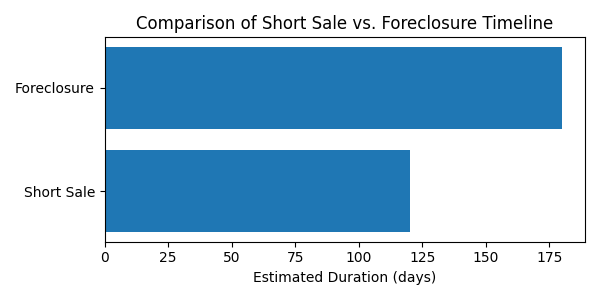

Why Your Short Sale Is Stuck in “Under Review” (And How to Fix It Fast)

You submitted the full package.

The buyer is ready.

The seller is calling daily.

And the lender portal still says: “Under Review.”

Days turn into weeks. Weeks turn into silence. The buyer starts to panic. The agent starts to lose confidence. And the seller starts wondering if this whole short sale thing was a mistake.

Here’s the truth: “Under Review” does not mean what most people think it means. And in many cases, it’s completely fixable.

What “Under Review” Actually Means Inside the Bank

When a file hits “under review,” it usually means one of three things:

1. The file is incomplete (even if no one told you).

2. The negotiator hasn’t actually been assigned yet.

3. It’s sitting in a queue waiting for an internal valuation.

Most lenders won’t proactively tell you which one it is.

That’s where professional short sale processing makes a difference. A strong short sale negotiator knows how to pull status details that aren’t visible in the online portal. They know which departments to call and what questions to ask.

Because “under review” is often code for “no one is actively working this file.”

The #1 Hidden Problem: Silent Document Gaps

Banks rarely reject a file immediately. Instead, they mark it incomplete and let it sit.

Common missing items include:

- Expired bank statements

- Outdated hardship letters

- Incorrectly signed authorization forms

- Settlement statements missing prorations

- HOA estoppel not uploaded correctly

- Insurance declaration pages not included

And here’s the frustrating part: the system won’t always notify you.

If you don’t have someone overseeing short sale document prep and reviewing every upload like a checklist-driven machine, you can lose 30 days without realizing it.

This is exactly why many agents rely on a dedicated short sale processor instead of trying to manage lender portals while juggling listings and buyers.

Valuation Delays: The Other Silent Killer

Even if your file is technically complete, it may be waiting for a BPO (Broker Price Opinion) or internal appraisal review.

Here’s what most agents don’t realize:

- The valuation may already be completed but not uploaded to the negotiator’s system.

- The negotiator might be waiting on an internal second review.

- If the value comes in high, it can stall without explanation.

A proactive short sale coordinator doesn’t wait for portal updates. They call the valuation department. They confirm completion. They escalate internally when needed.

That’s how you close a short sale fast — not by waiting politely.

When the Negotiator Isn’t Really Assigned

Some lenders batch-assign negotiators only after a file hits a certain milestone.

So your file may technically exist in the system but not be on anyone’s desk.

If you don’t follow up consistently, it can sit untouched.

This is one of the biggest differences between passive and active short sale processing. Following up every 7–10 days is not enough at some banks. Sometimes it requires multiple department calls in a single week to get real movement.

It’s not aggressive. It’s strategic.

What Agents Should Check Immediately

If your short sale has been “under review” for more than 14 days, here’s what to verify:

1. Confirm negotiator assignment (get a name and extension).

2. Confirm the complete document list in writing.

3. Verify expiration dates on all financial documents.

4. Confirm valuation status and expected completion date.

5. Confirm there are no internal flags or second-lien holds.

If you’re unsure how to navigate those calls, this is where professional support makes the difference. We outline exactly how we manage these checkpoints inside our process here:

→ short sale support and oversight at /how-we-help

Why DIY Short Sales Stall

Short sales don’t fail because they’re impossible.

They stall because:

- No one is driving the file daily.

- Portals aren’t monitored properly.

- Internal bank notes aren’t reviewed.

- Escalation paths aren’t used.

Most agents are excellent at marketing, negotiating contracts, and serving clients.

But lender negotiation is a completely different skill set.

That’s why we focus exclusively on helping real estate agents close short sales faster — not replacing them, but supporting them behind the scenes. (You can see exactly who we partner with here: /who-we-serve.)

How to Restart a Stalled Short Sale

If your file has been stuck for 30+ days:

- Re-submit a clean, updated package.

- Refresh all financial documents.

- Request a supervisor review if valuation is complete.

- Confirm investor guidelines if it’s FHA, VA, or conventional.

- Ask whether the file needs to be re-escalated internally.

In many cases, a stalled short sale can regain traction within 7–10 days once the right department is engaged.

And if you’re feeling stuck, it may be time to bring in professional short sale assistance to push it across the finish line.

If you want to start the short sale process correctly from day one, here’s where that begins:

→ /start-short-sale

The Bottom Line

“Under Review” is not a death sentence.

It’s usually a communication gap.

The difference between a 30-day approval and a 6-month nightmare often comes down to:

- Precision document prep

- Relentless follow-up

- Strategic escalation

- Experience inside lender systems

Short sales don’t reward patience.

They reward persistence and process.

And when that process is handled properly, approvals move.

What Lenders Really Look for in a Short Sale Hardship Letter

A short sale hardship letter must tell the right story. We explain what lenders expect—clear hardship, proof of lasting financial impact, and consistent documentation—and why professional assistance prevents delays.

When a short sale stalls, it’s rarely because the offer is too low. It’s usually because the hardship letter didn’t tell the right story.

Banks don’t approve short sales out of sympathy. They approve them when the file clearly proves two things:

1) The hardship is real.

2) The hardship is permanent enough that foreclosure is the alternative.

If your hardship letter misses that mark, your short sale approval assistance just became a waiting game.

Let’s break down what lenders are actually looking for — and how a professional short sale processor structures this document to move files forward instead of sideways.

### The Hardship Letter Is Not a Sob Story

This surprises homeowners all the time. A hardship letter is not about emotion. It’s about documentation, clarity, and cause-and-effect.

**Lenders want:**

- A specific event (job loss, medical issue, divorce, death, business failure).

- A clear timeline.

- Evidence that income cannot reasonably recover.

- An explanation of why keeping the home is no longer sustainable.

**What they do not want:**

- Blame.

- Anger.

- Rambling narratives.

- Contradictions with bank statements or tax returns.

This is where professional short sale document prep becomes critical. The hardship letter must align perfectly with the financial package. If the bank sees deposits that contradict the hardship story, the file gets flagged. Delays follow.

### Lenders Look for “Involuntary” Hardship

Voluntary lifestyle changes don’t usually qualify.

**Examples lenders approve more easily:**

- Job termination or significant reduction in hours.

- Medical disability or major medical expenses.

- Divorce requiring sale of the home.

- Death of a borrower.

- Permanent relocation for employment.

**Examples that get pushback:**

- “We want to move.”

- “We don’t like the neighborhood.”

- “The market dropped.”

A seasoned short sale negotiator knows how to frame the hardship in lender language while staying truthful and compliant.

### The Numbers Must Support the Story

Here’s where most agents unintentionally sabotage approvals.

The hardship letter says income dropped.

But the bank statements show large cash deposits.

The letter says medical bills created distress.

But no medical statements are included.

The letter says unemployment is permanent.

But paystubs show new employment starting last month.

Lenders compare:

- Hardship letter.

- Paystubs.

- Bank statements.

- Tax returns.

- Financial worksheet.

If the story and numbers don’t match, you’ll get repeat document requests. That’s when short sale processing turns into a 6-month marathon. When we provide short sale assistance for realtors, this cross-checking happens before submission — not after a denial.

### Lenders Want Clarity and Brevity

Two pages maximum. Often one page is ideal.

A strong hardship letter:

- Opens with the hardship event.

- Explains the financial impact.

- States inability to reinstate.

