Early Warning Signs a Regular Listing Is Turning Into a Short Sale

The listing started normally.

Nice photos. Reasonable seller. Maybe a little stress in the background, but nothing that screamed "distressed sale."

Then the showings slowed. The seller stopped returning documents quickly. The payoff looked a little suspicious. Suddenly, the agent is trying to figure out whether this is still a regular listing or whether it quietly became a short sale while everyone was busy discussing paint colors.

That is the moment to pay attention.

The goal is simple: spot short sale risk early enough that the file can still be organized, priced correctly, and moved toward a real closing instead of becoming a last-minute emergency.

Why Agents Miss the Warning Signs

Most listings do not announce themselves as short sales on day one.

Sometimes the seller is embarrassed. Sometimes they do not understand the payoff. Sometimes they think the market will solve the problem. Sometimes they are hoping for a miracle offer, which is not technically a pricing strategy, although it does make for lively group texts.

The issue is that short sale problems usually get worse with time.

If the listing is overpriced, market time increases. If payments are late, foreclosure pressure builds. If liens or HOA balances are ignored, closing gets harder. If the seller waits too long to disclose hardship, the agent loses valuable time.

That is why agents should treat early warning signs seriously. You are not trying to label every tight-equity listing as a short sale. You are trying to find out whether the deal needs short sale assistance before the calendar starts making decisions for everyone.

Warning Sign 1: The Payoff Does Not Match the Market

The first clue is usually math. If the mortgage payoff, second mortgage, liens, HOA balance, taxes, commissions, and closing costs exceed what the home can realistically sell for, the file may not be able to close as a normal sale.

The key word is realistically.

A seller may believe the house is worth more. A neighbor may have sold high two years ago. A buyer may appear eventually. But if current comps, condition, showing feedback, and market time all point lower, the agent should not ignore the gap.

A short sale starts becoming likely when the only way to close is for the lender or another lienholder to accept less than the full amount owed.

Warning Sign 2: The Seller Cannot Bring Money to Closing

A payoff shortage is one problem. The seller's ability to cover it is another.

Agents should ask direct, practical questions early:

- If the home sells at market value, can you bring money to closing?

- Are there any second loans, judgments, tax liens, or HOA balances?

- Have you checked the current payoff, not just the monthly statement?

- Are you current on the mortgage and association dues?

If the seller cannot bring funds to closing and the numbers do not work, the listing may need a short sale specialist before an offer is accepted, not after everyone is already frustrated.

For agents who want support while keeping the client relationship intact, Crisp's approach to helping real estate agents handle short sale files is built for exactly this situation.

Warning Sign 3: The Seller Is Behind, But Avoiding the Topic

Sellers do not always volunteer that they are behind.

They may say things like:

- "We are trying to catch up."

- "The bank is working with us."

- "There is no sale date yet."

- "We just need to sell quickly."

Those statements are not proof of a short sale, but they are strong signals that the agent should ask more questions.

If missed payments are already involved, time matters. The file may need lender review, hardship documentation, payoff statements, title review, buyer coordination, and foreclosure tracking. That is a lot to discover after a contract is signed.

This is where it helps to start the short sale process before deadlines tighten, especially if there is already an offer or serious buyer interest.

Warning Sign 4: The Seller Keeps Rejecting Market Feedback

Some sellers resist price reductions because they want to walk away with money. That is normal. But when the numbers are tight, resistance to market feedback may be a sign that the seller has not accepted the financial reality.

If the seller needs a certain price only because that is what would pay off the loan, that price may not be market value. It may simply be the seller's break-even number.

Agents should separate the two. A listing can be priced at the amount the seller wants, or it can be priced where the market is likely to respond. In a potential short sale, confusing those two numbers can burn the time needed to negotiate the file.

Warning Sign 5: There Are Liens, HOA Balances, or Title Problems

Sometimes the mortgage is not the only problem.

A regular listing can become a short sale because of second mortgages, judgments, IRS liens, unpaid property taxes, HOA dues, condo association balances, collection attorney fees, or other title issues that have to be paid or released before closing.

For example, an HOA payoff letter should usually be ordered after approval when the file is closer to closing, but an account balance statement should be gathered early so the total amount owed is accounted for in the deal.

If these items are discovered late, the settlement statement may no longer work. The lender may need to approve different numbers. The buyer may need an extension. Title may need releases. The file can turn from straightforward to complicated very quickly.

Crisp helps agents and sellers organize these moving parts through short sale processing support that keeps the file moving, including payoff issues, lien review, document collection, and lender communication.

What Agents Should Do First

When a regular listing starts showing short sale warning signs, the next step is not panic. It is verification.

Agents should move through a short, practical checklist:

- Confirm the current mortgage payoff.

- Review realistic market value, not wishful pricing.

- Ask whether the seller can bring money to closing.

- Identify hardship early.

- Check payment and foreclosure status.

- Look for second liens, HOA balances, judgments, taxes, or title issues.

- Adjust pricing before market time becomes a bigger problem.

- Get short sale help if the numbers no longer support a normal closing.

The earlier the issue is identified, the more options the seller and agent usually have. Waiting until a buyer is under contract can still work, but it often creates avoidable pressure.

The Bottom Line

A regular listing can turn into a short sale gradually.

It may start with a payoff gap, a seller who cannot bring money to closing, missed payments, lien issues, HOA balances, or pricing resistance that does not match the market.

Agents do not need to solve every short sale problem alone. But they do need to recognize when the file is no longer behaving like a normal sale.

The sooner those warning signs are caught, the easier it is to organize the file, protect the timeline, communicate honestly with the seller, and give the transaction a real chance to close.

Because the worst time to discover a short sale is when everyone thought they were already at the finish line.

Texas Foreclosure Sale Date Coming Up? When a Short Sale Can Still Work

The foreclosure sale date is on the calendar.

The seller is panicking. The agent is trying to figure out if the listing can still be saved. The buyer, if there is one, wants to know whether this deal is real or just a very stressful group project with worse snacks.

The goal is simple: stop the file from drifting into foreclosure and see whether a short sale can still create a better outcome.

In Texas, timing matters a lot. Foreclosure sales are commonly scheduled quickly, and once that date is approaching, every delay becomes more expensive. A short sale may still work, but only if the right pieces move fast and in the right order.

First, Confirm the Sale Date

Before anyone starts guessing, confirm the actual foreclosure sale date. Not "sometime soon." Not "I think next month." The actual date.

That date controls everything.

If there is enough time to submit a complete short sale package, the lender may review the file and consider postponing the foreclosure sale. If the file is incomplete, disorganized, or missing key documents, the lender has very little reason to stop the process.

This is where early short sale help before the foreclosure clock gets tighter can make a real difference. The goal is not just to submit something. The goal is to submit something the lender can actually review.

A Short Sale Is Not Just an Offer

One of the biggest mistakes agents and sellers make is thinking the offer itself is the short sale package.

It is not.

The offer matters, but the lender usually needs much more before it can evaluate the request. That may include the seller's hardship letter, financial worksheet, bank statements, pay stubs, tax documents, listing agreement, purchase contract, estimated settlement statement, authorization forms, and supporting property information.

If the lender asks for documents one at a time, the file can bleed days quickly. In a Texas foreclosure timeline, days are not decorative. They are the deal.

A strong short sale coordinator helps make sure the package is complete, current, and presented in a way the lender can process without bouncing it back for avoidable reasons.

The Lender Needs a Reason to Postpone

A lender does not usually postpone a foreclosure sale just because someone asks nicely.

It needs a file that shows there is a realistic alternative to foreclosure.

That means the short sale request should show:

- The seller has a legitimate hardship.

- The property value supports the offer.

- The buyer appears serious and qualified.

- The numbers make sense.

- The file is complete enough for review.

- The closing path is realistic.

If the lender sees a half-built file, it may keep the foreclosure moving. If it sees a complete file with a real offer and a clear path to closing, there may be a better chance of getting attention.

This is why how we help agents and homeowners organize short sale files is not just paperwork support. It is about giving the lender a usable file before the timeline collapses.

What If There Is No Offer Yet?

A short sale can be harder without an offer, but that does not always mean the situation is hopeless.

If the property is listed, priced realistically, and marketed properly, the agent may still be able to create activity. The important part is being honest about value. An inflated list price can waste the most important days the seller has left.

If the property has already been sitting with little activity, the agent should look at pricing, condition, access, buyer feedback, and comparable sales immediately. A lender is not likely to take a weak offer seriously if the pricing story is sloppy.

In a foreclosure-pressure situation, "let's test the market" can become very expensive. The market already gave feedback. Listen to it.

What If the Buyer Is Ready?

If there is already a buyer, the focus shifts to packaging and urgency.

