Short Sale vs Foreclosure Credit Impact in 2026

The missed payments are already stressful. Then the homeowner starts thinking about what comes next: credit damage, buying again someday, explaining the situation to a future lender, and whether foreclosure will follow them around like a bad financial tattoo.

That is usually when the short sale question gets serious.

For many distressed homeowners, the decision is not really “short sale or perfect credit.” That ship may have already left the dock wearing sunglasses. The real question is whether a short sale can create a cleaner exit than letting the property go all the way to foreclosure.

In many cases, yes. But the details matter.

The Credit Damage Usually Starts Before Either Option

By the time a homeowner is comparing a short sale vs foreclosure, the credit impact may already be underway. Missed mortgage payments are often the first major hit. Late payments can damage credit before the short sale is approved and before the foreclosure sale happens.

That is important because some homeowners assume the short sale itself is the only credit issue. Usually, it is not. The total impact can include:

- Missed mortgage payments

- Collection activity

- Foreclosure filings

- Charge-off or settlement reporting

- Deficiency balance issues

- Public record or court activity, depending on the state and process

A short sale does not erase the fact that payments were missed. But it may help stop the situation from turning into a completed foreclosure.

That distinction can matter when the homeowner is trying to recover.

Why Foreclosure Is Usually the Harsher Outcome

Foreclosure means the lender completed the legal process to take back or sell the property. From a future lender’s perspective, that can look more severe than a negotiated short sale because the borrower did not resolve the debt before the foreclosure process reached the finish line.

A short sale, by contrast, is a negotiated sale where the lender agrees to accept less than the full payoff to release its lien. The homeowner still sold the property, the lender reviewed the file, and the transaction closed through a formal approval process.

That does not make a short sale painless. But it may be viewed differently than foreclosure because the homeowner took action before the property was lost at sale.

This is why timing matters. If the foreclosure date is already close, the homeowner may still have options, but the path gets narrower. Starting early gives the lender more time to review the hardship, buyer offer, valuation, title issues, and closing terms.

If a homeowner is already behind, the better move is usually to start the short sale process before the foreclosure clock gets too loud.

Short Sale Reporting Can Vary

One reason this topic gets confusing is that short sales are not always reported the exact same way. Credit reporting can depend on the lender, loan type, account status, settlement terms, and how the servicer reports the account after closing.

A short sale may appear with language such as settled, paid for less than the full balance, account legally paid in full for less than owed, or similar wording. The exact phrasing matters less than the bigger point: it is generally different from a completed foreclosure.

Homeowners should not rely on casual promises like “this will not hurt your credit.” That is not how this works. A short sale can hurt credit. The question is whether it may be less damaging, more controlled, and more recoverable than foreclosure.

That is where experienced short sale help matters. The file should be reviewed for approval terms, deficiency language, lien releases, settlement statement accuracy, and closing conditions before anyone assumes the seller is protected.

The Deficiency Balance Can Matter Too

Credit impact is not the only issue. A homeowner also needs to understand whether the lender may pursue a deficiency balance after the sale.

A deficiency is the difference between what is owed and what the lender receives. In some short sales, the lender may waive the deficiency. In others, the approval letter may preserve certain rights or require a contribution. State law, loan type, investor rules, and approval language can all matter.

This is one of the reasons a short sale approval letter should be read carefully. The homeowner is not just trying to get permission to sell. They are trying to understand what happens after closing.

A sloppy approval can create confusion. A clean approval gives everyone a clearer path.

Agents Should Frame the Conversation Carefully

For real estate agents, the safest approach is to avoid overpromising. Do not tell a seller, “A short sale will save your credit.” That is too broad and may not be accurate.

A better conversation is:

A short sale may help avoid the additional damage of a completed foreclosure, but the seller should speak with credit, tax, and legal professionals about their specific situation.

That framing is honest and useful.

Agents can still play a major role by spotting the problem early, getting the file organized, pricing correctly, keeping the buyer engaged, and working with a short sale specialist who understands lender timelines. Crisp focuses on helping real estate agents close short sales faster so the agent is not stuck guessing while a foreclosure date gets closer.

The Big Practical Difference: Control

The biggest difference between a short sale and foreclosure is control.

With foreclosure, the lender and legal process drive the outcome. The homeowner may have limited say in timing, sale price, post-sale consequences, or how cleanly the file resolves.

With a short sale, the homeowner still has a chance to participate in the solution. The agent can market the property. A buyer can make an offer. The lender can approve terms. The closing can be coordinated. Title issues can be addressed before the final deadline.