- Confirms desire to cooperate with short sale.

- Ends respectfully.

No fluff. No drama.

Think business letter, not diary entry.

### Timing Matters More Than You Think

If foreclosure is already scheduled, the hardship letter becomes even more critical.

In late-stage files, lenders want reassurance that:

- The seller is cooperative.

- The offer is legitimate.

- The hardship is ongoing.

- Foreclosure will cost the bank more.

If you’re within weeks of a sale date, it’s critical to move quickly and ensure the entire file — including the hardship letter — is airtight before submission. That’s why homeowners often reach out to us through our [start the short sale process](/start-short-sale) page when time is tight.

### What a Strong Hardship Letter Looks Like (Structurally)

Here’s the structure we typically use when providing short sale approval assistance:

1. **Opening Statement**

- Loan number.

- Property address.

- Brief hardship summary.

2. **Detailed Explanation**

- What happened.

- When it happened.

- How income changed.

3. **Current Financial Position**

- Why reinstatement isn’t possible.

- Why modification won’t solve it.

4. **Resolution**

- Request approval of short sale.

- Acknowledge cooperation.

That’s it. Simple. Direct. Supported by documentation.

### Why Most DIY Hardship Letters Fail

Because they’re written emotionally. Or they’re copied from Google. Or they’re inconsistent with the financials. Or they lack the supporting documentation. And once a lender loses confidence in the file, every subsequent step becomes slower.

This is where having a dedicated short sale specialist behind the scenes changes the outcome. When we step in to provide structured short sale support, lenders recognize the file quality immediately. You can see how we assist with document prep and full-file review on our [how we help](/how-we-help) page.

### Agents: This Is Where Deals Are Won or Lost

Most listing agents are excellent at pricing, marketing, and negotiating offers. But short sale facilitation is a different skillset. Lender packaging, compliance language, escalation protocols, investor guidelines — these are technical processes.

If you’re representing sellers facing hardship, having a professional short sale coordinator can mean the difference between approval and foreclosure. We outline exactly who we work with on our [who we serve](/who-we-serve) page.

### Final Thought

A hardship letter doesn’t need to be dramatic. It needs to be credible. When the story is consistent, supported, and professionally packaged, approvals move faster. When it’s sloppy, emotional, or inconsistent, lenders stall.

If you’re unsure whether your hardship letter will pass lender scrutiny, it’s far easier to fix it before submission than after a denial. Because in short sales, the paperwork isn’t a formality. It’s the decision.

Can You Negotiate a Short Sale After a Foreclosure Sale Date is Issued?

When a foreclosure sale date is issued, it feels like the clock just went from ticking… to exploding.

Related topic hub: Foreclosure Urgency. It groups timing-sensitive posts for sale dates, foreclosure pressure, lender postponements, and short sale options.

Homeowners panic. Agents scramble. Buyers disappear. And everyone starts asking the same question:

**Is it too late to negotiate a short sale?**

The short answer? No.

The better answer? It depends — and timing is everything.

Let’s break it down clearly so you know what’s realistic, what’s risky, and how to navigate it the right way.

## First: What Does a Foreclosure Sale Date Actually Mean?

When the lender schedules a foreclosure sale, it means:

- The borrower is significantly delinquent

- Loss mitigation options have not been approved

- The file has moved to the foreclosure attorney

- The lender is preparing to liquidate the property

But here’s what many agents and homeowners don’t realize:

A foreclosure sale date does not automatically mean the lender won’t consider a short sale.

In many cases, lenders prefer a short sale over foreclosure — even at the last minute — if the numbers make sense and the file is properly packaged.

This is where professional short sale processing becomes critical.

## Can You Still Negotiate a Short Sale After the Sale Date?

Yes — but there are three major conditions:

### 1⃣ The lender must agree to postpone the sale.

This is often called a “sale date extension” or “postponement.”

Lenders will usually postpone the foreclosure if:

- There is a bona fide offer

- The contract is fully executed

- The short sale package is complete

- The net proceeds meet their internal threshold

If the file is sloppy or incomplete, they will not delay the sale just to “see what happens.”

This is why having experienced short sale help matters more at this stage than ever.

### 2⃣ The file must move fast — very fast.

Once a sale date is set, timelines compress dramatically.

- BPOs need to be ordered immediately

- Title must be clean

- All documents must be current

- Buyer must be solid and ready

This is not the time for missing bank statements or outdated pay stubs.

A skilled short sale negotiator knows how to escalate internally and communicate directly with foreclosure counsel to buy time. Without that coordination, files stall — and stalled files get sold at auction.

### 3⃣ The lender’s net calculation must make sense.

At this stage, lenders are laser-focused on one thing:

**Net proceeds.**

If the short sale nets more than foreclosure (after legal costs, holding costs, resale timelines), they will often approve — even days before auction.

If it doesn’t? They’ll let it go to foreclosure.

This is why knowing how to negotiate a short sale properly — including commissions, closing costs, and potential relocation assistance — can be the difference between approval and auction.

## What’s Realistic? Let’s Be Honest.

Here’s what I tell homeowners and agents:

- 30+ days before sale? Very workable.

- 14–30 days before sale? Tight, but doable.

- Under 10 days? Possible, but requires precision and speed.

- 48 hours before auction? Rare, but I’ve seen it happen — if the file is airtight.

The biggest mistake people make is waiting too long to start the short sale process.

If you’re facing a sale date, the worst move is doing nothing. The second worst move is submitting a half-complete package and hoping for the best.

If you're unsure how to structure the file properly, this is where understanding exactly how we help agents and sellers navigate lender escalation can make all the difference.

## Common Myths About Sale Dates and Short Sales

Let’s clear up a few misconceptions:

**Myth #1: Once a sale date is set, the bank won’t talk to you.**

False. They just won’t waste time.

**Myth #2: Filing bankruptcy is the only way to stop foreclosure.**

Not always. A legitimate short sale in review can postpone the auction.

**Myth #3: All lenders behave the same way.**

Definitely not. Some servicers are flexible. Others require aggressive follow-up and internal escalation.

That’s why working with someone who specializes in short sale coordination — not just general real estate — changes outcomes.

If you’re an agent handling distressed listings, understanding who we serve and how we support real estate professionals behind the scenes can dramatically increase your closing ratio.

## Why Speed + Strategy Wins

When a foreclosure sale date is issued, you don’t have the luxury of trial and error.

You need:

- Immediate lender contact

- Clear escalation channels

- Organized documentation

- Strong contract terms

- Strategic negotiation on net

This is not “submit and wait.”

It’s active file management.

At Crisp Short Sales, we’ve handled files at every stage — including last-minute sale dates — and the pattern is always the same:

Prepared files get postponed.

Disorganized files get auctioned.

#You’re Facing a Sale Date Right Now

Here’s what you should do immediately:

1. Confirm the exact sale date in writing.

2. Get a fully executed purchase contract.

3. Assemble a complete financial package.

4. Contact someone experienced in short sale negotiation immediately.

If you need to move quickly, the smartest step is to start a short sale here and get the file structured correctly from day one.

Time is leverage.

Delay is risk.

## Final Thought

Yes — you can negotiate a short sale after a foreclosure sale date is issued.

But the margin for error shrinks fast.

This is where expertise in short sale processing and lender negotiation isn’t a luxury — it’s a requirement.

If you’re an agent inheriting a listing with a ticking clock, or a homeowner staring at an auction notice, don’t assume it’s over.

Just make sure you’re moving with precision.

Because when the sale date hits, preparation is the only thing standing between “sold at auction” and “closed at the table.”

Is a Short Sale Better Than Letting the Home Go to Foreclosure in 2026?

Short sale or foreclosure? Learn the 2026 credit impact, timeline, and risks—and how expert short sale help protects homeowners.

If you’re behind on your mortgage in 2026, you’re probably asking one very direct question:

Related topic hub: Foreclosure Urgency. It groups timing-sensitive posts for sale dates, foreclosure pressure, lender postponements, and short sale options.