The buyer's offer should be clean. Financing should be credible. Proof of funds or pre-approval should be included. The estimated settlement statement should reflect realistic costs. Any HOA balances, liens, taxes, or second mortgages should be identified early.

This is where a short sale specialist or short sale negotiator can help prevent the file from going sideways. The lender is not only reviewing price. It is reviewing whether the deal can actually close.

A good offer with bad paperwork can still lose to the calendar.

Agents Should Not Wait for One More Update

When a foreclosure sale date is close, waiting passively for updates is usually the wrong move.

The file needs active follow-up. Not random "just checking in" emails, but specific follow-up tied to what the lender needs next.

Has the file been opened?

Has the authorization been accepted?

Has the hardship package been marked complete?

Has a negotiator been assigned?

Has valuation been ordered?

Has the foreclosure department been notified that a short sale review is pending?

These details matter. They are the difference between "we submitted it" and "the lender is actually reviewing it."

For agents who want support without losing control of the client relationship, who we serve in short sale transactions explains how the right back-end team can support the file while the agent stays in position.

Can a Short Sale Stop Foreclosure in Texas?

Sometimes, yes. But it depends on timing, lender policy, investor rules, file quality, and how close the sale date is.

No one should promise a foreclosure postponement. That is a lender decision, and every file is different.

But a complete short sale request can give the lender something to evaluate before foreclosure happens. If the numbers make sense and the file is moving, the lender may decide that reviewing the short sale is better than pushing forward with foreclosure.

That is the window you are trying to create.

The Bottom Line

A Texas foreclosure sale date is serious, but it does not always mean the door is closed.

The key is speed plus structure.

Confirm the date. Build the file. Get the documents. Price realistically. Submit a complete package. Follow up with purpose. If there is a buyer, make sure the offer is clean and credible.

A short sale under foreclosure pressure is not the time for vague updates or "we'll see what happens."

It is the time to move the file like the calendar matters, because it does.

Short Sale vs Foreclosure Credit Impact in 2026

The missed payments are already stressful. Then the homeowner starts thinking about what comes next: credit damage, buying again someday, explaining the situation to a future lender, and whether foreclosure will follow them around like a bad financial tattoo.

That is usually when the short sale question gets serious.

For many distressed homeowners, the decision is not really “short sale or perfect credit.” That ship may have already left the dock wearing sunglasses. The real question is whether a short sale can create a cleaner exit than letting the property go all the way to foreclosure.

In many cases, yes. But the details matter.

The Credit Damage Usually Starts Before Either Option

By the time a homeowner is comparing a short sale vs foreclosure, the credit impact may already be underway. Missed mortgage payments are often the first major hit. Late payments can damage credit before the short sale is approved and before the foreclosure sale happens.

That is important because some homeowners assume the short sale itself is the only credit issue. Usually, it is not. The total impact can include:

- Missed mortgage payments

- Collection activity

- Foreclosure filings

- Charge-off or settlement reporting

- Deficiency balance issues

- Public record or court activity, depending on the state and process

A short sale does not erase the fact that payments were missed. But it may help stop the situation from turning into a completed foreclosure.

That distinction can matter when the homeowner is trying to recover.

Why Foreclosure Is Usually the Harsher Outcome

Foreclosure means the lender completed the legal process to take back or sell the property. From a future lender’s perspective, that can look more severe than a negotiated short sale because the borrower did not resolve the debt before the foreclosure process reached the finish line.

A short sale, by contrast, is a negotiated sale where the lender agrees to accept less than the full payoff to release its lien. The homeowner still sold the property, the lender reviewed the file, and the transaction closed through a formal approval process.

That does not make a short sale painless. But it may be viewed differently than foreclosure because the homeowner took action before the property was lost at sale.

This is why timing matters. If the foreclosure date is already close, the homeowner may still have options, but the path gets narrower. Starting early gives the lender more time to review the hardship, buyer offer, valuation, title issues, and closing terms.

If a homeowner is already behind, the better move is usually to start the short sale process before the foreclosure clock gets too loud.

Short Sale Reporting Can Vary

One reason this topic gets confusing is that short sales are not always reported the exact same way. Credit reporting can depend on the lender, loan type, account status, settlement terms, and how the servicer reports the account after closing.

A short sale may appear with language such as settled, paid for less than the full balance, account legally paid in full for less than owed, or similar wording. The exact phrasing matters less than the bigger point: it is generally different from a completed foreclosure.

Homeowners should not rely on casual promises like “this will not hurt your credit.” That is not how this works. A short sale can hurt credit. The question is whether it may be less damaging, more controlled, and more recoverable than foreclosure.

That is where experienced short sale help matters. The file should be reviewed for approval terms, deficiency language, lien releases, settlement statement accuracy, and closing conditions before anyone assumes the seller is protected.

The Deficiency Balance Can Matter Too

Credit impact is not the only issue. A homeowner also needs to understand whether the lender may pursue a deficiency balance after the sale.

A deficiency is the difference between what is owed and what the lender receives. In some short sales, the lender may waive the deficiency. In others, the approval letter may preserve certain rights or require a contribution. State law, loan type, investor rules, and approval language can all matter.

This is one of the reasons a short sale approval letter should be read carefully. The homeowner is not just trying to get permission to sell. They are trying to understand what happens after closing.

A sloppy approval can create confusion. A clean approval gives everyone a clearer path.

Agents Should Frame the Conversation Carefully

For real estate agents, the safest approach is to avoid overpromising. Do not tell a seller, “A short sale will save your credit.” That is too broad and may not be accurate.

A better conversation is:

A short sale may help avoid the additional damage of a completed foreclosure, but the seller should speak with credit, tax, and legal professionals about their specific situation.

That framing is honest and useful.

Agents can still play a major role by spotting the problem early, getting the file organized, pricing correctly, keeping the buyer engaged, and working with a short sale specialist who understands lender timelines. Crisp focuses on helping real estate agents close short sales faster so the agent is not stuck guessing while a foreclosure date gets closer.

The Big Practical Difference: Control

The biggest difference between a short sale and foreclosure is control.

With foreclosure, the lender and legal process drive the outcome. The homeowner may have limited say in timing, sale price, post-sale consequences, or how cleanly the file resolves.

With a short sale, the homeowner still has a chance to participate in the solution. The agent can market the property. A buyer can make an offer. The lender can approve terms. The closing can be coordinated. Title issues can be addressed before the final deadline.

That does not guarantee a perfect outcome. But it usually creates more room to work.

And in distressed real estate, room to work is everything.

Bottom Line

A short sale can still damage credit, especially when payments have already been missed. But foreclosure is usually the more severe outcome because it means the lender completed the process of taking or selling the property.

For homeowners in 2026, the better question is not whether a short sale is painless. It is whether acting now can prevent the situation from getting worse.

If the seller is behind, facing foreclosure, or worried about future credit recovery, the conversation should happen early. Not after the sale date is three business days away and everyone is sprinting through paperwork with cold coffee and regret.

Short Sale Relocation Assistance Denied? Timing Is Usually Why

The seller finally agrees to move forward with a short sale. The agent is relieved. The buyer is interested. The foreclosure date may be getting uncomfortably close.

Then someone asks the question everyone should have asked earlier:

Can the seller still get relocation assistance?

That is where things can get messy.

Short sale relocation assistance can be a meaningful lifeline for a homeowner who is already dealing with missed payments, moving costs, uncertainty, and the emotional joyride of bank paperwork. But relocation money is not automatic. It is often tied to lender rules, investor guidelines, occupancy status, timing, approval terms, and whether the file was handled correctly before the approval letter was issued.

In plain English: sellers usually do not lose relocation assistance because the idea was impossible. They lose it because the file was not positioned correctly early enough.

Relocation Assistance Is Usually Decided Before Closing

A common mistake is treating relocation assistance like a bonus that gets discussed at the end of the deal.

That is too late.

By the time the short sale approval letter is issued, the lender has usually already decided what it will allow, what it will pay, and what terms must be met before closing. If relocation assistance is not included in the approval structure, it may be difficult or impossible to add later.

This is why early short sale assistance matters. The seller's occupancy status, hardship, loan type, investor, sale timeline, and foreclosure status should all be reviewed before the file is too far along. A good short sale specialist is not just asking, "Can we get this approved?" They are also asking, "What terms should we protect before the bank issues approval?"

That distinction matters.

The Biggest Timing Mistake: Waiting Until Approval

The worst time to ask about relocation assistance is after everyone is already rushing toward closing.

At that point, the lender may have issued approval with no relocation incentive. The buyer may be pushing for a closing date. The title company may already be preparing settlement figures. The seller may assume money is coming, only to find out the approval letter says nothing about it.

Nobody enjoys that conversation. It has all the charm of finding out your moving truck has been double-booked.

Agents should raise the relocation question early, especially when the seller is still living in the property. Some programs require the home to be owner-occupied. Some require the seller to leave the property in acceptable condition. Some require signatures, affidavits, or specific lender review before approval.