That does not guarantee a perfect outcome. But it usually creates more room to work.

And in distressed real estate, room to work is everything.

Bottom Line

A short sale can still damage credit, especially when payments have already been missed. But foreclosure is usually the more severe outcome because it means the lender completed the process of taking or selling the property.

For homeowners in 2026, the better question is not whether a short sale is painless. It is whether acting now can prevent the situation from getting worse.

If the seller is behind, facing foreclosure, or worried about future credit recovery, the conversation should happen early. Not after the sale date is three business days away and everyone is sprinting through paperwork with cold coffee and regret.

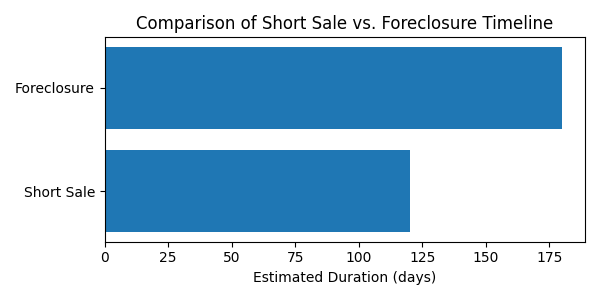

Short Sale vs. Foreclosure Timeline: What Homeowners Don’t Realize Until It’s Too Late

A breakdown of short sale vs. foreclosure timelines explaining how early short sale assistance helps homeowners maintain control, avoid delays, and minimize credit damage.

When homeowners fall behind on their mortgage, the conversation almost always centers on one question:

Related topic hub: Foreclosure Urgency. It groups timing-sensitive posts for sale dates, foreclosure pressure, lender postponements, and short sale options.

“How much time do I have?”

Unfortunately, that’s the wrong question.

The real difference between a short sale and a foreclosure isn’t just the final outcome—it’s who controls the timeline, the decisions, and the damage along the way. And most homeowners don’t realize how fast control slips away once foreclosure momentum starts.

Let’s break down what actually happens in each scenario, and why early short sale assistance can completely change the outcome.

The Foreclosure Timeline: Faster Than You Think

Foreclosure feels slow—until it isn’t.

Most homeowners assume they’ll receive plenty of warning before anything serious happens. In reality, the foreclosure timeline accelerates quickly once key deadlines pass.

Here’s what typically unfolds:

- Missed payments trigger default notices

- Legal filings begin (often before homeowners fully understand their options)

- Fees, legal costs, and interest stack up

- Decision-making shifts from homeowner to lender

- Sale dates get scheduled—even while homeowners are still “figuring things out”

Once foreclosure is in motion, options narrow fast. Loan modifications get denied. Buyers hesitate. And homeowners often discover too late that a short sale is still technically possible—but now much harder to execute cleanly.

This is where many deals fail: not because a short sale wasn’t allowed, but because it was started too late and without structure.

The Short Sale Timeline: Slower, but Strategic

A short sale doesn’t stop time—it replaces panic with process.

When started early and handled correctly, a short sale gives homeowners breathing room while maintaining control over key decisions like:

- Who buys the home

- When the sale closes

- How relocation is handled

- What the final credit impact looks like

Unlike foreclosure, a short sale timeline is driven by documentation, valuation, and lender review—not court schedules.

But here’s the catch: banks don’t wait forever.

Delays, missing documents, or sloppy communication can quietly push a short sale past the point of no return. That’s why experienced short sale processing matters far more than most homeowners realize.

What Homeowners Don’t Realize Until It’s Too Late

This is where timelines collide—and mistakes become permanent.

1. Waiting Does Not Buy Time

Many homeowners delay action because they’re overwhelmed or hopeful something will change. Unfortunately, waiting usually reduces options instead of preserving them.

By the time foreclosure notices feel “real,” lenders may already be less flexible.

2. Short Sales Are Front-Loaded

The most important work in a short sale happens early:

authorizations, hardship review, document accuracy, and valuation strategy.

If those pieces aren’t handled properly from the start, approvals stall—or get denied outright.

This is where a dedicated short sale coordinator or short sale negotiator makes a measurable difference.

3. Foreclosure Narrows Buyer Interest

Buyers get nervous when foreclosure timelines tighten. They worry about auctions, title issues, and approval risk.

That reduces leverage and limits offers—exactly the opposite of what homeowners need.

4. Relocation Help Is Time-Sensitive

Relocation assistance (often called “cash for keys”) is far more likely when a short sale is organized early and presented correctly. Once foreclosure progresses, those opportunities often disappear.