Should I try a short sale… or just let the house go to foreclosure?

It’s not an easy place to be. But it is a decision that deserves clarity instead of panic.

As a short sale specialist who has handled these situations for over 15 years, I can tell you this: the two paths are not equal. They affect your credit differently. They affect your future buying power differently. And they absolutely affect your stress level differently.

Let’s break this down clearly and practically.

First: What Actually Happens in a Foreclosure?

In a foreclosure, the lender takes the property back because payments have stopped. The timeline varies by state, but once the sale date hits, control is gone.

Here’s what homeowners often experience:

- Public foreclosure record

- Major credit score drop (often 150–200+ points)

- Difficulty qualifying for a mortgage for 5–7 years

- Potential deficiency balance (depending on state and loan type)

- No relocation incentive

- Little to no control over timing

Foreclosure is reactive. It happens to you.

Now: What Happens in a Short Sale?

A short sale is when you proactively negotiate a payoff with your lender for less than the amount owed.

Instead of the bank forcing a sale, you and your agent market the property and submit an offer for approval. A professional short sale negotiator works directly with the lender to secure approval and release of the lien.

The difference? Control.

With proper short sale assistance, homeowners often experience:

- Smaller credit impact than foreclosure

- Potential eligibility to buy again in 2–4 years (sometimes sooner depending on loan program)

- Possible relocation assistance at closing

- Avoidance of a foreclosure auction

- Closure instead of uncertainty

A short sale is strategic. It’s negotiated.

Credit Impact: The Reality in 2026

Here’s where it gets interesting.

In 2026, lenders are not shocked by hardship anymore. Rising rates, inflation pressure, job shifts, and resets have created more distressed sellers.

A foreclosure is coded as a severe derogatory event. A short sale, when reported correctly as “settled” or “paid for less than owed,” tends to be viewed more favorably by future underwriters.

Is it perfect? No.

But when underwriters see that a borrower worked with the bank, cooperated, and resolved the debt, it tells a very different story than simply letting the property go to sale.

And that narrative matters when you try to buy again.

Deficiency Judgments: The Hidden Risk

This is one area many homeowners overlook.

In some states and loan types, the lender may pursue a deficiency after foreclosure. That means if the house sells for less than what’s owed, you could technically still owe the difference.

With a properly structured short sale negotiation, we push for full deficiency waiver language in the approval letter.

This is one of the biggest advantages of working with an experienced short sale processor. It’s not just about getting approval. It’s about protecting you after closing.

Timing & Stress: What People Don’t Talk About

Foreclosure feels like waiting for a hammer to drop.

Short sale processing gives structure:

- Package submitted

- Valuation ordered

- Negotiations conducted

- Approval issued

- Closing scheduled

There’s a process. There’s communication. There’s movement.

When we work with homeowners, we provide weekly updates and full transparency. You’re not guessing what the bank is doing. You’re not calling a random 800-number hoping someone picks up.

If you’re wondering how we manage that, you can see exactly how we help homeowners navigate the short sale process.

What About Relocation Assistance?

Here’s something many people don’t realize.

Some lenders offer relocation incentives at closing in approved short sales. It’s not guaranteed, but it’s often negotiable depending on investor guidelines.

This can help cover moving expenses and ease the transition.

Foreclosure? There is no structured relocation benefit unless you’re deep into a “cash for keys” situation— and that comes with very little leverage.

When Does Foreclosure Make Sense?

There are rare situations where foreclosure might be the path:

- The home has no market demand at all

- The borrower has already vacated and moved on

- There is no desire to preserve credit

- The timeline is too compressed for a short sale to complete

But even in those cases, it’s worth exploring whether you can negotiate a short sale quickly before the auction date.

If you’re facing a looming sale date and aren’t sure whether you can stop it, here’s how to start the short sale process immediately.

Time matters. Early action creates options.

The Emotional Side of This Decision

Let’s address something real.

Many homeowners avoid short sales because they feel embarrassed.

I’ve had clients whisper, “I feel like I failed.”

You didn’t.

Markets change. Jobs change. Health changes. Divorce happens. Tenants stop paying. Adjustable rates reset.

A short sale is not a failure. It’s a financial strategy to prevent a worse outcome.

The sooner you view it that way, the more control you regain.

Agents: Why This Conversation Matters

If you’re a real estate agent reading this, your distressed seller is watching your confidence.

When you position a short sale as a structured solution—with a dedicated short sale coordinator and experienced negotiator behind you—you give your seller peace of mind.

We regularly provide short sale assistance for agents who want to focus on listing and selling while we handle lender negotiations, document prep, and approval strategy. You can see more about who we serve and how we support agents.

Short sales close more often when they’re handled professionally. That’s just the truth.

So… Is a Short Sale Better?

In most cases in 2026? Yes.

It protects credit better. It preserves dignity. It reduces legal risk. It offers potential relocation help. It gives structure instead of chaos.

Foreclosure is surrender.

A short sale is negotiation.

If you’re unsure which direction makes sense for your situation, reach out. We’ll walk through the numbers, the timeline, and the realistic outcomes so you can make a decision based on facts—not fear.

And that alone is worth the conversation.

How to Negotiate a Short Sale When the BPO Comes in Too High

BPO too high? Learn how to negotiate a short sale when the bank's price opinion is unrealistic and keep your deal alive.

# How to Negotiate a Short Sale When the BPO Comes in Too High If you’ve been in the short sale world long enough, you’ve seen it happen. You submit a clean file. The hardship is solid. The buyer is qualified. The offer makes sense. Then the bank orders a BPO… and it comes back $40,000 too high. Suddenly your short sale approval is “under review,” your buyer is nervous, and everyone is looking at you for answers. Here’s the good news: a high BPO does not kill a deal. It just changes the strategy. Let’s walk through how to negotiate a short sale when the valuation comes in above reality — and how an experienced short sale negotiator handles it. ## Step 1: Understand What the BPO Really Is A Broker Price Opinion is **not** an appraisal. It’s a quick, often surface-level valuation done by a local agent who may or may not understand distressed property value, short sale urgency, or market conditions. Common problems include: - Using retail comps instead of distressed comps - Ignoring condition issues - Overlooking neighborhood declines - Not entering the property This is where professional short sale processing makes a difference. Instead of arguing emotionally, you respond strategically. ## Step 2: Audit the BPO Like a Prosecutor When a BPO comes in high, the first move is not panic. It’s analysis. An experienced short sale specialist will: - Request a copy of the BPO - Compare every comp used - Check for square footage mismatches - Verify sale dates - Confirm condition adjustments - Identify superior vs. inferior properties If the BPO agent used renovated comps while your seller’s home needs a roof and HVAC, that’s leverage. If they used sales from six months ago while prices have softened, that’s leverage. Every error becomes negotiation material. ## Step 3: Submit a Proper Rebuttal Package This is where most deals fall apart. A short sale rebuttal is not a casual email saying, “We disagree.” It is a structured package that includes: - 3–5 better comps (with detailed adjustments) - A revised net sheet - Repair estimates - Updated photos documenting condition - Market trend commentary - Days-on-market data - Active competition analysis You are not just negotiating price. You are building a case. When we handle short sale approval assistance, we format rebuttals the way asset managers expect to see them. Clean. Organized. Data-backed. Banks respond to numbers, not frustration. ## Step 4: Escalate the Right Way If the negotiator refuses to adjust value, escalation may be necessary. But escalation is delicate. Push too hard and you stall the file. Push too soft and nothing changes. An experienced short sale coordinator knows: - When to request a second valuation - When to escalate to a supervisor - When to wait for updated comps - When to reposition the buyer Sometimes the solution is requesting a new BPO. Sometimes it’s asking for a formal appraisal review. Sometimes it’s adjusting the offer slightly while preserving buyer incentives. Negotiating a short sale is part art, part math. ## Step 5: Protect the Buyer While You Negotiate Here’s the real danger of a high BPO: The buyer walks. This is why communication matters. When we provide short sale assistance for realtors, we make sure: - Buyers understand the timeline - Agents understand strategy - Everyone knows we have a plan Transparency prevents panic. If you can confidently explain how you’re challenging the valuation, buyers are far more likely to stay in the deal. ## Step 6: Know When the Bank Is Bluffing Sometimes the bank pushes back hard on price simply to test the file. If there’s only one offer and it’s market-supported, lenders often adjust after sufficient documentation. But if there are multiple offers close to the BPO value? That’s different. A true short sale negotiator understands lender psychology. Some asset managers anchor high expecting pushback. Others genuinely rely on the BPO as gospel. Reading the room matters. ## Why This Is Where Deals Are Won or Lost Most short sales don’t die because the seller doesn’t qualify. They die because valuation disputes drag on too long or are handled poorly. When you’re helping real estate agents close short sales faster, you have to anticipate the valuation battle before it happens. That means: - Pre-pulling comps before submission - Preparing condition documentation early - Pricing strategically from day one This is exactly how we approach files inside our short sale processing system. We assume scrutiny. We prepare for it. If you’re an agent managing this alone, you’re juggling listing duties, buyer communication, and lender negotiation simultaneously. That’s a lot. That’s why many agents choose to outsource the negotiation side entirely. If you want to see exactly how we structure our approach, you can review how we handle valuation challenges and approvals here: 👉 [How We Help](https://www.crispshortsales.com/how-we-help) If you’re an investor or brokerage looking for structured short sale support, you can see who we typically work with here: 👉 [Who We Serve](https://www.crispshortsales.com/who-we-serve) And if you have a file right now that’s stuck because of a high BPO, you can start the short sale process here: 👉 [Start Short Sale](https://www.crispshortsales.com/start-short-sale) ## Final Thought A high BPO is not a rejection. It’s an invitation to negotiate. Handled correctly, it becomes leverage. Handled incorrectly, it becomes a dead deal. Short sale negotiation is not about arguing with the bank. It’s about presenting better data, controlling the narrative, and staying persistent without being reckless. That’s the difference between a file that sits… and a file that closes.