If the seller moves out too early, ignores lender requests, misses document deadlines, or waits until foreclosure pressure is severe, relocation assistance may become harder to secure.

Occupancy Can Make or Break the Incentive

Many relocation assistance programs are built around helping an owner-occupant transition out of the property after an approved short sale.

That means occupancy matters.

If the seller already moved out, rented the property, abandoned the home, or left it in poor condition, the lender may deny relocation funds. The same can happen if the seller cannot verify occupancy or does not meet the lender's program requirements.

This does not mean every vacant property is automatically disqualified. Short sale rules vary by lender, investor, loan type, and program. But occupancy is one of the first things that should be reviewed when the seller asks about relocation money.

For agents, this is where helping real estate agents close short sales faster is not just about pushing the bank. It is about catching eligibility issues before they become closing-day surprises.

The Approval Letter Controls the Reality

Here is the practical rule: if relocation assistance is approved, it should be clearly reflected in the short sale approval letter or related lender instructions.

Verbal comments are not enough. "The bank said they might help" is not a closing strategy. It is a wish wearing business casual.

The approval letter should confirm the amount, recipient, conditions, and any restrictions. Some lenders may allow relocation money only if the seller signs an arm's-length affidavit, leaves the property by a specific date, or confirms they are not receiving other prohibited funds from the transaction.

If the approval letter is silent, unclear, or inconsistent with the settlement statement, the file needs attention before closing.

This is one reason strong short sale help can make a real difference. A short sale negotiator should review the approval terms, settlement statement, and seller expectations together so nobody assumes money is available when the lender has not approved it.

Foreclosure Timing Can Reduce Options

Relocation assistance is often easier to address when there is still enough time to submit a clean short sale package, respond to lender requests, and negotiate terms before the sale date becomes urgent.

When the foreclosure clock is already loud, the entire file becomes more compressed. The lender may be focused on whether the short sale can even be approved before the deadline. Investor review may take longer than expected. Missing documents may cause delays. A buyer may get impatient. The relocation question can get buried under more urgent problems.

That does not mean it is hopeless. But waiting narrows the path.

If a homeowner is behind on payments and hoping a short sale can help them avoid foreclosure, it is usually better to start the short sale process before every deadline is stacked against the file.

What Agents Should Ask Early

Before promising anything to the seller, agents should confirm:

- Is the seller still occupying the property?

- Has the lender or servicer mentioned relocation assistance?

- Is the loan type FHA, VA, conventional, or something else?

- Is there an active foreclosure date?

- Has the seller already received short sale approval?

- Does the approval letter mention relocation funds?

- Are there liens, HOA issues, or other settlement problems that could affect the closing statement?

These questions do not guarantee relocation money. They prevent false expectations.

And false expectations are dangerous in short sales because sellers are often making major life decisions under stress. If they believe they are receiving funds to help move, only to find out late that no incentive was approved, the deal can lose trust quickly.

The Bottom Line

Short sale relocation assistance is not something agents should treat as an afterthought. It is a timing-sensitive issue that should be reviewed early, documented clearly, and confirmed in the approval terms.

The seller may qualify. The seller may not. But the answer should not be discovered three days before closing.

If relocation assistance matters to the homeowner, bring it into the conversation at the beginning of the short sale file. Confirm occupancy. Review lender requirements. Watch the foreclosure timeline. Get the approval letter right.

Because in a short sale, the money sellers are counting on is only useful if the file is set up to protect it before the bank makes the decision.

Short Sale HOA Payoff Letter: The Deadline Agents Miss

The lender approved the short sale. The buyer is still in. The seller is packed. Everyone is ready to close.

Then, three days before closing, the title company says the HOA payoff is missing.

That is when a small association balance suddenly becomes a very large problem. The bank may have approved the short sale, but if the final HOA payoff letter, estoppel, lien release, or settlement demand is not ready, the closing can still stall.

The goal is not to order the final payoff too early. Those letters can expire, and some associations charge fees to issue or update them. The smarter goal is to get the HOA account balance early enough that the debt is already accounted for in the short sale numbers, then order the formal payoff after approval when closing is realistic.

Why HOA Balances Cause So Many Short Sale Delays

Short sales already have enough moving parts: lender review, investor approval, mortgage insurance, buyer timelines, appraisals, BPOs, seller documents, and title issues. HOA balances add one more layer, and they are easy to underestimate because the numbers often look small at first.

The problem is not always the monthly dues. It is everything wrapped around them.

There may be late fees, attorney collection fees, transfer fees, resale certificate fees, estoppel charges, lien recording fees, or release fees. By the time the final payoff is issued, the balance may be much higher than the agent expected.

That matters because the lender usually controls what can be paid from short sale proceeds. If the HOA demand shows up after approval and the lender has not accounted for it, the closing statement may need to be revised and resubmitted. That can send the file back into review. Nobody enjoys that sentence. Not even the bank.

This is where experienced short sale processing support matters. The HOA is not just a side note. It can affect the approval letter, the settlement statement, the seller's required contribution, and whether title can insure the transaction.

The Deadline Agents Usually Miss

The missed deadline is not ordering the final payoff too late. It is failing to find out the HOA balance early enough.

Agents should not necessarily order the formal HOA payoff letter at the beginning of the file. In many cases, that payoff can expire, become outdated, or create unnecessary fees before the short sale is approved.

But agents should get an HOA account balance statement early. That gives the short sale negotiator, title company, and lender a realistic picture of what must be accounted for in the deal.

Some associations respond quickly. Others work through management companies. Some files have already been sent to a collection attorney. Some communities require separate resale documents or estoppel requests once the transaction is ready to close.

If the HOA has recorded a lien, title may need a formal release. If legal fees are involved, the payoff demand may need to come from the attorney, not the association manager. If the seller has ignored HOA mail for months, the balance may be less "a few months behind" and more "please sit down before reading this email."

What a Short Sale Coordinator Should Check Early

A strong short sale coordinator should not wait for title to raise the alarm at the finish line. Early in the file, someone should confirm:

- Whether the property is part of an HOA or condo association

- Whether dues are current, behind, or in collections

- Whether the HOA has recorded a lien

- Whether a management company or attorney handles the account

- What the current account balance statement shows

- How long the final payoff or estoppel request usually takes

- Whether the lender is likely to approve HOA fees on the settlement statement

This does not mean every number will be final on day one. It means the risk is visible early enough to manage.

For agents, this is one reason helping real estate agents close short sales faster often comes down to process, not pressure. Calling the bank every day does not fix a missing HOA release. Knowing the issue exists before approval does.

The Lender May Not Pay Everything

Here is the uncomfortable part: even if the HOA demand is valid, the short sale lender may not approve every fee.

Some lenders will allow certain HOA dues or lien amounts. Others may cap what they allow. Some may reject attorney fees, late fees, or transfer charges. If the balance is high, the lender may ask for a reduced HOA demand, a seller contribution, a buyer contribution, or a revised net sheet.

That does not mean the deal is dead. It means the HOA issue has to be negotiated into the short sale approval structure.

This is where a short sale negotiator earns their keep. The negotiation is not only with the mortgage lender. Sometimes the HOA, collection attorney, title company, buyer side, and seller all need to be coordinated so the settlement statement can actually work.

What Agents Should Do Before Approval

Before lender approval, the goal is not always to order the final HOA payoff letter. The goal is to identify the HOA balance and risk.

Ask the seller early:

- Are you current with the HOA?

- Have you received collection letters?

- Is there a condo association, master association, or second HOA?

- Can we get a current account balance statement?

- Has the HOA recorded a lien or sent the file to an attorney?

Then loop in title and your short sale specialist early. If the HOA balance looks minor, confirm it. If there is a lien or attorney involvement, better to know before the bank approval clock starts ticking.

Once short sale approval is issued and closing is realistic, order the formal HOA payoff or estoppel so title has the final amount needed to close.

Why This Matters More in 2026

Short sale timelines are getting tighter because foreclosure pressure is rising in many markets. Sellers are often waiting longer before asking for help. Agents are stepping into files with less time and more complications.

That makes small title issues more dangerous.

An unpaid HOA balance may not sound dramatic compared with a foreclosure sale date, but it can create the same result: a delayed closing, a frustrated buyer, and a short sale file that needs another extension.

If a homeowner is already behind and the HOA issue is part of a larger distressed-sale picture, it is better to start the short sale process before every deadline is stacked against the file.

The Bottom Line

A short sale is not really ready to close until the lender, buyer, seller, title company, and lienholders are all aligned. The HOA is one of those lienholders people forget about until it gets loud.

The smartest agents treat the HOA balance like a closing-critical item, not paperwork housekeeping. Identify the association early. Get the account balance statement. Confirm whether there is a lien. Find out who manages the account. Then, after approval, order the final payoff or estoppel so title has the number needed to close.