At Crisp, this kind of homeowner support is built directly into how we help distressed sellers navigate the process.

Control Is the Real Difference

A short sale isn’t just about avoiding foreclosure—it’s about preserving agency.

Foreclosure is something that happens to homeowners.

A short sale is something homeowners participate in.

When structured correctly, a short sale allows families to:

- Exit with dignity

- Avoid last-minute chaos

- Minimize long-term credit damage

- Move forward on their own timeline

That’s why we focus on short sale assistance that starts early, stays proactive, and doesn’t rely on hope or guesswork.

Whether we’re helping homeowners directly or supporting agents through the process, our role is to keep files moving, lenders engaged, and deadlines under control. You can see exactly who we work with on our who we serve page.

The Right Question to Ask

Instead of asking, “How much time do I have?” Homeowners should be asking:

“How much control do I want to keep?”

If foreclosure is already on the horizon, the window for a successful short sale hasn’t necessarily closed—but it is narrowing.

Starting the short sale process early, with experienced guidance, is often the difference between an orderly transition and a forced one. If you’re considering next steps, this is the moment to start the short sale process before decisions get made for you.

Why Cash Buyers Love Short Sales (and How Sellers Benefit)

When a homeowner is facing foreclosure, a short sale can feel like the only light at the end of a very long tunnel. But here’s a little secret: cash buyers—especially seasoned investors—absolutely love short sales. And that’s not a bad thing. In fact, when investors jump in, sellers often benefit in ways they didn’t expect.

Cash Buyers Thrive on Distress Deals

Investors make their living finding properties with built-in equity opportunities. A short sale is exactly that: a home being sold for less than what’s owed. Since banks are motivated to cut their losses rather than deal with foreclosure, these homes often hit the market below typical pricing.

For a cash buyer, it’s like walking into a clearance aisle. For a seller, this means your listing is far more attractive to investors, which increases the chances of getting an actual buyer under contract quickly. For more tips on keeping your short sale moving, check out our advice on why some short sales stall and how to keep yours moving.

Speed is the Name of the Game

Traditional buyers often need weeks (sometimes months) for loan approvals, appraisals, and underwriting. In a short sale, where every day counts, that delay can be deadly.

Cash buyers eliminate that problem. They don’t need mortgage approvals, so they can close faster once the bank issues its short sale approval. For homeowners, this can mean shaving weeks off the timeline—sometimes the difference between approval and foreclosure.

Banks Prefer Cash Buyers Too

Here’s something many agents and homeowners don’t realize: banks reviewing short sales love to see a cash offer. Why? Less risk.

Financing contingencies mean more opportunities for deals to fall apart. If a buyer’s loan is denied, the bank is back at square one. A cash buyer signals certainty—the deal is almost guaranteed to close once approved. That assurance can help push the file across the finish line, as explained in what happens after you accept a short sale offer.

Sellers Don’t Pay the Investor’s Discount

One common misconception is that if an investor gets a “deal,” the seller somehow loses out. Not true in a short sale.

Remember, the seller isn’t pocketing any money in the transaction—the lender is the one taking the loss. So when an investor buys at a discount, it doesn’t harm the homeowner’s bottom line. In fact, sellers still get the same benefits: avoiding foreclosure, wiping out debt, and potentially qualifying for relocation assistance.

Relocation Assistance is Still on the Table

Cash buyers don’t interfere with relocation incentive programs. In fact, a strong cash offer may make it more likely that the deal closes, which means the homeowner actually receives the relocation funds (instead of losing them if the short sale collapses).

The Win-Win Dynamic

At first glance, it might feel like investors are just hunting for bargains at a seller’s expense. But in reality, their motivation to buy fast and close reliably is exactly what makes short sales succeed.•.

• Investors win by securing a property below retail.

Homeowners win by avoiding foreclosure, protecting their credit, and moving forward with dignity.•

That’s the essence of a short sale: everyone gives a little, but everyone gains something too.

Final Thoughts

Cash buyers aren’t the enemy in short sales—their ability to pay cash and move quickly often turns them into the heroes. If you’re a homeowner considering a short sale, don’t shy away from investors. Their ability to pay cash and move quickly could be the very thing that saves your home from foreclosure and gives you the fresh start you need.

At Crisp Short Sales, we specialize in bringing these pieces together—negotiating with banks, connecting with serious buyers, and ensuring sellers walk away with the best outcome possible.