Related topic hub: BPO and Short Sale Pricing. It covers high BPOs, counteroffers, valuation disputes, offer strategy, and pricing problems.

Short Sales Are Rising First in Lower-Income ZIP Codes — What Agents Need to Know

Short Sales Are Rising First in Lower-Income ZIP Codes — What Agents Need to KnowReal estate market shifts rarely arrive all at once; they surface in pockets first. A new mortgage delinquency chart by ZIP code income shows that by the end of 2025, serious delinquencies in zip codes with household incomes under $58k have climbed to around 3.0%, while the highest-income zip codes see about 0.7%. This matters for agents because rising delinquency is often the check-engine light that flashes before a short sale conversation happens.Not every delinquency leads to a short sale, and overall performance remains far below Great Recession levels, but the stress is uneven. Lower income neighborhoods are feeling the pressure first and those sellers typically reach a “we need a plan” moment sooner than higher‑income sellers.## What the chart is really telling usThe Q4 2025 delinquency rates, by annualized zip code income bracket, look something like this:- Under $58k income: ~3.0%- $58k–$73k: ~2.1%- $73k–$101k: ~1.5%- Over $101k: ~0.7%The New York Fed notes that serious delinquencies averaged about 1.3% in 2025 overall. The key takeaway isn’t panic; it's that the stress is uneven and increasing from pandemic-era lows.Agents will see that uneven stress as more price reductions on borderline listings, more sellers who want to sell but can’t bring cash to the closing table, and more files where the lender’s approval timeline becomes the biggest risk. Those are all classic short sale ingredients.## Why delinquency tends to lead short sale volumeA typical progression goes like this: A homeowner hits a disruption (job loss, divorce, medical issue); they fall behind, try to catch up, and realize the math doesn’t work. They consider selling and discover they don’t have enough equity to pay off the loan and costs. That’s when a short sale becomes the option.Delinquency doesn’t guarantee a short sale, but delinquency plus low or declining equity is a common setup. The sellers in lower-income zip codes usually have less financial cushion, so they reach that stage faster.## The agent’s problem: short sales are “easy” until they’re notListing a short sale is simple on paper; getting it approved fast enough to keep a buyer is the real challenge. When delinquencies rise, you see more short sale files where documentation is incomplete, lenders are stricter and timelines tighten because foreclosure activity is picking up. That’s why a dedicated short sale processor or negotiator can be the difference between “we have a contract” and “we have a closing”. Crisp Short Sales focuses on making each file lender‑ready early, so the deal keeps moving.## How to use income‑based delinquency trends as an early‑warning mapYou don’t need to be an economist to use these trends. If you work a market with zip codes that skew lower income or heavy FHA buyer pools, watch for these signs:1. **Listing appointments where the seller “needs a certain number.”** Sellers anchoring on a specific payoff figure are often trying to solve a payoff problem, not a pricing problem.2. **Sellers asking about credits, commissions, and “money at closing.”** Those signals mean the seller is already thinking about cash flow and deficiency risk.3. **Contracts that keep getting renegotiated.** In stressed zip codes, buyers and sellers are more rate‑sensitive, and sloppy approvals can derail deals.When you see these patterns, bring in a short sale negotiator early rather than after the lender has said “no.”## What homeowners in these zip codes need to hearWhen delinquency is rising, homeowners often assume their only options are to catch up magically or be foreclosed on. A short sale is the third option most people don’t understand until it’s late. The message to stressed sellers should be: you’re not alone; you may still be able to sell and move forward without foreclosure; and you need a plan with a timeline because the lender process matters. If they’re ready to move from panic to plan, they can start the short sale process with a team like Crisp.## Bottom lineThe delinquency chart isn’t saying the housing market is collapsing; it’s a forecast that stress is building in specific income bands. That’s exactly where short sales tend to appear first. Agents in those markets don’t need more drama; they need a repeatable process that protects the homeowner, keeps the buyer engaged, and gets the lender to yes without burning their time. That’s what we do at Crisp Short Sales.

The Psychology of the Short Sale Seller: Managing Emotions to Get to Closing

Learn how managing seller emotions is key to closing short sales successfully, from shame and denial to emotional fatigue and fear.

If you've handled more than one short sale listing, you already know something most agents don't talk about enough:

Short sales are not paperwork problems.

They're emotional problems.

Yes, there are lender portals, valuation disputes, hardship letters, and endless document requests. But the real reason many short sales fail isn't missing paperwork. It's a seller who emotionally checks out.

Understanding the psychology of a short sale seller — and knowing how to manage it — is one of the biggest differences between a file that closes and one that dies quietly after 90 days.

Let's break it down.

### 1. Shame and Embarrassment

Most short sale sellers feel like they've failed.

Even if the hardship was caused by job loss, divorce, medical issues, or rate adjustments, they internalize it. They often:

- Avoid returning calls

- Delay submitting documents

- Downplay urgency

- Resist signing paperwork

This isn't laziness. It's avoidance behavior tied to embarrassment.

A strong short sale specialist understands this and communicates differently than a standard listing agent. Instead of pressure, you use reassurance. Instead of urgency alone, you use clarity.

When sellers feel understood, they cooperate. And cooperation is what makes short sale processing move forward.

### 2. Denial and Magical Thinking

You'll hear things like:

- 'Maybe the bank will just forgive it.'

- 'Maybe I can refinance.'

- 'Maybe prices will rebound in 6 months.'

Hope is natural. But denial kills timelines.

A professional short sale negotiator sets expectations early. We explain:

- Approval timelines

- Deficiency possibilities

- Foreclosure deadlines

- Realistic value opinions

Clarity removes fantasy. And removing fantasy creates action.

Without that grounding conversation, sellers delay decisions until it's too late — and suddenly foreclosure is scheduled.