Because in a short sale, the tiny line item nobody checked can become the reason everyone is suddenly asking for an extension.

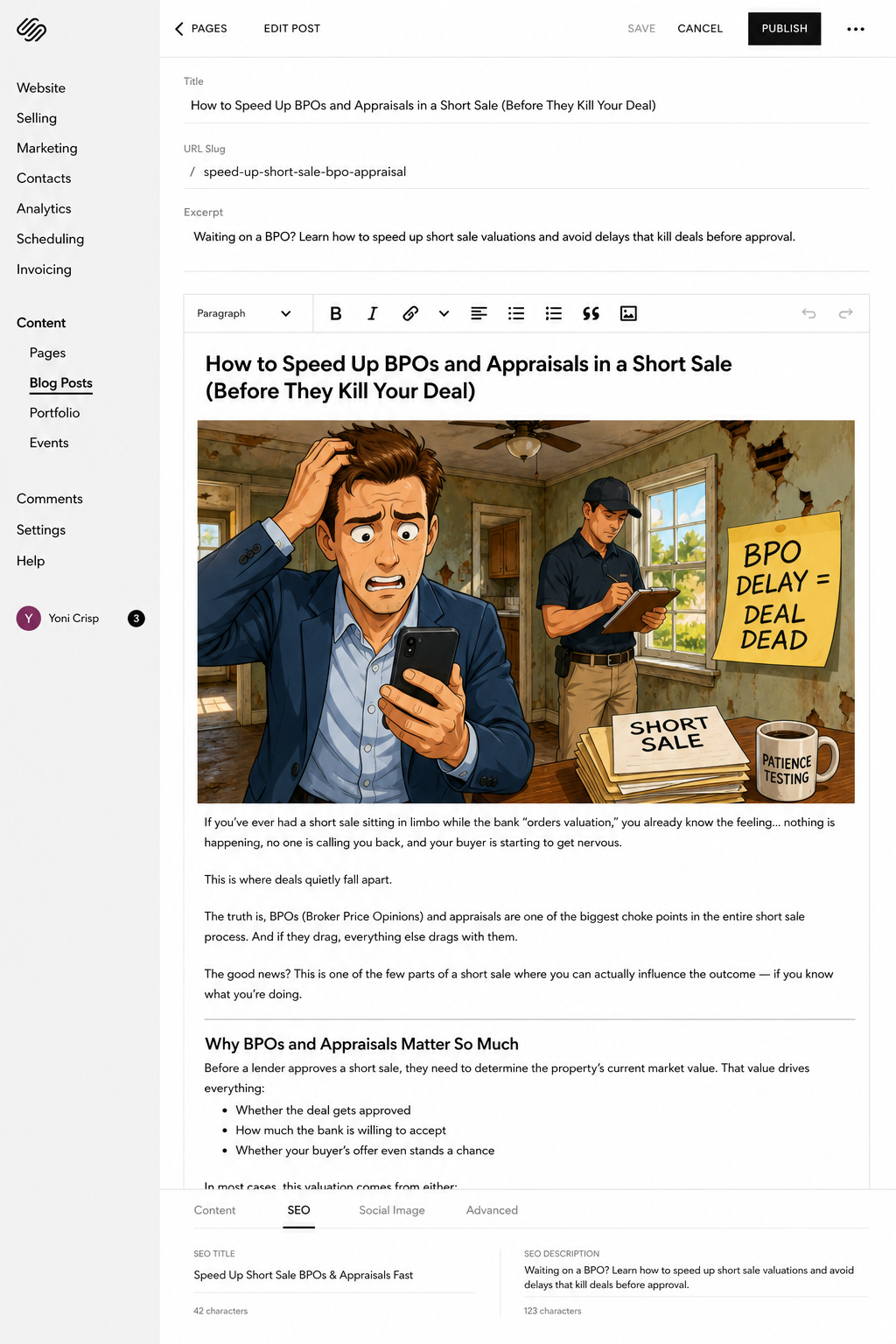

Houston Short Sale Timeline: How Fast Can It Close?

You finally have an offer on the table, the foreclosure clock is ticking, and everyone wants the same thing: get the short sale approved before the deadline turns into a disaster. Simple goal. Not always a simple path.

For Houston homeowners, the short sale timeline can feel especially stressful because Texas foreclosure timelines move quickly. One missed document, one slow lender response, or one pricing issue can turn a reasonable deal into a last-minute scramble. The good news? A Houston short sale can move faster when the file is packaged correctly, priced realistically, and pushed by someone who understands how lenders review these deals.

That is where strong short sale help matters.

How Fast Can a Houston Short Sale Close?

A Houston short sale can sometimes close in 45 to 90 days, but that depends on several moving parts: the lender, the investor, the buyer's financing, the property value review, and whether there are junior liens, HOA balances, tax issues, or mortgage insurance involved.

The biggest mistake is assuming the lender's approval is just a formality after an offer comes in. It is not. The lender still has to review the seller's hardship, financial documents, purchase contract, estimated closing statement, property value, and investor guidelines.

In plain English: the offer starts the race, but the short sale package determines how fast the race goes.

If you are already behind on payments or facing a sale date, the smartest move is to start the short sale process before the file becomes a five-alarm closing circus. And yes, "five-alarm closing circus" is a technical term in my office.

What Usually Slows Down a Houston Short Sale?

Most short sale delays are not random. They usually come from one of these issues:

- Missing or outdated seller documents

- A buyer offer that does not match lender value expectations

- A slow BPO or appraisal review

- HOA dues, tax liens, or second mortgages

- Mortgage insurance approval

- Investor rules that require extra review

- Poor communication between the agent, negotiator, lender, and title company

This is why short sale processing matters. A lender may ask for the same document more than once. A servicer may reject a file because one page is missing a signature. A closing statement may need to be revised multiple times before it matches investor requirements.

A normal listing can survive a little mess. A short sale with a foreclosure date usually cannot.

Why Houston Short Sales Need a Real Timeline Strategy

Houston agents and homeowners should not treat the timeline as "wait and see." That is how files stall.

A better strategy starts with three questions:

- Is there already a foreclosure sale date?

- Has the lender received a complete short sale package?

- Does the offer have a realistic chance of meeting the lender's valuation?

If the answer to any of those is unclear, the file needs immediate attention.

At Crisp Short Sales, our focus is helping real estate agents close short sales faster by keeping the lender review organized, tracking document requests, watching investor requirements, and pushing the file forward before delays become emergencies.

The agent still owns the relationship. The seller still needs guidance. The buyer still needs communication. But the file needs a short sale coordinator or specialist who knows where the bottlenecks usually hide.

Can a Houston Short Sale Stop Foreclosure?

A short sale does not automatically stop foreclosure just because the home is listed or because an offer has been submitted. The lender usually needs to see a complete file, a qualified buyer, and a realistic path to closing before it considers postponing a foreclosure sale.

That is why timing matters so much.

If a Houston homeowner waits until the week before foreclosure to begin, the file may still be possible, but every delay becomes more dangerous. If the short sale is started earlier, there is more room to correct documents, challenge valuation issues, negotiate junior liens, and request a postponement when appropriate.

This is one of the biggest reasons agents bring in a short sale specialist. The goal is not just to submit paperwork. The goal is to negotiate a short sale in a way that gives the lender enough confidence to keep reviewing the deal instead of letting the foreclosure proceed.

What Agents Should Do First

For agents, the first step is to confirm the urgency before spending too much time on the listing presentation.

Ask the seller:

- How many payments are missed?

- Has a foreclosure notice been received?

- Is there a sale date?

- Are there second mortgages, HOA dues, IRS liens, or other claims?

- Has the seller already submitted anything to the lender?

Then price the property with the lender's future valuation in mind. In Houston, a short sale priced too low may attract offers quickly, but it can also trigger a lender counter or denial if the BPO comes in higher. A short sale priced too high can sit too long and waste the time the seller does not have.

This is where professional short sale processing can make the transaction cleaner. The faster the right documents are collected and submitted, the faster the lender can make a real decision.

What Homeowners Should Do First

For homeowners, the first step is not panic. The second step is not hiding lender letters in a kitchen drawer and hoping they become less real. They do not. They multiply.

A Houston homeowner considering a short sale should gather:

- Mortgage statement

- Recent pay stubs or proof of income

- Bank statements

- Hardship explanation

- HOA information

- Any foreclosure notices

- Tax or lien documents, if applicable

The earlier these are organized, the better the odds of avoiding last-minute chaos. For a broader state-level view, the existing Texas short sale timeline breaks down why lender review and foreclosure timing need to be managed early.

The Bottom Line

A Houston short sale can move quickly, but it rarely moves quickly by accident. It takes a complete package, realistic pricing, lender follow-up, and a clear plan for foreclosure deadlines.

