still need a complete package, updated financials, buyer proof, title review, valuation review, and investor approval.

Call when any of these are true:

- The seller has received foreclosure court papers.

- A sheriff sale date is listed or expected.

- The seller owes more than the home is worth.

- The listing agent has an offer but no lender approval yet.

- The lender keeps asking for the same documents.

- There is a second mortgage, HOA lien, tax lien, judgment, or title issue.

- The buyer is getting impatient.

- The seller does not know whether foreclosure can still be delayed.

- The agent has not handled many short sale files recently.

The earlier the short sale file is organized, the easier it is to show the lender, title company, buyer, and foreclosure attorney that the deal is real.

What an Ohio Short Sale Expert Should Actually Do

A short sale expert should not just say "send me the offer."

They should help move the file in a way that supports approval. That usually means checking:

- The seller's hardship story

- Financial documents

- Mortgage payoff and investor rules

- Buyer proof of funds or pre-approval

- Estimated settlement statement