### 3. Emotional Fatigue

Short sales take time. Sometimes months.

Sellers start strong. They respond quickly. They're motivated.

Then 45 days go by.

The lender requests updated paystubs.

The valuation comes in low.

The buyer gets nervous.

The seller gets tired.

This is where most deals quietly fall apart.

A short sale coordinator's real job isn't just document prep. It's maintaining emotional momentum.

That means:

- Weekly updates (even when there's no news)

- Clear explanations of next steps

- Reinforcement that progress is being made

Silence breeds fear. Communication builds stability.

This is a huge reason why we emphasize direct involvement and consistent follow-up at Crisp Short Sales. Emotional management is part of short sale assistance — not an add-on.

### 4. Anger Toward the Bank

Many sellers are angry.

They feel the bank caused the problem. They resent the lender's documentation requests. They see valuation disputes as unfair.

If that anger isn't managed, it shows up in ways like:

- Refusing to submit updated docs

- Ignoring lender calls

- Threatening to 'just let it foreclose'

A seasoned short sale processor acts as a buffer.

We absorb frustration.

We translate lender language.

We depersonalize the process.

The seller doesn't need to fight the bank. They need someone to negotiate the short sale calmly and strategically.

That separation often keeps a deal alive.

### 5. Fear of the Unknown

What happens after closing?

Will I owe money?

Will I be sued?

How long before I can buy again?

Uncertainty creates paralysis.

The more unknowns there are, the more sellers freeze.

This is why education is critical. When we help agents and homeowners understand what happens before, during, and after closing, fear decreases — and cooperation increases.

If you don't proactively answer those questions, sellers will stall while trying to research it themselves.

### Why This Matters for Agents

Most agents are trained to market property.

They are not trained to manage distressed psychology.

And that's completely fair.

But in short sales, emotional regulation is just as important as contract negotiation.

This is exactly why many agents choose to work with a dedicated short sale specialist rather than handling everything alone. The listing agent can focus on selling. The short sale negotiator focuses on lender strategy and seller stability.

When those roles are clear, deals close faster.

If you want to see how we structure that support behind the scenes, you can review exactly how we help manage the full short sale process.

### Why This Matters for Homeowners

If you're a homeowner reading this and considering a short sale, understand this:

You are not alone in how you feel.

Most sellers experience:

- Stress

- Embarrassment

- Anger

- Fear

The goal isn't to rush you. The goal is to guide you.

The right support system makes a massive difference in outcome. You can see who we serve and how we support sellers through the process so you understand exactly what to expect.

And when you're ready, you can start the short sale process here with clarity and structure.

### The Bottom Line

Short sales fail less because of paperwork — and more because of unmanaged emotion.

When a file has:

- Clear expectations

- Consistent communication

- Calm negotiation

- Emotional stability

It closes.

A true short sale processor doesn't just push documents.

A true short sale negotiator doesn't just argue with banks.

They manage people.

And when people are managed well, short sale approvals follow.

Short Sales Are Coming Back in 2026: What to Watch

Short sales are coming back in 2026, but not with the giant flashing sign most people are waiting for. The early signal is quieter: stretched homeowners, higher payments, thinner equity, and agents who need to spot short sale risk before foreclosure pressure becomes obvious. For years, short sales were treated like a relic of the last housing crash. Something agents whispered about and sellers feared. Something lenders grudgingly processed as a last resort. The assumption was that once the foreclosure crisis passed, short sales would fade away.

Fast Answer: Are Short Sales Coming Back in 2026?

Yes, short sales are likely to become more visible in 2026, especially where homeowners have payment stress but not enough equity to sell cleanly. The opportunity is early detection. Agents who identify hardship, liens, and lender requirements before a foreclosure filing can create more options and better outcomes for sellers.

What Agents Should Watch Next

- Look for sellers with rising mortgage stress, HOA balances, tax liens, or little room after closing costs.

- Ask hardship questions early when the numbers do not support a normal sale.

- Bring in short sale help before foreclosure deadlines remove negotiating leverage.

But that's not what's happening. In fact, short sales are quietly poised for a comeback in 2026—and not because of a wave of foreclosures or collapsing home prices. Instead, a combination of structural factors is converging to make short sale transactions more common again. The agents and investors who understand those dynamics will be able to help more homeowners exit gracefully and close deals that others can't.

This Isn’t 2008 All Over Again

First things first: we are not reliving the 2008 crash. Today's market is different. Most homeowners still have fixed‑rate mortgages at historically low rates. Payment histories are generally strong. And while price appreciation is slowing, most owners still have some equity—on paper, at least.

So why are short sales back on the table? It's because of the invisible pressures building under the surface. These pressures aren't about catastrophic job losses or exotic mortgage products. They're about everyday realities that don't show up in national price charts but do show up in your pipeline.

1. The Lock-In Effect Is Trapping Homeowners

Millions of owners refinanced into 2‑4% mortgages during the pandemic. On paper, that sounds like a dream loan. In practice, it's become a cage. When rates jump to 6‑7%, selling a home often means taking on a much higher payment—even for a smaller property.

Meanwhile, life keeps happening. Divorce. Job relocation. Medical expenses. Inherited properties. Aging parents. Burnout landlords. Sellers discover that when you tally commissions, payoff statements and holding costs, that "equity" shrinks fast or disappears. Rather than hemorrhaging money or falling behind, many will opt for a short sale that allows them to move on.

This is where working with a short sale processor or short sale coordinator early in the process makes all the difference. A professional can run the numbers, guide the seller through the paperwork and give the lender confidence that the file is clean and accurate.

2. Equity Is Thinner Than People Realize

Home values remain high compared to pre‑pandemic levels. But thin equity has become a hidden problem. Agents often assume that because a house isn't underwater, there is no need for a short sale. In reality, all the little costs add up:

- Realtor commissions and buyer credits.

- Mandatory repairs and lender‑required upgrades.

- HOA balances, municipal liens and utility bills.

- Carrying costs during long days on market.

Suddenly, that $15,000 in equity is gone—or negative. Without a plan, sellers either reject offers they should accept or walk away from deals that could have closed. A knowledgeable short sale negotiator can get ahead of these issues, explain them to the seller and present a package that banks will approve.

3. Investor-Owned Properties Are Quietly Becoming Distressed

Mom‑and‑pop investors and small rental funds jumped into the market during the last few years. Many bought at peak prices with thin margins, betting on rising rents. Now they're squeezed by higher insurance premiums, rising taxes and slower rent growth. Vacancy rates are ticking up, and turnover costs are heavier than expected.

These properties are often not in foreclosure. They look fine from the outside. But the owners are bleeding cash. Rather than waiting for the situation to deteriorate, many investors are opting for strategic short sales. This is where a short sale assistance team can structure a file that accounts for tenant leases, landlord obligations and investor goals.

4. Lenders Are More Open—But Less Forgiving

Here's the paradox: lenders in 2026 are more willing to consider short sales than in the past. They have streamlined valuations, online portals and dedicated workout departments. However, they expect complete, accurate submissions. Files with missing documents, incorrect HUDs or sloppy hardship letters are now denied in days, not weeks.

Agents who try to wing it often walk into a bureaucratic buzz saw. Deals stall for months, buyers walk away, and sellers lose hope. Working with an experienced short sale processor protects your clients from these pitfalls. We know which documents matter, when to submit updated financials and how to keep a file active until approval comes through.

5. Buyers Are Back—and They’re Paying Attention

Buyers in 2026 aren't naive. They're watching interest rates, reading about short sales and expecting transparency. They don't want surprises at closing. When buyers see that a short sale is being handled by a professional, confidence goes up—not down.

Remember: buyers often pay for the short sale facilitation. When they know there is a professional guiding the process, they are more comfortable paying for that service. That means deals close faster, and your seller gets to move on sooner.