If you are an agent, the win is keeping the transaction alive and giving your client a real path forward. If you are a homeowner, the win is avoiding foreclosure when there is still time to pursue a short sale.

Houston timelines can be tight. The process does not have to be sloppy.

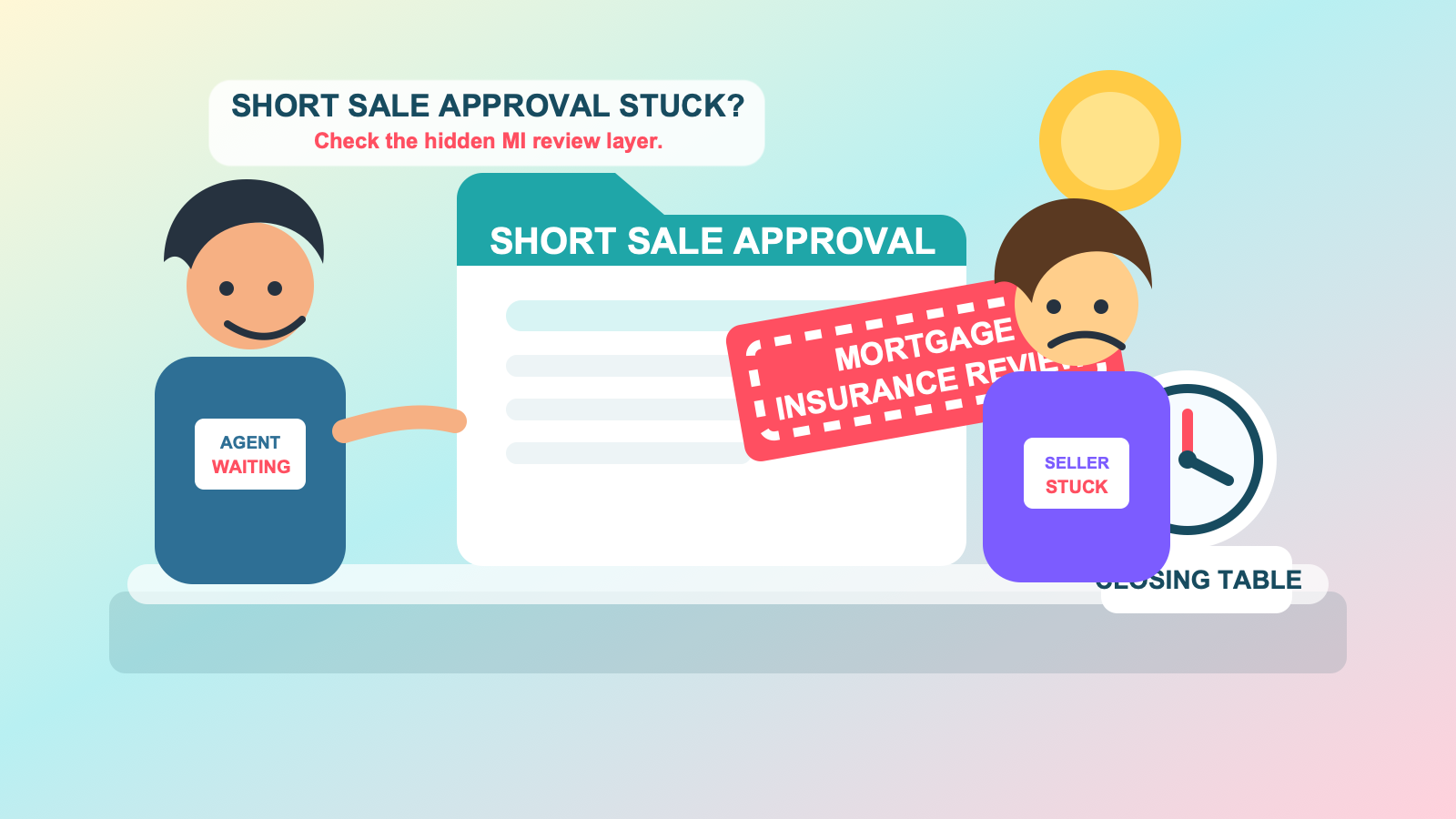

Short Sale Approval Delayed by Mortgage Insurance?

Related topic hub: Short Sale Approval Delays. It breaks down lender delays, document loops, valuation problems, mortgage insurance review, and next steps.

Fast Answer: Mortgage Insurance Short Sale Delays

Mortgage insurance can delay a short sale because the insurer may have to approve the lender's loss before the final short sale approval is released. The fastest path is to confirm whether MI review is active, identify the exact missing condition, and send one clean response package through the lender or short sale negotiator.

What To Do Next If MI Is Holding Approval

- Ask the lender whether the file is in mortgage insurance review or still waiting for investor approval.

- Get the exact missing condition in writing so the response does not turn into a guessing game.

- Keep the buyer, listing agent, and short sale negotiator aligned on timing before the contract loses momentum.

A short sale approval can feel painfully close, then mortgage insurance steps in and everything stalls. If your short sale approval is delayed by mortgage insurance, the goal is to identify the missing review issue fast, give the insurer what it needs, and keep the buyer from drifting away. The buyer is ready. The seller is packed. The agent is refreshing the inbox like it owes them money.

Then the short sale approval does not show up.

Even worse, the bank says the file is "still under review," even though everyone thought the review was basically done. This is one of those moments where a short sale can feel less like a real estate transaction and more like a mystery novel with too many characters.

One of the hidden characters? Mortgage insurance.

Mortgage insurance can be the extra approval layer that slows down a short sale, surprises the agent, and frustrates the seller. The servicer may appear to be the decision-maker, but if mortgage insurance is attached to the loan, the file may need another set of eyes before the approval letter is issued.

That does not mean the deal is doomed. It does mean the file needs to be handled carefully, because timing, documentation, and negotiation strategy matter.

The Bank May Not Be the Only Party Reviewing the File

In many short sales, the mortgage servicer collects the documents, orders the valuation, reviews the offer, and communicates with the agent or short sale negotiator. That makes it easy to assume the servicer has full authority to approve or deny the deal.

Sometimes they do.

Sometimes they do not.

If the loan has mortgage insurance, the mortgage insurance company may have a financial stake in the loss. That means they may need to review the proposed short sale terms before the servicer can issue final approval.

This is where sellers and agents often get blindsided. The file may move through document review, valuation review, buyer offer review, and investor review, only to hit another checkpoint near the finish line.

That checkpoint can affect:

The acceptable payoff amount

Seller contribution requests

Promissory note demands

Closing cost approvals

Commission approval

Whether the file can close before a foreclosure sale date

This is why experienced short sale assistance is not just about submitting paperwork. It is about knowing where approval authority really sits and anticipating what may slow the deal down.

Why Mortgage Insurance Can Create Delays

Mortgage insurance delays usually happen because the MI company is trying to limit its own loss.

From their perspective, a short sale is not just a seller asking the bank to accept less than the full balance. It may also be a claim event. The mortgage insurance company may be asked to cover part of the lender's loss, so they want to review whether the proposed short sale makes sense.

That review can take time, especially if the file is missing details or the numbers are unclear.

Common delay triggers include:

A purchase price below the valuation range

Unusual closing costs on the estimated settlement statement

Excessive credits to the buyer

A seller financial package that does not clearly show hardship

Missing income, bank statement, or tax documentation

A buyer who keeps extending without updated proof of funds

Last-minute changes to commissions, fees, or closing dates

This is where good short sale processing makes a real difference. A clean file does not guarantee instant approval, but a messy file almost guarantees extra questions.

And in short sales, extra questions are where timelines go to take a nap.

The Seller Contribution Surprise

One of the biggest mortgage insurance surprises is the seller contribution request.

A seller may believe the short sale has been accepted, then suddenly hear that the mortgage insurance company wants money at closing or a promissory note. That can feel unfair, especially when the seller is already in hardship.

But the request is not random. The MI company may be trying to reduce the claim amount or recover part of the loss directly from the seller.

That does not mean the seller should automatically agree.

A skilled short sale negotiator may be able to challenge the request, explain the seller's hardship, document limited financial ability, or negotiate the demand down. In some cases, the request can be reduced. In others, it may become part of the final approval terms.

The key is not to panic when the request appears. The key is to respond with documentation, not emotion.

Why Agents Need to Ask About MI Early

For real estate agents, mortgage insurance is one of those details that can quietly affect the entire transaction. If the agent does not know MI approval may be required, they may accidentally overpromise timelines to the buyer, seller, title company, or cooperating agent.

That creates pressure later.

A better approach is to build the possibility into the strategy from the beginning. When the file is opened, the agent or short sale specialist should look for signs that additional approval parties may be involved.

That may include:

Asking the servicer whether MI review is required

Watching for investor or insurer language in updates

Preparing the buyer for possible extensions

Keeping the seller's financials current

Making sure the estimated settlement statement is clean

Avoiding unnecessary fees that could trigger objections

This is one reason Crisp Short Sales focuses on helping real estate agents close short sales faster. Short sales are not just about getting an offer. They are about managing the approval path from start to finish.

What Sellers Should Do If the File Is Stuck

If your short sale seems stuck and no one can explain why, mortgage insurance may be one possible reason.

The first step is to get clarity. Ask whether the file is with the servicer, investor, mortgage insurance company, or another approval party. The answer matters because "under review" is not specific enough.

The next step is to make sure the file is complete and current. If updated pay stubs, bank statements, hardship details, or buyer documents are needed, delays can compound quickly.

Sellers should also be careful about ignoring communication from the servicer. A short sale file can be closed or delayed if requested documents are not returned on time. The bank may not wait politely forever, even if the seller feels like the bank has been taking its sweet time.

If there is already a foreclosure date, timing becomes even more important. The earlier you start the short sale process, the better the chances of managing extra approval layers before the timeline gets tight.

The Bottom Line

Mortgage insurance can delay a short sale because it may add another decision-maker to the approval process.

That does not make approval impossible. It just means the file needs to be positioned correctly. Agents need to understand who is reviewing the deal. Sellers need to keep documentation current. Buyers need to be prepared for possible extensions. And the numbers need to make sense before the file reaches the final approval stage.

A short sale can already have enough moving parts. Mortgage insurance adds one more.

The good news? Once you know it may be there, you can plan around it. And in short sales, planning around the hidden delay is often what keeps the deal alive.

Short Sale Relocation Assistance Before Foreclosure: Timing Matters

Foreclosure date coming up? See how short sale relocation assistance works, what mistakes can cost sellers the check, and why timing matters.

The foreclosure date is on the calendar, the moving boxes are not packed, and the seller is wondering the same thing at 2:13 a.m.: “If I do a short sale, can I still get help with moving money?”

Related topic hub: Foreclosure Urgency. It groups timing-sensitive posts for sale dates, foreclosure pressure, lender postponements, and short sale options.

Short Sale Relocation Assistance Hub

Relocation assistance is one of the most click-worthy short sale topics because the reader wants to know whether money may be available before moving. This hub connects the strongest posts on incentive programs, eligibility, timing, and foreclosure pressure.

- Can You Get Relocation Money in a Short Sale?

- Short Sale Incentive Programs: Get Paid to Move

- Short Sale Relocation Incentives: Who Gets Paid?

- What Is Relocation Assistance in a Short Sale?

- How Relocation Incentives Work in a Short Sale

- Can You Do a Short Sale Without Missing Payments?

- Georgia Short Sales: Avoid Foreclosure Earlier

- Utah Foreclosures Rising: When Short Sales Help

- Pennsylvania Foreclosures: When Short Sales Help

Ask about relocation assistance before approval terms are final

That question matters because relocation assistance is often not just about whether a seller qualifies. It is about timing, cooperation, documentation, and whether the short sale closes before the lender’s foreclosure process runs out the clock.

And yes, in the right situation, a seller may be able to receive relocation assistance through an approved short sale. But this is not magic money from the real estate fairy department. It has rules. It has deadlines. And if the file is handled casually, that check can disappear before anyone knows what happened.

The Window Can Close Faster Than Sellers Expect

A short sale is a negotiated settlement with the mortgage servicer or investor. The lender agrees to accept less than the full loan balance because it may be a better outcome than foreclosure.

Relocation assistance is separate. It is a payment some lenders or investors allow at closing to help the homeowner move after completing the approved short sale. For example, Fannie Mae’s current servicing guidance says eligible owner-occupant borrowers in a completed Fannie Mae short sale may receive relocation assistance, subject to specific exclusions and conditions.

The key phrase is “completed short sale.”

If the foreclosure sale happens first, there is no short sale closing. No closing usually means no relocation payment. That is why sellers who want to protect the possibility of relocation assistance should ask for short sale help as early as possible, not after the auction notice has already started breathing down everyone’s neck.

The Seller Usually Has to Cooperate All the Way Through

Relocation assistance is typically tied to cooperation. That means the seller needs to provide documents, allow access, sign forms, maintain communication, and move out as agreed.

Common seller mistakes that can put relocation money at risk include:

Waiting too long to submit the short sale package

Ignoring servicer document requests

Refusing reasonable showings

Letting the property deteriorate

Moving out without a plan

Assuming the buyer, agent, or title company controls the incentive

That last one is big. Relocation assistance is usually approved by the lender, investor, or servicer. It should appear in the written short sale approval and on the closing statement. If it is not confirmed in writing, do not treat it like guaranteed money.

Agents Should Ask About It Early

For agents, relocation assistance is not just a seller benefit. It can keep the file alive.

A seller who is overwhelmed, broke, and facing foreclosure may stop cooperating because the entire process feels pointless. When they understand that a successful short sale may provide moving funds, they often stay more engaged.

That does not mean agents should promise a payout. They should not. But they can ask the right questions early:

Is this an owner-occupied property?

Who owns or insures the loan?

Is there an active foreclosure sale date?

Has the seller already received relocation assistance from another source?

Will the servicer allow relocation funds in this file?

Will the incentive be listed in the approval letter?

This is where a strong short sale negotiator earns their keep. Crisp Short Sales helps with short sale assistance for agents and homeowners by tracking lender requirements, requesting available incentives, and making sure the approval terms are clear before closing.

The Foreclosure Date Changes the Strategy

If there is no foreclosure date yet, the strategy is usually straightforward: build the strongest short sale file possible and push for approval.

If there is already a sale date, the strategy becomes more urgent. The short sale team may need to request a foreclosure postponement, show that the property is actively listed, document the offer status, and prove that the lender has a better path than foreclosing.

This is where sellers get into trouble when they wait. A lender may be more willing to review a short sale when there is enough time to evaluate the hardship, order a valuation, review the buyer’s offer, negotiate liens, and approve the settlement. When the sale date is only days away, everyone is working with less oxygen.

Can a foreclosure sale be postponed? Sometimes. Is it guaranteed? Absolutely not. That is why the safest move is to start the short sale process before the timeline becomes an emergency.

What Sellers Should Do Right Now

If a seller is hoping for relocation assistance, the first step is not guessing. It is getting the file organized.

They should gather:

Mortgage statement

Hardship explanation

Pay stubs or income documentation

Bank statements

Tax returns if requested

HOA information

Any foreclosure notices

Listing agreement and buyer offer if available

They should also ask the servicer directly whether relocation assistance may be available for their loan type. Some investors have published rules. Some lenders have internal programs. Some files qualify, some do not.

The important thing is to ask early and document everything.

Bottom Line

Short sale relocation assistance can be a meaningful lifeline for a seller who needs to move before foreclosure. It may help cover deposits, moving trucks, utility setup, or the basic costs of getting a fresh start.

But it is not automatic. It depends on the investor, the servicer, the property occupancy, the seller’s cooperation, the approval terms, and whether the short sale actually closes.

If foreclosure is already in motion, timing becomes the whole game. The sooner the seller gets organized, the better the chance of preserving options, negotiating clearly, and avoiding the classic short sale tragedy: finding out help was available after the clock already ran out.

The Hidden Deadline Most Homeowners Miss Before Starting a Short Sale

The biggest mistake most homeowners make during financial hardship isn’t missing a payment.

It’s waiting too long to ask for help.

By the time many sellers finally start researching short sales, they’re already staring at a foreclosure sale date, nonstop lender letters, and a timeline that suddenly feels impossible to stop. What surprises people most is that there’s usually a hidden deadline long before the actual foreclosure auction — a point where options begin shrinking fast.

The earlier you act, the more control you keep.

And in many cases, homeowners who start the process sooner have dramatically better odds of avoiding foreclosure entirely, protecting future home-buying ability, and even qualifying for relocation assistance at closing.

The “Invisible” Timeline Most Sellers Don’t Realize Exists

A foreclosure sale date isn’t where the pressure begins. It’s where the pressure becomes unavoidable.

Long before that happens, lenders are already tracking:

- Missed payments

- Loan delinquency timelines

- Document submission deadlines

- Valuation orders

- Investor approval windows

- Foreclosure attorney scheduling

- Internal escalation milestones

Once certain internal deadlines pass, lenders become less flexible. Files move faster toward foreclosure departments, negotiators become harder to reach, and approval windows tighten.

That’s why homeowners who wait until “the last minute” often discover there’s far less time remaining than they thought.

Why Waiting Hurts Your Short Sale Chances

Many homeowners delay because they’re hoping something changes:

- The market improves

- Income increases

- The lender offers a modification

- A buyer appears immediately

- They somehow catch back up

Unfortunately, lenders usually don’t pause their timeline while homeowners figure things out.