The Real Shift: Short Sales as a Planning Tool

The biggest change is how short sales are being used. They are no longer just emergency maneuvers for people already in foreclosure. In 2026, the most successful short sales are planned early and executed cleanly. They give homeowners and investors control over their timelines and finances.

If you have a listing where the numbers don't work, or you hear a seller saying they "can't afford to sell," it's time to start the short sale process proactively. Working with professionals can help your clients walk away with dignity, sometimes even with a relocation stipend or cash for keys.

What This Means for Agents Right Now

The return of short sales isn't about doom and gloom. It's about friction in the market. Agents who embrace this reality will thrive. Here's what to do:

- Identify properties where equity is thin or nonexistent.

- Engage a short sale specialist early to evaluate options.

- Educate sellers on the benefits of short sale help versus letting the situation deteriorate.

- Remind buyers that paying for a negotiator is a small investment to secure a clean title and a timely closing.

If you need help helping real estate agents close short sales faster, we have an entire team dedicated to just that. Our goal is to guide agents, investors and homeowners through every step so they get approved and close on time.

Bottom Line

Short sales are coming back in 2026, but not because of a housing crash. They're returning because of the lock‑in effect, thin equity, stressed investors, evolving lender expectations and savvy buyers. The agents who recognize these trends and partner with an experienced short sale professional will close deals others never even get approved.

Whether you're a homeowner facing a tough decision, an investor considering your exit strategy or an agent who wants to expand your toolbox, understanding the new world of short sales will set you apart. It's not about panic. It's about planning—and about knowing who to call when you need short sale assistance.

What Listing Agents Should Know Before Accepting an Offer on a Short Sale

Learn what listing agents should consider before accepting a short sale offer: evaluate net proceeds, buyer strength, credits, pricing, and timing to prevent delays and denials.

Accepting an offer on a short sale isn’t the finish line—it’s the starting gate. Too many short sale listings stall or die because the offer looked “good enough” on paper but wasn’t structured with the lender’s reality in mind.

Related topic hub: Short Sale Help for Agents. It pulls together the practical workflow posts agents need before submitting, negotiating, and closing a short sale.

As a listing agent, your role at this stage is critical. The right offer sets expectations, shortens timelines, and dramatically improves approval odds. The wrong one wastes months and leaves everyone frustrated.

Here’s what every agent should know before they accept an offer on a short sale—and how the right short sale assistance can keep your deal on track.

1. Not All Offers Are Equal in the Bank’s Eyes

A common mistake is assuming the highest offer wins. Lenders don’t think like buyers or sellers — they think like loss mitigation departments. Banks evaluate net proceeds after all fees and credits, market support through BPOs and appraisals, buyer strength and closing certainty, and clean, defensible numbers. An offer with inflated credits, weak financing, or unrealistic seller concessions often gets countered—or worse, denied outright. This is where having a short sale negotiator review the deal structure before submission can save weeks of back‑and‑forth.

2. Seller Credits Can Kill an Otherwise Good Deal

Credits are one of the fastest ways to trigger lender objections. Many investors restrict or prohibit excessive buyer closing cost credits, credits tied to third‑party fees, or any credits that reduce net proceeds below threshold. Agents often accept offers with large credits thinking they’ll sort it out later. Unfortunately, lenders see credits as negotiable red flags, not placeholders. A short sale processor can help evaluate whether credits are realistic for the specific loan type and investor—before the offer ever goes to the bank.

3. Buyer Type Matters More Than You Think

From a lender’s perspective, not all buyers are created equal. Generally, banks prefer strong conventional or cash buyers, clean loan approvals, and buyers with realistic timelines. They’re more cautious with FHA or VA loans (extra overlays), buyers relying on layered assistance, or tight closing windows with contingencies. This doesn’t mean those buyers can’t work — it means the offer must be structured carefully. Experienced short sale processing anticipates these concerns and positions the buyer correctly in the submission package.

4. Your Short Sale Package Starts With the Offer

Once an offer is accepted, everything else builds off it: financials, the hardship narrative, the HUD or net sheet, and lender negotiations. If the offer is flawed, the entire file suffers. Fixing deal terms after submission often resets timelines or forces resubmissions. Agents who work with a short sale specialist early tend to see smoother approvals because the offer and documentation align from day one.

5. Pricing Still Matters—Even Below Market

Pricing a short sale low to spark interest can backfire. Lenders rely heavily on BPOs, and a low contract price can anchor the valuation downward—but not always in your favor. Banks may order multiple BPOs, counter above contract price, or delay while seeking justification. The goal is defensible pricing, not desperation pricing. A short sale negotiator works with the numbers the bank is likely to accept—not just what gets showings.

6. Communication Expectations Should Be Set Immediately

Once an offer is accepted, sellers and buyers often expect rapid movement. In reality, lender response times vary widely, files move in stages, not straight lines, and silence doesn’t always mean inactivity. This is where proactive communication matters. When agents partner with a coordinator who handles lender updates and escalations, they’re freed up to focus on selling—not status chasing. This collaborative model is exactly why we built our process around supporting listing agents and their clients throughout the transaction.

7. Timing the Offer Acceptance Is a Strategy

Sometimes the smartest move isn’t accepting the first offer—it’s waiting for the right one. Questions to ask before accepting: Is the buyer prepared for a long timeline? Are terms lender-friendly? Can this offer survive scrutiny? Rushing into acceptance often creates avoidable problems later. A quick pre-review by a short sale coordinator can tell you whether the deal is worth submitting—or needs adjustment first.

Final Thought: The Offer Sets the Tone for the Entire Short Sale

Short sales don’t fail randomly. They fail because of preventable mistakes made at the offer stage. When agents understand what lenders look for—and partner with experienced short sale help early—they close more deals, faster, with far less stress. If you’re about to accept an offer or want a second set of eyes before submitting to the bank, we’re always happy to help you start the short sale process the right way.

VA Short Sales Explained: Process, Timing, and Next Steps

A plain-English explanation of VA short sale process steps, timing, documents, and lender review issues for agents and homeowners.

When a homeowner has a VA-backed mortgage and owes more than the home is worth, a VA short sale can be a powerful alternative to foreclosure. But VA short sales are very different from conventional or FHA short sales — and misunderstanding the process is one of the biggest reasons these deals stall or fail.

Related topic hub: Liens and Complex Short Sale Files. It covers HOA dues, IRS tax liens, reverse mortgages, FHA and VA rules, and other complex-file risks.

For homeowners, VA short sales offer a path out with dignity, less long-term credit damage, and the ability to move on.

For real estate agents, they can unlock listings that would otherwise be lost to foreclosure — if the process is handled correctly.

This article breaks down how VA short sales work, what both homeowners and agents should expect, and how a professional short sale processor and negotiator can make the difference between approval and denial.

What Is a VA Short Sale?

A VA short sale happens when a lender agrees to accept less than the total mortgage balance on a VA-guaranteed loan, and the U.S. Department of Veterans Affairs also approves the transaction.

Unlike a standard short sale, VA loans add a second layer of review:

1. The loan servicer evaluates the short sale.

2. The VA must approve the net proceeds and terms.

That second approval is critical — and it’s where many deals slow down without proper short sale coordination.

How the VA Short Sale Process Works (Step by Step)

1. Homeowner Hardship Review

The process starts with a documented hardship. Common VA short sale hardships include:

- Loss or reduction of income

- Divorce or separation

- Medical expenses

- PCS or relocation

- Rising payments or escrow increases

The homeowner must show they can no longer sustain the mortgage and that the home’s value doesn’t support the loan balance.

2. Property Is Listed and Offer Accepted

Once listed, the agent secures a buyer and a signed contract. VA short sales are not approved before an offer — the lender and VA need real numbers to review.

This is where many agents underestimate the workload. A clean contract alone isn’t enough.

3. Complete VA Short Sale Package Is Submitted

This is the most critical step — and where professional short sale processing matters.