A successful short sale requires time for:

- Gathering documents

- Completing hardship paperwork

- Valuation reviews

- Offer negotiations

- Investor approval

- Title work

- Closing coordination

That’s where experienced Crisp Short Sales teams can make a major difference. A professional short sale coordinator and short sale negotiator can often help organize the process early before the situation becomes urgent.

The Best Time to Start a Short Sale

Most homeowners assume they need to wait until foreclosure is imminent before beginning.

That’s usually the opposite of what works best.

The strongest short sale files often begin:

- After the first few missed payments

- When hardship becomes long-term

- Before the foreclosure attorney gets heavily involved

- Before a sale date is finalized

Starting early creates leverage.

It gives time to:

- Market the property properly

- Attract stronger offers

- Negotiate more effectively

- Resolve title or lien issues

- Communicate consistently with the lender

If you wait until the final weeks before foreclosure, every delay becomes dangerous.

What Happens If You Wait Too Long?

Every lender is different, but late-start files commonly run into problems like:

1. Incomplete Review Windows

The lender simply doesn’t have enough time to fully review and approve the file before the foreclosure date arrives.

2. Expedited Foreclosure Departments

Once files escalate internally, some departments become much harder to work with.

3. Buyers Walk Away

Investors and retail buyers often lose patience if timelines become chaotic or uncertain.

4. Missed Relocation Incentives

Some sellers may qualify for relocation assistance programs during a short sale, but delayed files can reduce those opportunities.

5. Increased Stress

This may be the biggest one. Last-minute short sales often become emotional emergencies instead of organized solutions.

The Good News: Foreclosure Isn’t Always Immediate

A lot of homeowners assume once they receive legal notices, it’s already too late.

That’s not always true.

Many short sales are approved surprisingly close to scheduled foreclosure dates — but those situations require fast action, complete documentation, and experienced communication with the lender.

That’s why homeowners often seek professional short sale help once they realize the process involves much more than simply listing the property.

Why Organization Matters So Much

Lenders are looking for complete, organized files.

Missing paperwork, delayed responses, or incomplete submissions can stall approval for weeks.

An experienced team handling:

- lender communication,

- document collection,

- buyer coordination,

- and short sale processing

can often reduce delays that otherwise kill deals.

That’s especially important for agents trying to manage multiple listings at once. Many Realtors partner with outside professionals who specialize in helping real estate agents close short salesfaster so the transaction doesn’t consume their entire schedule.

Homeowners Still Have More Options Than They Think

The earlier you explore solutions, the more likely you are to:

- avoid foreclosure,

- negotiate favorable terms,

- preserve future borrowing ability,

- and reduce overall stress.

Many homeowners are shocked to discover they had options available months earlier that disappeared simply because nobody explained the timeline properly.

Starting early doesn’t commit you to anything.

It simply gives you time to understand:

- your lender’s process,

- your available options,

- and what path makes the most sense for your situation.

Don’t Wait for the “Perfect Time”

There usually isn’t one.

The homeowners who have the smoothest short sales are rarely the ones who waited until the foreclosure clock hit panic mode. They’re the ones who addressed the problem early while options still existed.

If you’re already falling behind, receiving lender notices, or worried foreclosure may eventually happen, now is the time to ask questions and gather information.

Even one extra month can make a massive difference in whether a short sale succeeds.

If you want to explore your options or start the

Learn more about how we help real estate agents close short sales faster.

Start the short sale process. Getting organized early may be the single most important decision you make.

Why Investors Lose Money on Short Sales Even When the Deal Looks Great

You finally found it.

The listing looks underpriced. The comps support the value. The photos show "light cosmetic updates needed." The seller is motivated. On paper, it looks like a home run investment deal.

Then the short sale approval drags on for four months.

The lender counters higher than expected. The title search uncovers surprise liens. The property condition gets worse while waiting. The seller stops cooperating. Suddenly, the "great deal" barely breaks even — or worse, becomes a money pit.

This happens to investors every day.

The truth is, profitable short sales are rarely won by the investor with the lowest offer or biggest rehab budget. They’re usually won by the investor who understands the process best and works with the right short sale specialist behind the scenes.

Here are the biggest reasons investors lose money on short sales — even when the deal initially looks incredible.

1. They Underestimate the Timeline

One of the fastest ways investors lose money is assuming a short sale will close quickly.

Unlike a traditional transaction, the bank must approve the payoff before the sale can happen. That means the lender is reviewing:

- Seller hardship

- Financial documents

- Property value

- Investor guidelines

- Net proceeds

- Liens and title issues

- Purchase contract terms

If any piece is incomplete or submitted incorrectly, the process can stall for weeks.

Many investors line up contractors, hard money, holding costs, or resale plans before approval is finalized. Then delays start stacking up.

A professional short sale negotiator can dramatically reduce these delays by ensuring the package is complete from the beginning and proactively managing lender communication throughout the file.

That’s one reason many investors choose to work with experts who specialize in helping investors navigate complex short sales before the deal becomes expensive.

2. Hidden Liens Destroy the Numbers

A short sale might appear profitable until title work comes back.

Suddenly there’s:

- A second mortgage

- HOA debt

- Tax liens

- Contractor liens

- Judgments

- Utility balances

- IRS issues

Now the lender wants more money. The title company raises concerns. Negotiations become more difficult. Sometimes junior lienholders refuse to cooperate entirely.

Experienced short sale coordinators know how to identify these issues early and structure negotiations around them before the investor wastes months chasing a dead deal.

Without that preparation, investors often spend valuable time, inspections, and due diligence costs on deals that never close.

3. They Trust Zillow Repair Estimates

This one gets investors constantly.

Photos lie.

Listings often downplay condition issues, especially in distressed situations. Vacant homes can deteriorate rapidly during the short sale process itself.

By the time approval arrives, the property may now have:

- Mold

- Water intrusion

- Theft or vandalism

- HVAC damage

- Roof leaks

- Foundation problems

- Code violations

The longer the process drags on, the higher the risk.

Savvy investors budget conservatively and expect surprises. They also understand that strong short sale processing can shorten timelines and reduce the chance of the property sitting vacant for months deteriorating further.

4. Banks Care About Net Numbers — Not Investor Margins

Many investors assume if they submit a low offer with solid comps, the bank will simply accept reality.

Unfortunately, banks don’t always operate logically from an investor’s perspective.

Lenders rely heavily on:

- Broker price opinions (BPOs)

- Automated valuation models

- Internal investor guidelines

- Mortgage insurance requirements

- Investor restrictions

- Loss mitigation formulas

That means the bank may counter far above what actually makes sense for an investor.

This is where an experienced short sale processor becomes critical. Strong negotiators know how to challenge inflated valuations, dispute bad BPOs, provide repair estimates properly, and build a compelling value argument to the lender.

Without that guidance, many investors overpay just to "save the deal" — and wipe out their profit margin before renovations even begin.

5. Sellers Sometimes Stop Cooperating

Short sales are emotional.

Many homeowners are overwhelmed, embarrassed, stressed, or simply exhausted by the process. Some stop returning calls halfway through. Others delay paperwork for weeks. Some decide not to sell at all.

Every delay increases risk for the investor.

An organized system for communication, updates, document collection, and seller management is one of the most overlooked parts of successful short sale investing.

That’s why investors often rely on professional sale assistance and lender coordination services instead of trying to manage the entire process themselves.short

Keeping sellers engaged throughout the transaction can be the difference between a profitable closing and months of wasted effort.

6. They Ignore Carrying Costs During Delays

Even when a deal eventually closes, the numbers can quietly deteriorate during the waiting period.

Investors often forget to account for:

- Rising interest rates

- Insurance

- Taxes

- Utilities

- Hard money extension fees

- Contractor price increases

- Market shifts

- Opportunity cost

A deal projected to make $45,000 can slowly shrink to $15,000 or less if approval takes too long.

That’s why speed matters so much in short sales.

Efficient short sale negotiation is not just about getting approved — it’s about protecting the economics of the investment while the file is still alive.

7. They Try to Handle the Entire Negotiation Themselves

Some investors are excellent at acquisitions, construction, and disposition — but short sale negotiations are their own skill set entirely.

Every lender has different requirements.

Every negotiator handles files differently.

Every investor guideline changes over time.

Trying to learn everything mid-deal can become expensive fast.

Many successful investors eventually realize it’s more profitable to outsource the negotiation side completely and focus on what they do best: finding deals and closing transactions.

If you’re looking to start the short sale process on an investment property, having experienced guidance early can help prevent expensive surprises later.

Final Thoughts

Short sales can absolutely create incredible opportunities for investors.

But the investors who consistently profit are usually the ones who understand that the negotiation process itself is just as important as finding the property.

The best deals are not always the cheapest deals.

They’re the deals that actually close cleanly, close efficiently, and close with the profit margin still intact by the time the investor reaches the finish line.

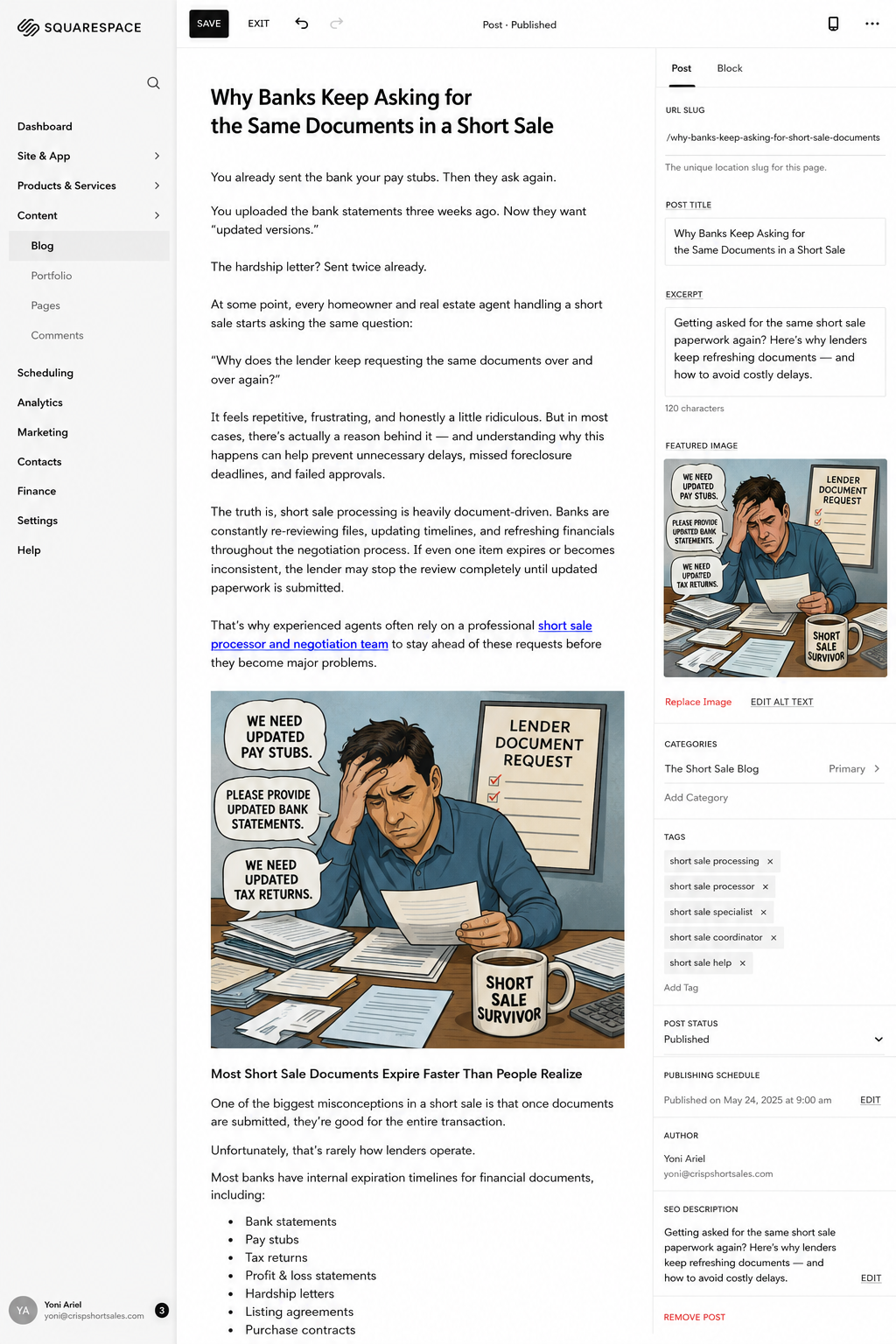

Why Banks Keep Asking for the Same Documents in a Short Sale

You already sent the bank your pay stubs. Then they ask again.

Related topic hub: Short Sale Approval Delays. It breaks down lender delays, document loops, valuation problems, mortgage insurance review, and next steps.

You uploaded the bank statements three weeks ago. Now they want “updated versions.”

The hardship letter? Sent twice already.

At some point, every homeowner and real estate agent handling a short sale starts asking the same question:

“Why does the lender keep requesting the same documents over and over again?”

It feels repetitive, frustrating, and honestly a little ridiculous. But in most cases, there’s actually a reason behind it — and understanding why this happens can help prevent unnecessary delays, missed foreclosure deadlines, and failed approvals.

The truth is, short sale processing is heavily document‑driven. Banks are constantly re‑reviewing files, updating timelines, and refreshing financials throughout the negotiation process. If even one item expires or becomes inconsistent, the lender may stop the review completely until updated paperwork is submitted.

That’s why experienced agents often rely on a professional short sale processor and negotiation team to stay ahead of these requests before they become major problems.

## Most Short Sale Documents Expire Faster Than People Realize

One of the biggest misconceptions in a short sale is that once documents are submitted, they’re good for the entire transaction.

Unfortunately, that’s rarely how lenders operate.

Most banks have internal expiration timelines for financial documents, including:

- Bank statements

- Pay stubs

- Tax returns

- Profit & loss statements

- Hardship letters

- Listing agreements

- Purchase contracts

- HUDs and settlement statements

Some lenders treat documents as “stale” after just 30 days. Others allow 60 or 90 days depending on investor guidelines.

That means if the negotiator, underwriter, valuation department, or mortgage insurer takes too long reviewing the file, the entire package may need to be refreshed before approval can continue.

And yes — sometimes that means resending documents that were already submitted perfectly the first time.

## Different Departments Review the File at Different Times

Another reason documents get requested repeatedly is because multiple departments inside the lender may touch the file during the short sale process.

The negotiator reviewing the hardship package is often not the same person reviewing the valuation. The mortgage insurer may have separate conditions. Investor approval may trigger additional underwriting reviews.

Sometimes the lender transfers the file to a new negotiator entirely.

When that happens, requests can restart almost from scratch.

This is one reason many real estate agents outsource short sale coordination rather than trying to manage every lender update themselves while also handling inspections, showings, contracts, and client communication.

A good short sale coordinator keeps the file organized so updated documents can be delivered immediately instead of losing another two weeks waiting on sellers to resend paperwork.

## Small Inconsistencies Can Trigger New Requests

Banks are extremely sensitive to inconsistencies during short sale review.

If one pay stub shows overtime income that wasn’t mentioned previously, the lender may ask for clarification.

If a bank statement suddenly shows a large deposit, they may request sourcing documentation.

If the seller changes jobs, opens a new account, or misses a payment during review, the lender may want updated financials to reassess hardship eligibility.

Even something minor — like a missing signature or an unreadable PDF upload — can trigger another document request cycle.

This is where professional short sale processing becomes less about “paperwork” and more about quality control.

An experienced short sale specialist knows how lenders review files and can often spot issues before submission, reducing unnecessary conditions and delays later.

## Foreclosure Timelines Don’t Pause Just Because Documents Are Missing

One of the biggest dangers with repeated document requests is timing.

Many sellers assume the lender will simply “work with them” indefinitely while paperwork gets updated. But foreclosure departments usually operate independently from loss mitigation.

That means the foreclosure clock may continue moving while the short sale file sits incomplete.

We’ve seen situations where:

- Sellers waited too long to provide updated documents

- Negotiators went silent for weeks

- Expired financials delayed approval review

- Foreclosure sale dates were scheduled before the file was fully escalated

This is why homeowners often reach out for short sale help early in the process instead of waiting until the foreclosure timeline becomes critical.

The earlier the file is stabilized and updated consistently, the more options usually remain available.

## Why Experienced Short Sale Negotiators Stay Obsessively Organized

The best short sale negotiators aren’t just good at talking to banks.

They’re good at preventing problems before they happen.

That means:

- Tracking document expiration dates

- Following up proactively with lenders

- Keeping sellers updated on upcoming refreshes

- Reviewing submissions for missing items

- Maintaining complete file history

- Resubmitting updated packages quickly when needed

A well‑managed short sale file moves differently than a reactive one.

Instead of scrambling every time the lender requests something, the file stays prepared for the next stage of review.

That can mean faster approvals, fewer surprises, and a much smoother experience for everyone involved — including the buyer waiting on the transaction.

## The Repeated Requests Are Annoying — But Usually Normal

If you’re currently dealing with a lender asking for updated paperwork again, you’re definitely not alone.

It doesn’t always mean something is wrong with the file.

In many cases, it simply means the short sale is still actively moving through lender review channels and the bank needs refreshed documentation before issuing final approval.