A complete VA short sale package typically includes:

- Financials and hardship letter

- Listing agreement and purchase contract

- Estimated HUD / closing disclosure

- Broker price opinion or appraisal

- VA-specific forms and net sheets

Missing or incorrect documentation can reset the review clock or trigger a denial.

4. Lender Review and VA Approval

The lender reviews the file first. If acceptable, it is submitted to the VA for final approval of:

- Net proceeds

- Closing costs

- Commissions

- Any buyer or seller credits

This dual-approval structure means follow-up and accuracy are essential.

5. Approval Letter and Closing

Once approved, the transaction moves to closing with VA-approved terms. Timing, coordination with title, and compliance with VA conditions are key to getting to the finish line.

Why VA Short Sales Are Tricky Without Help

VA short sales are very doable — but they are not forgiving. The most common failure points we see are:

- Incomplete or inconsistent packages

- Agents unfamiliar with VA guidelines

- Poor communication with the servicer

- Delays that push the loan toward foreclosure

- Confusion around VA deficiency and entitlement issues

This is exactly where experienced short sale negotiators and coordinators add value.

How Crisp Short Sales Helps VA Short Sale Deals Close

For Homeowners

We:

- Explain the VA short sale process in plain language

- Gather and organize all required documentation

- Communicate directly with the lender and VA

- Help protect the homeowner from unnecessary delays

- Guide them through the next steps after closing

If you’re looking for professional short sale help and want a clear plan forward, we make the process manageable from day one.

For Real Estate Agents

We:

- Handle short sale processing from start to finish

- Act as the primary point of contact with the lender and VA

- Ensure clean, compliant submissions

- Reduce approval timelines and surprises

- Keep you focused on selling — not paperwork

Most importantly, there is no upfront cost to you or your client. We’re paid at closing, typically by the buyer, so there’s no financial risk to trying to save the deal.

If you work with distressed sellers or VA-backed loans, our short sale assistance for realtors is designed to protect your time, your commissions, and your reputation.

Learn more about how we help here:

👉 /how-we-help

Who VA Short Sales Are Right For

VA short sales are often a great fit for:

- Veterans facing financial hardship

- Homeowners trying to avoid foreclosure

- Agents with VA listings stuck in limbo

- Buyers looking for structured, legitimate short sale opportunities

We regularly support agents, homeowners, and investors through this process. You can see exactly who we serve here:

👉 /who-we-serve

Thinking About Starting a VA Short Sale?

If you’re early in the process — or already under contract and feeling stuck — the best move is to get clarity fast.

You don’t need to guess your way through VA guidelines or lender expectations. With proper short sale coordination, these deals can close smoothly.

If you’re ready to start the VA short sale process, we’re happy to walk you through the next steps:

👉 /start-short-sale

FHA Short Sales: How the Process Really Works (And How to Get Them Approved)

FHA short sales are not “regular” short sales with a different logo slapped on the paperwork. They follow a very specific HUD-driven process, include additional layers of review, and leave far less room for error. When handled correctly, they can absolutely get approved. When handled casually, they stall, get suspended, or quietly die.

Related topic hub: Liens and Complex Short Sale Files. It covers HOA dues, IRS tax liens, reverse mortgages, FHA and VA rules, and other complex-file risks.

If you are a homeowner trying to avoid foreclosure or a real estate agent navigating an FHA deal for the first time (or the tenth), this guide will walk you through what actually happens, what to expect, and how professional short sale processing dramatically improves approval odds.

What Makes an FHA Short Sale Different?

FHA loans are insured by HUD, which means the lender is not making approval decisions in a vacuum. Even though the loan is serviced by a bank or mortgage company, HUD guidelines drive the approval framework.

Key differences include:

• Stricter financial review

• Mandatory net thresholds

• Required documentation formats

• Limited flexibility on credits and fees

• Additional approval layers beyond the servicer

This is why FHA short sales often feel slower and more rigid. The rules are not optional.

Step 1: Verifying FHA Eligibility

Before anything is submitted, the first step is confirming:

• The loan is FHA-insured

• The homeowner qualifies for a short sale under HUD guidelines

• There are no disqualifying issues such as recent fraud, undisclosed transfers, or unresolved bankruptcy restrictions

This step alone eliminates a lot of wasted time. Submitting a short sale package that was never eligible in the first place is one of the most common mistakes agents make.

Step 2: Homeowner Financial Review and Hardship

FHA short sales require clear, documented financial hardship. HUD expects the numbers to tell a consistent story.

Typically required:

• Hardship letter that aligns with financials

• Pay stubs or proof of income

• Bank statements

• Tax returns (when requested)

• Monthly expense breakdown

This is not a place for vague explanations or missing pages. Incomplete or inconsistent documentation almost always triggers re-requests and delays.

This is where experienced short sale processing matters. Files are reviewed for internal consistency before they ever reach the lender.

Step 3: Listing the Property and Offer Review

Once listed, FHA short sales are priced based on HUD net expectations, not just comps. A good listing price:

• Attracts real buyers

• Aligns with FHA net thresholds

• Minimizes counteroffers and re-marketing

When offers come in, FHA looks closely at:

• Purchase price

• Closing costs

• Credits

• Repair requests

• Third-party fees

Deals often fall apart here when agents assume FHA will “just counter.” FHA usually does not negotiate the way conventional lenders do. If the structure is wrong, the file can simply stall.

Step 4: FHA Appraisal and Net Calculation

FHA short sales typically require an FHA appraisal or valuation review. The final approval is driven by net proceeds, not emotion or effort.

HUD calculates:

• Allowable closing costs

• Maximum commissions

• Approved third-party fees

• Minimum acceptable net

If the numbers do not work, the deal does not work. Period.

This is where a short sale negotiator earns their keep by structuring offers correctly before they hit underwriting.

Step 5: Approval, Conditions, and Timelines

FHA short sale approvals often come with:

• Strict expiration dates

• Non-negotiable conditions

• Zero tolerance for post-approval changes

Miss one deadline or change one line item and the approval can be voided.

From submission to approval, FHA short sales typically take:

• 90–150 days when handled correctly

• Much longer when files bounce back for corrections

What Homeowners Should Expect

For homeowners, FHA short sales are emotionally exhausting but often the best alternative to foreclosure.

Homeowners should expect:

• Detailed financial review

• Regular document updates

• Clear timelines

• No surprises at closing

When managed properly, FHA short sales allow homeowners to move on with dignity, minimize credit damage, and sometimes qualify for future financing sooner than expected.

What Agents Should Expect

Agents should expect FHA short sales to:

• Require patience

• Demand precision

• Punish sloppy submissions

But when done right, they also:

• Close consistently

• Protect commissions

• Build long-term credibility with clients

This is why many agents choose to outsource FHA files to a dedicated short sale coordinator instead of juggling lender portals, buyer expectations, and constant follow-ups.

How Crisp Short Sales Helps FHA Deals Get Approved

At Crisp Short Sales, FHA files are handled with process discipline, not guesswork.

We help by:

• Reviewing eligibility before listing

• Preparing HUD-compliant short sale packages

• Managing all lender and HUD communication

• Structuring offers to meet FHA net requirements

• Preventing last-minute approval failures

• Keeping agents and homeowners informed throughout

If you are looking for short sale help that reduces delays, protects commissions, and keeps FHA files from derailing, this is exactly what we do every day. Learn more about how we assist throughout the on our /how-we-help page..

We also specialize in helping real estate agents close FHA short sales faster, which you can explore on our /who-we-serve page.

If you are dealing with an FHA short sale now and want to start the short sale process the right way, you can get started directly at /start-short-sale.

Short Sale Approval Timelines by Investor Type: What Agents Should Really Expect

One of the biggest mistakes agents make with short sales isn’t pricing, paperwork, or even the buyer—it’s expectations.

Related topic hub: Short Sale Approval Delays. It breaks down lender delays, document loops, valuation problems, mortgage insurance review, and next steps.

Not all short sales move on the same clock. The investor behind the loan determines how fast (or slow) things move, who you negotiate with, and what approvals are required. Understanding these timelines upfront is the difference between a smooth closing and months of frustration.

As a short sale processor and negotiator, I’ve worked files across every major investor type. Here’s what agents should realistically expect—and how proper short sale coordination keeps deals from stalling.

FHA Short Sales: Expect 30–60 Days After Initial Approval

FHA short sales are often misunderstood because agents assume approval is “one and done.” It’s not. With FHA loans, the initial short sale approval is only part of the process. Once you have a ratified contract, FHA requires an Approval to Participate (ATP)—a re-approval of the short sale terms based on the executed offer.

Typical FHA timeline:

• File submitted and reviewed by the servicer

• Offer accepted by the seller

• ATP requested from FHA

• 30–60 days for ATP decision after submission

This is where many FHA deals die. Missing documents, incorrect net sheets, or premature buyer expectations can cause delays that feel endless. Having a dedicated short sale coordinator ensures the ATP package is clean, complete, and submitted correctly the first time. That alone can shave weeks off the process and protect the deal while buyers wait.

VA Short Sales: Usually 60 Days for a Decision

VA short sales follow a more centralized and rigid approval structure. Unlike conventional loans, the VA requires its own internal review before a final decision is issued.

What agents should expect:

• Servicer reviews the file first

• VA reviews the short sale request

• Decision typically issued in about 60 days

There’s very little room to “push” VA timelines, which makes expectation management critical. Buyers need to know upfront that this isn’t a 30‑day approval, and sellers need reassurance that the process is still moving even when there’s silence. This is where consistent communication matters. A short sale specialist keeps weekly touchpoints with the servicer so nothing quietly expires or falls out of queue—one of the most common reasons VA files stall.

Fannie Mae Short Sales: Faster, but a Completely Different Process

Fannie Mae short sales are often faster—but only if you know the system. Once the servicer completes its internal review, the file is transferred to Fannie Mae, and negotiations no longer happen with the servicer. Instead, agents or their short sale negotiator must upload the offer directly through the Aspen Grove portal and negotiate with Fannie Mae itself.

Typical Fannie Mae timeline:

• 30 days for file transfer from servicer to Fannie Mae

• Offer uploaded to Aspen Grove

• Direct negotiation with Fannie Mae

• Decisions often move quickly once live in the portal

The problem? Many agents don’t realize they’re now dealing with an entirely different entity—and they miss deadlines, upload incorrect documents, or wait on a servicer who’s no longer involved. A professional short sale processor understands this handoff and takes control of Aspen Grove submissions so agents aren’t learning a new system mid-deal.

Privately Owned Loans: Wildcards—but Often the Fastest

Privately owned loans don’t follow a standardized timeline. Each investor sets their own rules, valuation methods, and approval structure. That said, these files often move faster than government-backed loans.

What’s typical:

• Timeline varies every time

• Some approvals in weeks

• Others require multiple valuation rounds

• Decisions are often quicker when documentation is strong

Because there’s no universal rulebook, these files demand experience. Knowing when to push, when to wait, and how to present a clean financial narrative makes all the difference. This is where seasoned short sale negotiation pays off. A well-packaged file can mean approval in a fraction of the time agents expect.

Why Timelines Fail Without Proper Short Sale Processing

Most short sales don’t fail because the investor says no. They fail because:

• Documents expire

• Buyers lose patience

• Agents can’t get updates

• Files sit untouched in queues

A dedicated short sale negotiator keeps the file active, the parties informed, and expectations realistic from day one. If you have a short sale listing—or one headed that way—and want to avoid surprises, start the short sale process early. Early setup almost always leads to faster approvals later.

Why Investors Lose Good Short Sale Deals Even With Solid Offers

Even strong offers fail in short sales. Learn why investors lose deals and how proper short sale processing and negotiation prevents it.

If you’ve ever submitted what looked like a great offer on a short sale and still lost the deal, you’re not alone. This happens every day. And most of the time, it has nothing to do with price.

Investors tend to assume short sales fail because lenders are unreasonable or slow. In reality, most failed short sale deals collapse due to process mistakes, missing documentation, or poor lender communication. Even experienced investors with strong offers can lose deals simply because no one is properly managing the short sale.

This is where working with a short sale processor or short sale negotiator can mean the difference between closing and wasting months.

Let’s break down the most common reasons investors lose short sale deals—and how to prevent it.

1. The Offer Is Strong, but the Package Is Weak

Banks don’t approve short sales based on offer price alone. They approve them based on risk reduction and completeness.

A common mistake investors make is assuming the listing agent or seller will “handle the paperwork.” In reality, many short sale packages are incomplete, inconsistent, or poorly organized.

Typical issues include:

- Missing or outdated hardship letters

- Incomplete financials

- Incorrect HUDs or net sheets

- Title issues discovered late

- Liens not disclosed upfront

When a lender flags missing items, the file gets pushed aside—or worse, closed entirely.

This is where short sale processing matters. A dedicated short sale specialist ensures the file is clean, complete, and lender-ready from the start.

2. No One Is Driving the File Forward

Short sales don’t move themselves. If no one is actively following up with the lender, the deal stalls.

Investors often assume:

- The agent is calling the bank

- The bank is reviewing the file

- Someone else is managing timelines

Meanwhile, weeks pass with no movement.

A professional short sale coordinator tracks:

- Lender touchpoints

- Review stages

- Escalations

- Required updates

- Approval expiration dates

Without this oversight, even strong deals quietly die.

If you want to see what active management looks like, this is exactly how we guide files from submission through approval on our how-we-help page.

3. The Buyer Side Isn’t Properly Represented

Investors often don’t realize how much their side of the deal matters in a short sale.

Lenders evaluate:

- Buyer credibility

- Proof of funds

- Closing timelines

- End buyer structure (especially with assignments or flips)

If the lender senses uncertainty, delays, or confusion, they’ll move on to another offer or reject the file outright.

A seasoned short sale negotiator knows how to position the buyer as:

- Capable

- Ready

- Low risk

- Aligned with lender goals

That positioning alone saves deals that would otherwise fall apart.

4. Late Discovery of Liens or Secondary Mortgages

One of the biggest silent deal killers is discovering liens late in the process.

Common examples:

- Second mortgages

- HELOCs

- HOA arrears

- Judgment liens

When these surface late, lenders may:

- Reduce approvals

- Reopen negotiations

- Deny the short sale altogether

A proper short sale review includes early title analysis and lien strategy—not a last-minute scramble.

This is why investors and agents who work with us consistently lean on our experience serving both sides of the transaction, as outlined on our who-we-serve page.

5. Approval Terms Aren’t Reviewed Carefully

Even when a short sale is approved, deals still fall apart because approval terms aren’t reviewed closely.

Issues include:

- Short approval windows

- Unexpected closing costs

- Repair or condition requirements

- Buyer contribution clauses

Investors sometimes assume approvals are final, only to realize later that the terms don’t match the original offer—or don’t work financially.

A short sale specialist reviews approval letters line by line, flags problems immediately, and negotiates revisions when possible.

That step alone saves deals that would otherwise be abandoned.

6. No Clear Strategy for Communication

Short sales involve multiple parties:

- Seller

- Listing agent

- Buyer

- Buyer’s agent

- Lender(s)

- Title company

When communication isn’t centralized, messages get lost, timelines slip, and trust erodes.

Investors lose deals simply because:

- No one updated the lender

- No one responded quickly

- No one clarified a condition

Professional short sale assistance means one point of contact, consistent updates, and fewer surprises.

How Investors Can Stop Losing Short Sale Deals

The fix isn’t offering more money. It’s improving execution.

Successful investors treat short sales as a process, not just a purchase.

That means:

- Partnering with a short sale processor early

- Ensuring packages are complete and accurate

- Actively negotiating with lenders

- Monitoring timelines and approvals

- Catching issues before they become deal killers